The financial challenges presented by asbestos liabilities are not fading away as most insurance professionals have long hoped.

Executive Summary

Declining death rates from prostate cancer and a precipitous fall in the incidence of smoking may seem to have little to do with P/C carrier reserving for asbestos liability claims. But William Wilt and Alan Zimmermann of Assured Research see a link and cite these among the reasons that actuarial models systematically underestimate exposures.In fact, A.M. Best raised its estimate of ultimate asbestos liability losses by $10 billion to $85 billion in late 2012. More recently, insurers including Chubb, American Financial Group, Allstate, Hartford and Travelers all increased the charge taken for asbestos in 2013 over that of 2012.

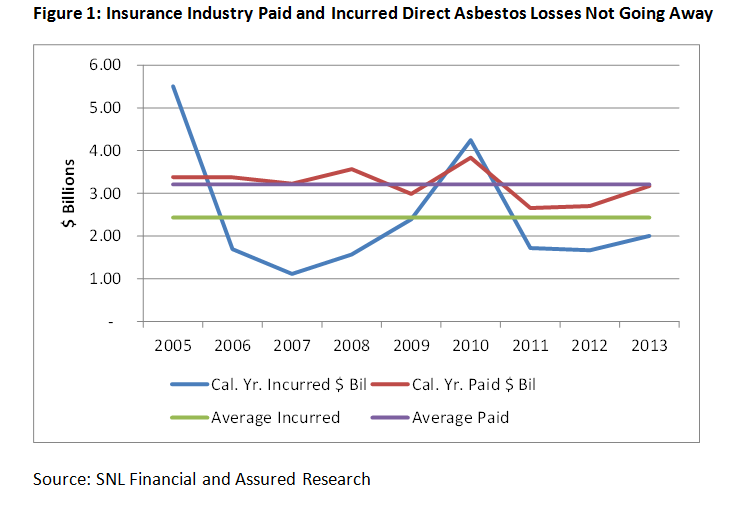

Industrywide, year-end 2013 statutory data reveals that direct asbestos payments rose to $3.2 billion—well above the $2.5 billion paid the two preceding years. The industry stepped up its reserving activity as well, incurring about $2.0 billion of losses compared to the $1.6 billion in each of the two preceding years.

What’s Happening, and Why Now?

As occupational exposure to asbestos declined rapidly from the 1970s onward, most insurance professionals could be excused for believing that actuarial models could, at this point, be sufficiently well-calibrated to forecast the incidence of mesothelioma, the deadly cancer most commonly caused by exposure to asbestos. Except that doesn’t seem to be the case.

Assured Research has written extensively on the topic of asbestos during 2014. A short summary of our position includes:

1. Actuarial models are systematically underestimating exposures.

New epidemiological studies and dramatic shifts in medical knowledge, life expectancies and societal behaviors warrant another, likely material overhaul of the actuarial models. Importantly, as we discuss in detail below, longer life spans increase the probability that people will discover and report asbestos-related diseases as more of them live through the 30-plus-year latency period for asbestos disease.

2. A third wave of asbestos exposures could sweep the nation.

We do not believe this potential third wave is adequately accounted for in insurers’ loss reserves as these new claims are typically nonoccupational exposures (known as “bystander” exposures in industry parlance). Insurers most often reserve only for occupational exposures.

In many cases, the plaintiffs are longtime smokers with some form of above-normal, nonoccupational exposure to asbestos.

We invite interested readers to contact us for our previously released work, but several of the main points of our research are summarized below.

Actuarial Models Are Outdated

We have come to believe the models used by major consulting firms—and, most likely, many insurance companies—rely on outdated assumptions. With those models constructed in the mid-1980s and recalibrated once in the later-1990s, we observe that new epidemiological studies and dramatic shifts in medical knowledge, life expectancies and societal behaviors warrant a push of the reset button.

The result, we expect, would be higher forecasted claims and an explanation for the series of annual “surprises” that many insurers relay each time they fund rising asbestos payments with yet another “one-time” annual reserve charge.

We can cite a few specific examples of areas in which the models lag current information:

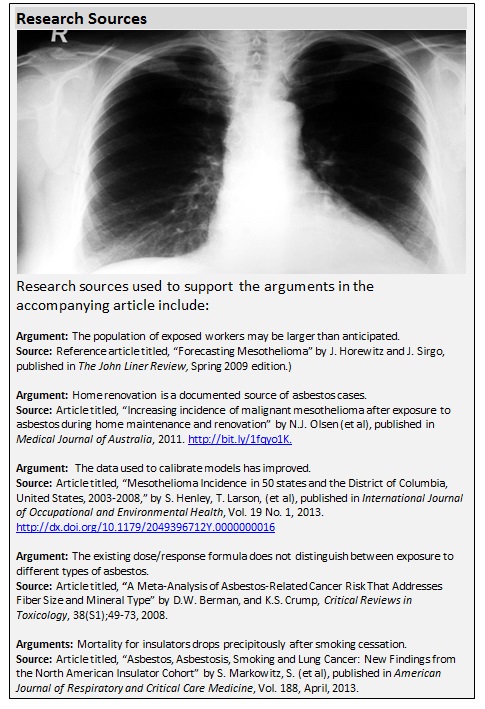

• The population of exposed workers may be larger than anticipated.

Most actuarial models have at their core pioneering work performed by William Nicholson (et al) in 1982. The authors of this seminal study evaluated and forecasted mortality from occupational exposure to asbestos in their paper titled “Occupational Exposure to Asbestos: Population at Risk and Projected Mortality.”

Nearly 30 years later, in 2009,researchers using new data and methodologies expanded by nearly 50 percent the size of the labor force considered exposed to asbestos—from 27.5 million people to 41.1 million workers. (Researchers Horewitz and Sirgo. See the accompanying textbox below article, “Research Sources,” for full references to all scientific and medical research articles discussed in this article.)

We are unable to judge whether the occupationally exposed populations feeding into most actuarial models use this expanded labor force, or whether they are sufficiently comprehensive at this point. We can observe, however, that recent medical literature suggests even short but intense exposures to asbestos can lead to serious asbestos-related illnesses.

Home renovation, for instance, has become a documented source of claims. (See, for example, Olsen, NJ (et al) at http://bit.ly/1fqyo1K.)

Those applying the actuarial models and using their output would probably be well served to pause and question whether today’s estimates of the occupationally exposed population are sufficiently comprehensive.

Even if all subsequent model and actuarial parameters operated perfectly, shortcomings in this important raw material—the size of the affected population—would lead to inaccurate claim projections.

• The data used to calibrate models has improved but is not incorporated.

A 2013 paper in the International Journal of Occupational and Environmental Health updated national and state-specific incidence of mesothelioma with data covering all 50 states and 100 percent of the U.S. population. The data immediately prior had covered just 40 states and 88 percent of the population. But both of these were dramatic improvements over still earlier SEER data—based on the National Cancer Institute’s Surveillance, Epidemiology and End Results, or SEER registries—that only covered some 26 percent of the U.S. population.

A 2013 paper in the International Journal of Occupational and Environmental Health updated national and state-specific incidence of mesothelioma with data covering all 50 states and 100 percent of the U.S. population. The data immediately prior had covered just 40 states and 88 percent of the population. But both of these were dramatic improvements over still earlier SEER data—based on the National Cancer Institute’s Surveillance, Epidemiology and End Results, or SEER registries—that only covered some 26 percent of the U.S. population.

It is our understanding that the new, more comprehensive datasets reveal that prior estimates of mesothelioma incidence extrapolated from the less complete datasets tended to underestimate the true number of cases. (Henley, S. Larson, T. (et al), “Mesothelioma Incidence in 50 states and the District of Columbia, United States, 2003-2008,” published in International Journal of Occupational and Environmental Health, Vol. 19 No. 1, 2013.)

This is an issue any actuary or insurance executive can understand implicitly. Models that were trained long ago on incomplete or unrepresentative data will produce forecasts that are inherently flawed to at least some degree.

• The dose/response formulas embedded in today’s models rely on outdated science.

The research performed by Nicholson and his colleagues involved: (i) identifying cohorts of workers exposed to asbestos; (ii) estimating the level or intensity of their exposure to asbestos; and (iii) forecasting the incidence or manifestation of mesothelioma (and related diseases) among those populations with consideration for their level of exposure. This is the dose/response measure to which we refer, and it is our understanding that it has not been updated since the mid-1980s.

And while many formulas and algorithms have withstood the test of time, in the face of rapidly advancing science it’s probably not too soon to question the veracity of this important formula. After all, if the exposed population is getting sick with more (or less) frequency than predicted by the current dose/response formula, the overall models won’t produce accurate forecasts, broadly speaking.

Without delving too deeply, we can share that researchers now understand that the body’s response to different types of asbestos fibers can vary greatly. Still, authors Berman and Crump writing in Critical Reviews of Toxicology (2008) reveal that the dose/response formula currently in use does not distinguish between workers’ exposure to different types of asbestos. Citing earlier work, the researchers note that amphibole asbestos, which is needle-like in appearance, is 100-500 times more potent for causing mesothelioma and possibly 10-50 times more potent for causing lung cancer than the more common chrysotile asbestos, sometimes called white asbestos.

Simply put, workers from varied industries or from different parts of the U.S. could have materially different exposure to these distinct fiber types, but none of that is accounted for in the currently used dose/response formula.

Thankfully, the U.S. used predominantly chrysotile asbestos, but workers in the U.K. and elsewhere were less fortunate; amphibole asbestos was more common and the higher incidence of mesothelioma in those countries bears out the somber statistics.

We are neither Ph.D. researchers nor modeling experts. Those are challenging jobs indeed. We are, however, advocates for challenging the status quo. If the models don’t work, time and effort should be invested to understand why.

People Are Living Into Their Disease

The long latency period of asbestos illnesses is well understood—and documented at 30-plus years depending on the intensity of exposure. Yet current actuarial models are unlikely to account for both rising life expectancy overall or, more important, changes that specifically affect the population of occupationally exposed workers.

Longer life spans mean more people will live to discover their asbestos-related illness and report a claim.

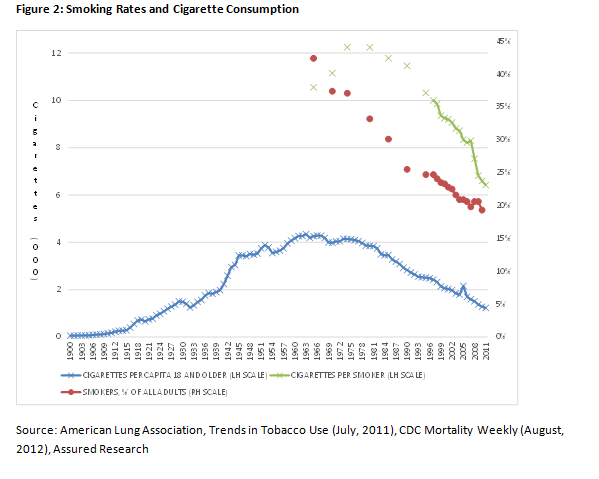

For instance, death rates from prostate cancer have fallen by 20 percent over the past 10 years. (Occupational asbestos exposure affects males predominantly.) Even more impactful is the fact that smoking rates have plummeted since the 1980s when the epidemiological models were first created, and even more recently the volume of cigarettes consumed by smokers has declined dramatically.

Figure 2 shows that fewer Americans are smoking and that those who do smoke less—45 percent less measured from 1985 when the epidemiology study regarding smoking and asbestos was incorporated into the actuarial model.

In short, there have been some massive societal shifts in smoking over the past 25 years. But what is the impact on serious asbestos claims, such as mesothelioma, lung cancer and asbestosis? Perhaps counterintuitively, we believe it will lead to more claims.

Medical researchers are increasingly recognizing—and documenting—the malignant synergy between asbestos exposure, asbestosis and smoking. One recent study found asbestos exposure—in the absence of asbestosis—increased the lung cancer rate 5.2-fold among nonsmokers compared to smoking, which increased the rate by 10.2-fold. Taken together, however, the rate of lung cancer increased more than 28 times.

When a smoker also has evidence of asbestosis (i.e., documented damage and scarring to the lungs caused by asbestos exposure), his risk of developing lung cancer is nearly 37-times that of this study’s control group. (Markowitz, S. et al)

Less appreciated, however, is that smoking cessation has an almost equally powerful, and favorable, impact on longevity. For instance, one recent study (the Markowitz study) concluded that “lung cancer mortality among insulators [installers of asbestos insulation] dropped precipitously after smoking cessation, and proportionate to that of smokers who were unexposed to asbestos.” After 30 years, the risk of lung cancer death among the insulators studied was no different than that of insulators who had never smoked.

Taken with rapid advancements in the treatment of advanced-staged critical illnesses (e.g. heart disease, colon or prostate cancer, to name a few), people who worked in industries with exposure to asbestos are simply living longer.

Think of it, a 65-year-old insulator and former smoker diagnosed at that age in 1985 might have died within a few years—before asbestosis and years of smoking turned into a reportable claim. Roll the clock forward and that same 65-year-old in 2010 had a 98 percent chance of surviving his prostate cancer past 10 years—plenty of time for years of smoking and asbestos exposure to fuse and become a reportable asbestos claim. Yet the models used to predict the incidence of mesothelioma are still drawing many of their parameters from the mid-1980s.

New Screening Recommendations May Increase the Number of Claims

In 2013, the U.S. Preventive Services Task Force recommended that current and former heavy smokers between the ages of 55 and 80 should undergo annual CT scans. As many as 10 million people could be affected by this recommendation.

Importantly, the Task Force’s recommendation included a grade of “B,” which should lead to the annual procedure being covered by Affordable Care Act-compliant health plans.

We won’t speculate as to the percentage of those 10 million people who might be found to have asbestos-induced lung scarring, but clearly the answer is not zero. This development alone should lead to an uptick in the number of asbestos claims and lawsuits.

Some insurers have bravely, or naively, reported that the asbestos environment is little changed in recent years. We disagree. Social, legal and medical trends as well as insurer’s own reserving behavior all suggest the opposite is true.

Berkshire-owned Utility Urges Oregon Appeals Court to Limit Wildfire Damages

Berkshire-owned Utility Urges Oregon Appeals Court to Limit Wildfire Damages  Flood Risk Misconceptions Drive Underinsurance: Chubb

Flood Risk Misconceptions Drive Underinsurance: Chubb  Experts Say It’s Difficult to Tie AI to Layoffs

Experts Say It’s Difficult to Tie AI to Layoffs  Earnings Wrap: With AI-First Mindset, ‘Sky Is the Limit’ at The Hartford

Earnings Wrap: With AI-First Mindset, ‘Sky Is the Limit’ at The Hartford