State Farm Tops List of Large Insurers Providing Satisfying Shopping Experience, While The Hartford Ranked Highest Among Midsize Insurers

Saving money is the primary focus of consumers searching for auto insurance, according to a new report released today.

Now in its 17th year, the J.D. Power 2023 U.S. Insurance Shopping Study highlights the increasing focus on cost as customers shop around for the best deal when it comes to auto insurance policies.

The study is based on responses from 10,845 insurance customers who requested an auto insurance price quote from at least one competitive insurer in the previous nine months.

U.S. auto insurers are struggling to retain customers in light of inflation and rising premiums. As shoppers tighten their wallets, interest in usage-based insurance (UBI) options is growing. The option, which uses telematics software to monitor a customer’s driving style and assign rates based on safety and mileage metrics, was offered to 22 percent of insurance shoppers and is purchased 18 percent of the time, according to the report. That’s up from a 16 percent offer rate and a 12 percent purchase rate in 2020.

When a UBI option is offered, the report found that customer satisfaction increases by 6 points.

“Auto insurance customers are starting to shop for insurance like they shop for gas,” said Stephen Crewdson, senior director, insurance business intelligence at J.D. Power. “They are taking a much more active stance in seeking out plans that fit their needs and their budgets, which could have a serious long-term effect on carriers that have been working for years to build lifetime value through bundling and other initiatives. In the near term, this shopping trend manifests itself in increased customer interest in usage-based insurance (UBI) plans and some reshuffling of market share among the top carriers.”

Auto insurance accounts for a steadily increasing share of consumer discretionary spending, as prices increased 14.5 percent in February 2023, a little over twice the rate of inflation (6 percent). The report found 44 percent of customers are price checking, while 42 percent say they are being spurred by a rate increase. Similarly, 41 percent of those shopping because of a rate increase reported their rate increased by 20 percent or more.

As shoppers consider their options, customer satisfaction has stagnated. The average overall satisfaction among auto insurance shoppers is 861 (on a 1,000-point scale), even though shopping and switching rates have increased in the same period, the consumer insight company found. The 30-day average shopping rate reached 13.1 percent in March 2023, the highest rate since June 2021 and well above the 2021 average of 11.4 percent. The 30-day average switch rate hit 4.1 percent in March 2023, which compares to an average of 3.4 percent for all of 2021.

Auto Insurer Rankings

Analysis of customer satisfaction among large auto insurance carriers indicates some reshuffling from last year’s findings, as Progressive gained market share as GEICO slowed, largely due to significant rate hikes by the latter.

GEICO raised its rates significantly above industry average throughout much of the second half of 2022, while Progressive raised rates in the first quarter of 2022 and then registered lower-than-average increases during the second half of the year. The report found that during the same period, Progressive posted a notable market share gain, becoming the second-largest auto insurer in the United States, ahead of GEICO and behind State Farm.

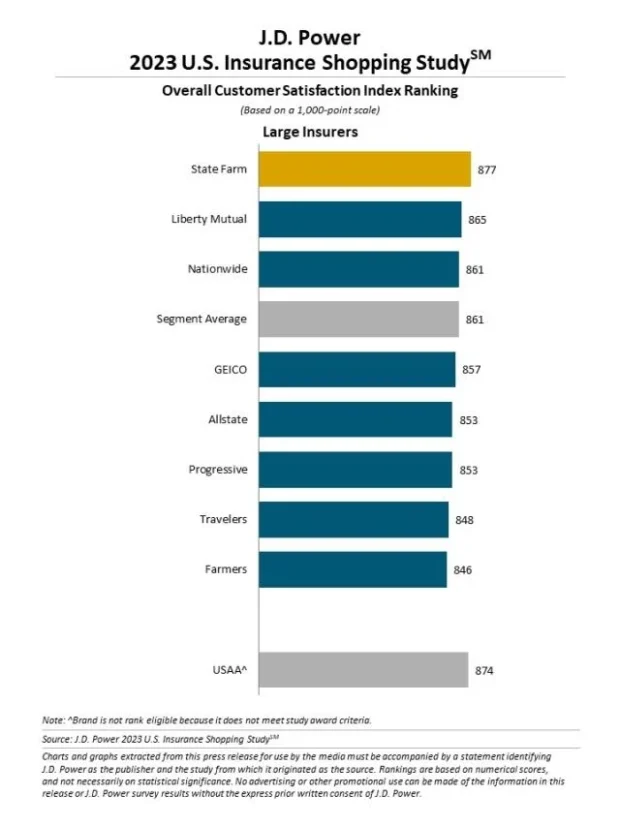

State Farm ranked highest among large auto insurers in providing a satisfying purchase experience for a third consecutive year, with a score of 877. Liberty Mutual (865) ranked second and Nationwide (861) ranked third. The segment average is 861.

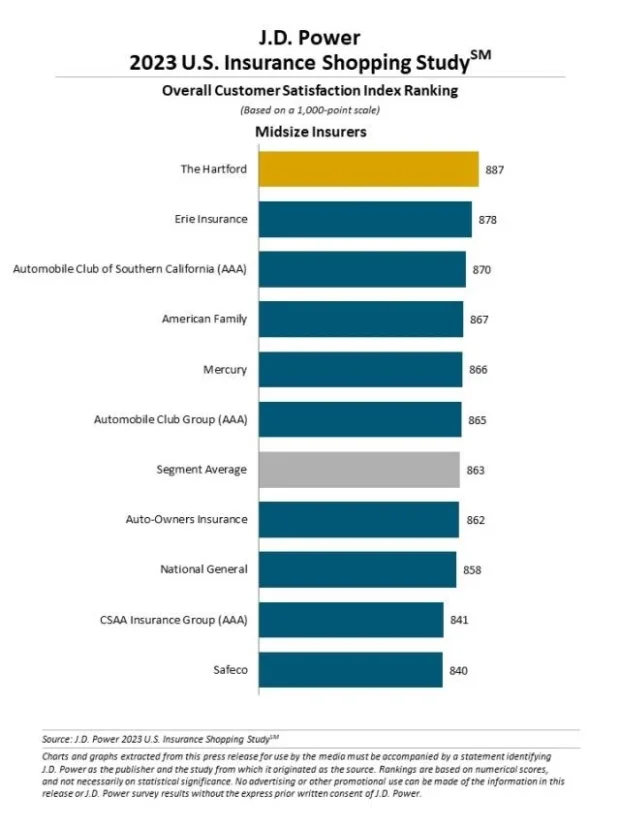

The Hartford ranked highest among midsize auto insurers for a second consecutive year, with a score of 887. Erie Insurance (878) ranked second and Automobile Club of Southern California (AAA) (870) ranked third, a spot previously held by Amica Mutual, a company no longer seen in the top market rankings. The segment average is 863.

Large insurers have direct premiums written of $4.5 billion or more in personal lines auto, while midsize insurers have direct premiums written of $1 billion-$4.499 billion in personal lines auto.

The study was fielded from March 2022 through January 2023.

More about the U.S. Insurance Shopping Study, can be found at https://www.jdpower.com/business/resource/jd-power-us-insurance-shopping-study.

Executives on the Move at AIG, HDI, Everest Group and The Andover Cos.

Executives on the Move at AIG, HDI, Everest Group and The Andover Cos.  Agent-Carrier Relationships Improving, Survey Shows

Agent-Carrier Relationships Improving, Survey Shows  USAA Not Done With Dividends: Florida Reforms Prompt $0.5B Payout

USAA Not Done With Dividends: Florida Reforms Prompt $0.5B Payout  Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?

Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?