Mike McGavick, the former chief executive of XL Group and Safeco Insurance, sees exciting possibilities ahead for AI to refocus the insurance industry on the problems it is designed to solve.

But today, the industry is falling short, he says.

“There is unbelievable opportunity, and unbelievable need for us to play our role with AI,” McGavick told a group of actuaries at the Casualty Actuarial Society Seminar on Reinsurance this week.

Executive Summary

Mike McGavick, the former CEO of XL, sees exciting possibilities ahead for AI to refocus the insurance industry on problems it is designed to solve. But today, the industry is falling short, he says.

During a keynote speech at the Casualty Actuarial Society Seminar on Reinsurance this week, McGavick was enthusiastic, not just about AI but also about the role of actuaries at the center of change, influencing trust in AI models. Still, he believes insurers aren’t living up to pronouncements they are making about their ability to harness AI today, nor are they fulfilling their central promises to efficiently transfer risks from society as they emerge.

Offering the perspective of a leader with three decades of industry experience, he described repeated patterns of carrier reactions to technological change—exclude it, harness it and then look for opportunities to insure it. He also offered his perspective as the non-executive chairman of an AI platform that automates insurance operations, describing how small domain-specific language models (dsDMs) are poised to transform underwriting, claims, reinsurance and actuarial work.

“Our whole purpose in life should be to look at society and the risks it really faces and to do everything we can to create products that can transfer that risk so that people can focus on their lives and creativity and all the solutions that come from this massive change in society,” he said. He offered this view near the end of a presentation that started with the veteran executive describing repeated patterns of technology adoption he’s observed over the course of more than three decades in the industry. He also punctuated his remarks with a challenge to actuaries to embrace their roles as model arbiters to pave the way forward.

In the end, he said the insurance industry exists “to take on what government can’t and to try to do it in an extremely economic and efficient way and make the world better—make the world take the risks that keep humanity improving. That’s our job. And yet right now, we aren’t doing it,” he said, offering an example of the industry’s role in cyber risk transfer to support his view.

Specifically, McGavick cited figures that put cyber insurance premiums at about $30 billion and the total amount of cyber crime globally at $10.5 trillion. Noting that cyber insurance loss ratios are roughly 50 cents on the dollar, the industry is, at most, addressing $15 billion of that.

(Editor’s Note: In a report last year, Munich Re put cyber insurance premiums at roughly $16 billion in 2025, projecting a $30 billion figure by 2030: “Cyber Insurance: Risks and Trends 2025.” The $10.5 trillion is a commonly cited figure from Cyber Ventures “Cybercrime Cost Predicts 2025 to 2031.”)

“We’re doing the stuff we know and are comfortable with” while risks are growing, he said. “The challenge is how to get out in the open on the horizon of opportunity—make the difference we’re called upon to make in society and to really do our jobs,” he said.

Read more in the related article: A $10.5 Trillion Cyber Problem: Whose Risk Is It Anyway?

Patterns Repeat

While McGavick also highlighted the level of inefficiency that persists in the industry, he was overwhelmingly enthusiastic about the promise of AI agents to deal with that and the role of actuaries at the center of change, influencing trust in AI models.

“This is the sexiest spot in insurance,” he said as he opened the talk. “I believe fundamentally every day that moves forward, actuaries become more important in the entire insurance ecosystem because there is no other group prepared and trained to continue to add trust to a world that is already distrusted and now, as it begins to use its AI journey, will be even more distrusted.”

“This is a huge moment. We know [what’s] coming is massive. But we just ain’t there yet,” McGavick told the actuaries assembled in a Philadelphia conference room, going on to describe the industry patterns that will repeat to shape how AI comes into the property/casualty insurance sector.

“Every day that moves forward, actuaries become more important in the entire insurance ecosystem. There is no other group prepared and trained to continue to add trust to a world that is already distrusted and now, as it begins to use its AI journey, will be even more distrusted.”

Mike McGavick

“How do we react to tech in the insurance industry? No. 1, exclude it. No. 2, try to harness it and eventually get greedy and figure out how to insure it.” Breaking the last two parts down further, he said insurers first attempt to harness technology to lower their own costs. Then they try to refine core insurance processes to be more effective: “We try to rethink how underwriting might be done with this tool at hand, how claims handling might be done.”

The third step involves starting to think about new risks that might need insuring—but the growth ambition comes after attempts to lower costs and refine processes.

“We’re genuinely at the beginning,” he said, suggesting that the actuaries already know this to be true. “When you watch your companies make announcements about AI work, I’m sure you snicker a little because you know it isn’t that much yet… Often, it’s a case of the leadership team doing a deal with an LLM and saying, ‘We’ve got it licked,’ when in reality, the actual processes that you engage in to create a trusted product are unchanged, largely.”

‘I Lent My Reputation to It’

Before elaborating on why the industry’s repeating pattern always starts with cost cutting, McGavick explained why he feels qualified to deliver any predictions about AI, describing two levels of involvement: as a hedge fund executive investing in AI, and as non-executive chair of a company that delivers insurance-specific agentic AI to tackle process improvement.

After retiring from the insurance industry, McGavick served as co-chair of the operating board of directors for Bridgewater Associates at a time when the large hedge fund was positioning itself as the lead thinker around AI in the investing world, having made early investments in OpenAI and Anthropic. “They already have multiple billions of dollars being managed by AI by itself with some guardrails around it for regulatory purpose,” he added.

At Bridgewater, McGavick recalled sitting in on a meeting where participants argued about the future of language models—whether the Anthropics and OpenAIs of the world would ultimately prevail across all industry sectors, or whether smaller domain-specific language models would operate sector by sector. At the same time, XL Catlin’s former leader of IT, Martin Henley, had McGavick’s ear, asking for help with a new company he had been working to set up for several years. The company, mea Platform, is premised on the idea that the dsLM construct makes more sense for insurance.

Related article: Former XL CEO McGavick Returns to Insurance With AI Firm Mea Platform

To McGavick’s mind, there’s going to be a meeting in the middle. “The LLMs are trying to boil the whole ocean of language to find learning and then are drilling down toward the ocean floor where the actual economic activity takes place. … They’re going to cover the ocean—a handful of them because there’s not enough money, not enough energy, not enough resources for there to be more than a handful…

“But down where the economic activity is handled—by people like us trying to create insurance products that help people—[the LLMs] lose their way. They can’t use the language we use. Our language is harnessed for specific purpose,” he reasons.

Small language models, specific to industry sectors, are going to grow up from the ocean floor. They’re going to meet the LLMs somewhere and they’re going to be very profitable.”

Offering proof of how strongly he believes this, McGavick said, “I lent my reputation to it” through a role as advisor and non-executive chair on the AI-powered insurance workflow automation platform mea. “I’m fully invested. I think this is a cool thing.”

‘We Should Be Ashamed’

Returning to his discussion of insurance industry patterns, McGavick gave his take on why insurers attack cost structures first when they react to new tech. “I believe that’s in part because we’re ashamed—and we should be,” he said, reporting that operational costs have represented 12 to 14 cents of every premium dollar for years.

Citing a figure from an Accenture report, McGavick noted that operational inefficiency costs the insurance sector about $32 billion a year. (Editor’s Note: McGavick cited the high end of a range presented in the 2002 Accenture report, “Poor Claims Experiences Could Put Up to $170B of Global Insurance Premiums at Risk by 2027,” which found that underwriters grappling with aging systems and inefficient processes spend 40% of their time on non-core and administrative activities—an annual efficiency loss of between $17 billion and $32 billion.)

“That is all money that should be going into the clients by virtue of loss costs, or into our underwriting functions to discover new products. There’s so much we should be doing with that and we aren’t. We’re wasting it.”

As insurers fight for cost advantages by launching big IT projects and hiring new workflow vendors “over and over and over,” McGavick said, “we’re running in place… because of the complexity of our product…We disappoint ourselves over and over.”

Optimistically, he predicted that “this time is going to be different” because AI attacks the problem of complexity in an effective way. “My expectation is that two or three platform providers are going to emerge who use AI just to run operations. None of the underwriting, none of the claim standards … They’re just going to hive off that whole operational level and make it work in whatever way that group of underwriters and claims handlers wants it to work.”

“It’s already happening,” he said, offering the example of data ingestion. Carriers spend an “unbelievable amount of money unraveling all the junk” that brokers drop at their doorsteps. The dsLMs “do it like that”—with accuracy rates well above humans, he said while snapping his fingers. “That’s attacking costs. That’s attacking speed to market, the ability to quote …”

“Everything changes,” he said, comparing the change ahead to one in the banking industry that saw Visa and MasterCard handle all payments. There are many “layers of insurance activity that simply have no commercial value as a competitive factor.” Language models can handle them, leaving humans to do what’s valuable.

“Language models all learn from repetition within spaces, and they start to think for themselves and solve problems,” he continued. “That is the perfect environment for agentic AI—repeatable processes that don’t have strategic value.”

McGavick suggested that insurance market dynamics are at play too. “We’re coming into a soft market. You don’t think everybody’s thinking about their expense structure? It’s the next thing you do.”

This Time Is Different

“We’re going to see real change because AI against the sector’s useless procedural projects is a no-brainer,” McGavick said.

A skeptical actuary asked for more proof during a Q&A session. The actuary countered that prior solutions—data analytics and blockchain—were supposed to improve submission ingestion headaches.

Why didn’t it happen and why will AI be different?

McGavick explained that misaligned incentives prevented the prior solutions from taking hold.

All the other solutions required submitters to do extra work upfront. “You had to convert [information] into a blockchain … Brokers aren’t incented to do that. They’re not going to take more costs. [But] they know you’re incented to sort that bag of junk to have a chance of writing a piece of business. So, the trash gets passed across the chain [into] the insurer’s bucket,” he said.

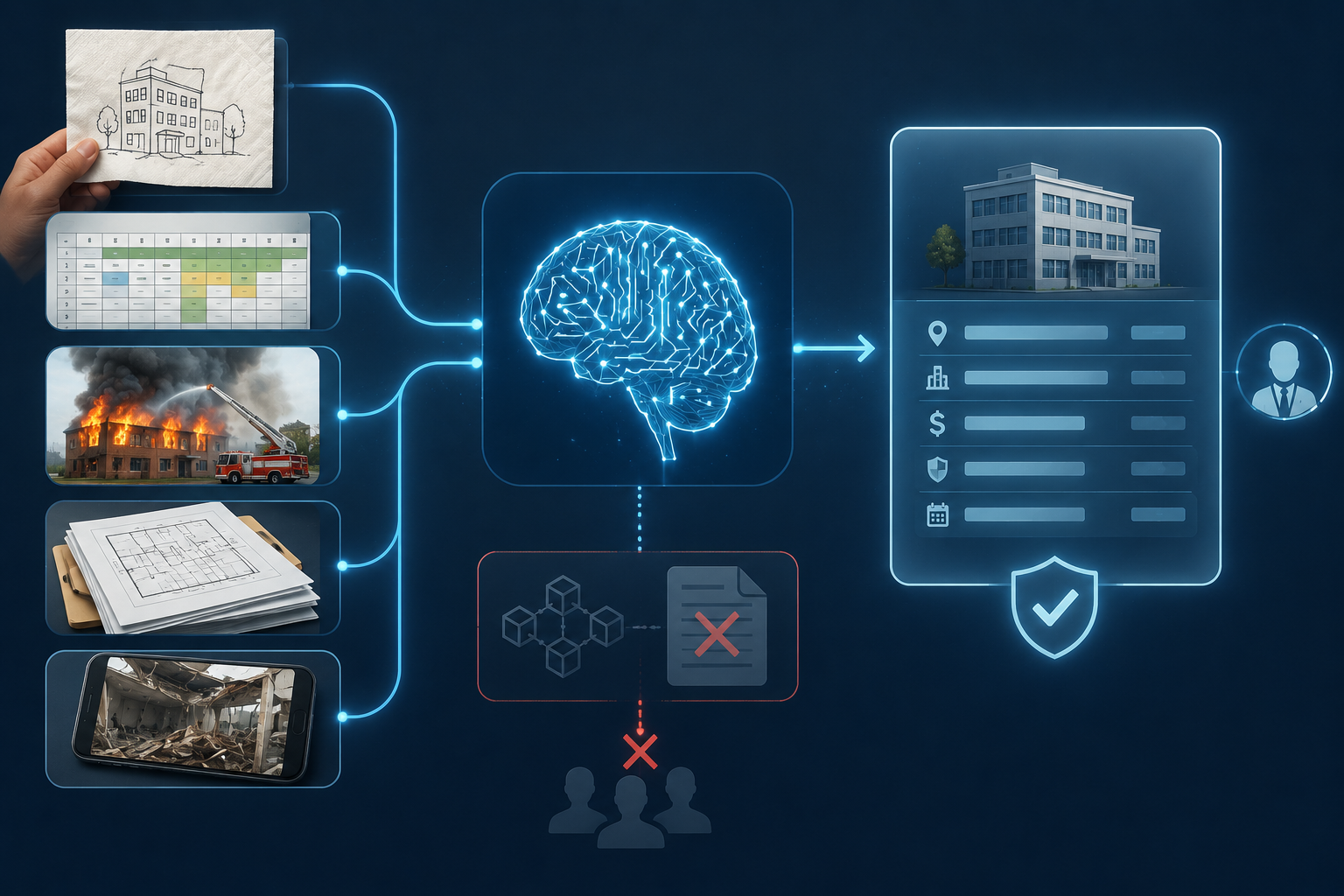

AI will be different because the dsLMs and insurance-specific “knowledge graphs” at the heart of emerging AI platforms can tackle “unbelievably nuanced and complicated” language and physical media of ingestion—encompassing everything from “a napkin with a drawing to an Excel sheet to a photo to a description.” (Editor’s Note: Various online sources define “knowledge graphs” as networks of connected information that show how people, places, things and concepts relate to one another, providing context for AI agents.)

AI will be different because the dsLMs and insurance-specific “knowledge graphs” at the heart of emerging AI platforms can tackle “unbelievably nuanced and complicated” language and physical media of ingestion—encompassing everything from “a napkin with a drawing to an Excel sheet to a photo to a description.” (Editor’s Note: Various online sources define “knowledge graphs” as networks of connected information that show how people, places, things and concepts relate to one another, providing context for AI agents.)

He continued: “These small domain language models can figure that out because that’s their language they work with. They can literally sort that random photo into a useful underwriting submission according to the demands of your underwriters.”

Turning to insurers’ repeated attempts to harness new technology to refine the processes core to their businesses and strategically differentiate them—underwriting, capital management and claims handling—from the process improvement phase of the patterns he introduced during the keynote, McGavick returned to the inefficiency that AI can eliminate. “Do you know your underwriter spends [almost] 40% of their time on handling office administeria?” he asked (likely citing Accenture research, “AI Underwriting: Beyond the hype | Insurance Blog | Accenture which puts the 2024 figure for non-core tasks and administration at 35%).

“They’re our product geniuses. They’re our risk gurus, and we’re making them move spreadsheets around. Have we lost our minds?”

“Imagine a world where they got the information they wanted in a clean way and were able to create configurations for how to underwrite quick, how to underwrite slow—and all they thought about was developing new products for their clients. Imagine that world. That’s the world we should live in,” he continued, offering that same type of world for claims handlers who can work with armies of AI agents.

Living the Dream: Underwriters and Actuaries

Starting the Q&A session, Stephanie Gould Rabin, an actuary and founder who moderated the panel, asked McGavick to imagine being an underwriter in 2035. “It should feel like a dream experience in which at the end you’re still in the most powerful position,” calling the shots on where risk goes and where to allocate capital, he said. “You’re going to wind up with a radically simpler ability to get information that you need to make a judgment.” And an “army of super-intelligent extensions of your own thinking” will anticipate “where you’re going to go.” They will “go out in the great world of knowledge and, with some freedom to interpret, come back to you with insights that you may not have thought of—and challenge you to think about them and add into your process.”

Repeatedly, McGavick asked, “How do we actually execute that promise as against all the challenges inherent in a distrusted industry?” And he answered that actuaries need to take up the challenge.

After cutting costs and re-examining processes, the industry is going to turn its attention to solutions for “risks that are growing so fast that we can’t get our heads around them. And the people who will create trust in all of that happening are sitting in this room…”

“If I use the word model, it’s the actuary in the end that’s going to be telling the rest of us in the leadership team, in the regulatory world and in the political world, what can be trusted and what cannot.”

Images (other than McGavick photo) are AI-generated (ChatGPT)

Diversity Crackdown Reverberates Throughout U.S. Boardrooms

Diversity Crackdown Reverberates Throughout U.S. Boardrooms  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Home Trend Report: Severity Reaches All-Time High, Frequency Declines

Home Trend Report: Severity Reaches All-Time High, Frequency Declines  Fitch Warns AI Market Correction Emerging as Major Global Credit Risk

Fitch Warns AI Market Correction Emerging as Major Global Credit Risk