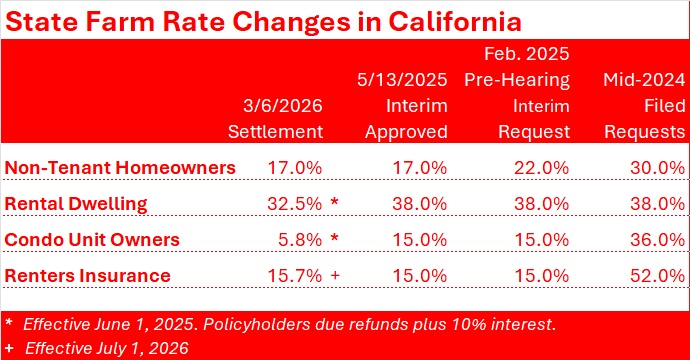

The long back-and-forth struggle between State Farm General Insurance Company, the California Department of Insurance and Consumer Watchdog is winding down, with the parties agreeing that an emergency 17% homeowners insurance rate hike will stand.

That 17% increase, and increases of 15% for renter/condo policies and 38% for rental dwelling (landlord) policies, were provisionally approved last May after an interim rate hearing, during which State Farm and CDI representatives argued that higher rate levels were necessitated by the ailing financial condition of the California affiliate of personal lines giant State Farm Mutual Automobile Insurance Company. The approval was contingent on the parent company putting $400 million of capital into State Farm General, and subject to a follow-up full rate hearing process that might prove the temporary interim increases to be excessive, requiring State Farm General to refund policyholders.

The three-party settlement agreement announced last week, potentially ending the full hearing process, does indicate that State Farm policyholders with rental dwelling policies and condominium policies will get some premiums refunded to them—plus 10% interest—because the parties have now agreed to rates lower than the interim levels, according to separate announcements from CDI and Consumer Watchdog. Rates for renter insurance policies, however, will be slightly higher than the previously approved figures, effective July 1, 2026, they said.

Both CDI and Consumer Watchdog, which served as intervenor in accordance with provisions of Proposition 103, announced the three-party settlement agreement late on Friday. State Farm has not posted an announcement about rates for residential property policies but did announce a 6.2% rate reduction for auto insurance of State Farm Mutual Auto in California earlier in the week.

The homeowners and other residential property policy rate agreements are subject to approval by an Administrative Law Judge and California’s Insurance Commissioner Ricardo Lara, who was not involved in the settlement negotiations in accordance with California’s rate hearing negotiations, CDI said.

If the proposed settlement stands, policyholders whose rates are being reduced will receive refunds with 10% interest retroactive to June 1, 2025.

Consumer Watchdog calculates that the refunds alone, excluding the interest due, will amount to $42 million—$35 million for condo tenants with State Farm General condominium insurance policies and $17 million for landlords with rental dwelling policies.

While the 17% non-tenant homeowners insurance rate hike of the three-party settlement agreement is equivalent to an interim emergency rate increase approved by the ALJ on May 13 last year, it is almost half of the requested increase State Farm General had originally filed for in June 2024 (30%). This means that even though the non-tenant homeowners policyholders are not getting refunds, as a group they avoided paying an extra $400 million in premiums, according to Consumer Watchdog’s calculations.

“State Farm originally sought staggeringly massive increases that were not supported by the data,” said Consumer Watchdog Litigation Director William Pletcher in a media statement last week. “This settlement substantially reduces those requests, secures refunds for some policyholders, and includes additional protections affecting non-renewals, claims oversight and future rate review.”

How We Got Here

Pletcher was one of many participants in an interim rate hearing last year, which began with State Farm General tempering its original June 2024 request for a 30% homeowners rate increase down to 22%. He argued that State Farm hadn’t actuarially demonstrated that its existing rate levels were inadequate.

During that interim hearing, representatives of CDI and State Farm General countered that if the requested rate hikes weren’t approved, some 680,000 homeowners with State Farm General policies and mortgages would be forced to pay more for inferior FAIR Plan coverage (and additional difference-in-conditions policies to fill in FAIR Plan gaps), anticipating that Standard & Poor’s would downgrade the insurer’s financial strength rating. They also warned that State Farm General could ultimately fail, and that the entire market would collapse in the absence of its biggest player, making homeowners insurance unavailable in the state.

Related articles:

- Is State Farm General Too Big to Fail? Calif. Rate Hearing Concludes (April 2025)

- Is State Farm General a Sinking Ship? California Emergency Rate Request Dropped to 17% (April 2025)

- California Commissioner ‘Provisionally’ OKs State Farm’s Rate Request (March 2025)

- State Farm, Consumer Group Battle Ahead of Commish Decision (March 2025)

- LA Fire-Related Capital Hit Prompts State Farm Emergency Rate Request (February 2025)

Ultimately, S&P did downgrade State Farm General by a total of four notches in two downgrade actions but never to the BBB level that industry representatives said could harm policyholders with mortgages when they testified on behalf of the insurer and the department during last year’s interim hearings.

Related articles: Another Downgrade for State Farm General: S&P Lowers Rating to A- (August 2025); Too Late? S&P Downgrades State Farm General (May 2025)

“Every mudslide, wildfire, major atmospheric river event…could open the floodgates to insurers demanding emergency interim rate hikes based solely on temporary financial setbacks or market fears,” Pletcher said during the interim hearing last year, countering a key argument from State Farm General that last year’s January wildfires were further weakening its already stressed financial condition.

Another Intervenor Reacts

One State Farm policyholder whose life was disrupted by the wildfires, Merritt Farren, petitioned CDI to intervene in the full rate review proceedings in June last year. Farren, who previously served as Associate General Counsel at Amazon and as General Counsel at Disneyland Resorts, lost his home in the Palisades Fire. (He did not participate in last year’s interim hearings.)

Like Pletcher, Farren intervened on behalf of consumers but surfaced different concerns in his motion filings—proposing changes to the regulatory rate review procedure that would allow an insurer’s claims handling and its treatment of consumers with claims to be used to determine whether sought-after rate increases are justified.

Related articles: Unpacking a Consumer Intervenor’s Novel Idea; The Good Neighbor

Farren was partly motivated to take this stance after witnessing the treatment of his neighbors in the aftermath of the fires. Although State Farm handled the claim for his home “expeditiously and fairly,” neighbors had faced extended delays, multiple document requests, claims denials for smoke damage and insufficient rebuild estimates.

More recently, Farren announced his candidacy for the position of Insurance Commissioner in the state. Believing his ongoing participation in the State Farm rate hearings while he is a candidate could present the appearance of a conflict of interest, he petitioned to remove himself from the proceedings. As a result, Farren did not take part in the settlement negotiations but has a positive view of the result.

“It did, in fact, provide State Farm a much, much lower increase than it had originally requested,” he told Carrier Management via email, when asked for his take on the pending settlement announced by CDI and Consumer Watchdog.

“It means that arguments that I made on how claims-handling practices should be considered in rate proceedings will have to wait for another day,” he added. “That said, the judge’s favorable decisions related to my arguments are now a matter of public record and my arguments will stand to be made again in the future.”

Related article: Unpacking a Consumer Intervenor’s Novel Idea

Farren added, “The fact that the Department has still not concluded or published its State Farm Market Conduct survey is unfortunate,” referring to an ongoing exam through which CDI is reviewing State Farm General’s claims-handling practices and compliance with California law. “That survey is, of course, separate from the rate proceedings, but for those who lost their homes in the fires, it’s still upsetting to see a rate increase approved with no action on importing the treatment of insureds,” Farren said.

The Latest Results and What’s Ahead

Beyond the stipulated rate increases and refunds, the new agreement includes provisions to address other issues raised during the interim and full hearing processes. Among them:

- State Farm General agreed not to implement new block non-renewals of homeowner policies during 2026 with respect to homeowners policies covered by the stipulation.

- Policies originally slated for non-renewal in a State Farm General filing in March 2024 must also continue in force, until the end of 2026.

- State Farm General must return for a new rate review no later than 2027, or within 90 days after its net premium to surplus ratio reaches 2:1, if that occurs prior to June 2017.

- When the company’s premium-to-surplus ratio reaches 1.5:1, as its financial condition improves, it will be required to provide a one-time 2.5% premium discount to renewing policyholders.

While State Farm hasn’t issued any specific media statements addressing the current financial condition of State Farm General, a late February announcement reporting full-year 2025 earnings for the group revealed that State Farm Mutual and State Farm General Insurance together have issued over $5 billion in wildfire damage payments for homes and autos—a figure that is expected to grow to $7 billion.

Across all of its property/casualty insurance businesses, State Farm booked an underwriting gain of $1.5 billion for 2025, representing a turnaround from an underwriting loss of more than $6 billion in 2024—and more than $10 billion of underwriting losses in each of the two prior years. The overall return to profitability prompted State Farm to announce a $5 billion payout of dividends to policyholders, even though the P/C businesses still reported a $3.1 underwriting loss for homeowners insurance.

Related article: State Farm Inked $1.5B Underwriting Profit for 2025; HO Loss Persists Feb 2026

Across the nation, State Farm reported $3.6 billion of underwriting profit related to auto insurance—and State Farm Mutual had enough profit in California to warrant a 6.2% rate cut, approved by CDI last week and scheduled to take effect on May 8 for new business and renewals.

As for State Farm General’s homeowners, tenant and rental dwelling rates, CDI said that filings of supporting declarations for the settlement agreement with the ALJ should be complete by around March 20, and the department estimates that the ALJ decision will come around April 7. After that, Commissioner Lara will review the proposed decision and make a final decision.

For his part, as Farren moves ahead with his bid to become the next commissioner, he is running on a platform to make the state’s FAIR Plan obsolete and revive the private market.

Key pieces to the solution would be a new, state-organized reinsurance entity, CAL Reinsure, into which carriers would cede total losses from “community fires”—fires that destroy at least three homes. CAL Reinsure would be funded by a “community fire” component fee included on policies for all homeowners and renters in the state and payments of policy limits would be made within 30 days to victims of total loss from a community fire.

Read more about CAL Reinsure in the Carrier Management article, “Reinsurance Program Could Wipe Out Need for Calif. FAIR Plan: Legal Exec.”

Featured image: AI-generated (Microsoft Copilot)

Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns

Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Robotaxis Operating Without Manual Controls, Like Brake Pedals, Coming Soon

Robotaxis Operating Without Manual Controls, Like Brake Pedals, Coming Soon  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age