“It’s not going to be easy to just restart the growth engine.”

Berkshire Hathaway Chief Executive Officer Greg Abel was referring to a challenge ahead of auto insurer GEICO during the annual meeting of the conglomerate last weekend as he reviewed first-quarter results across all the insurance and non-insurance operations.

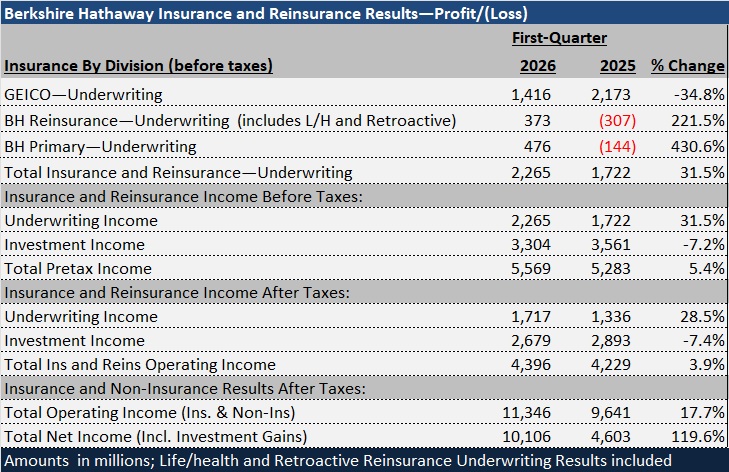

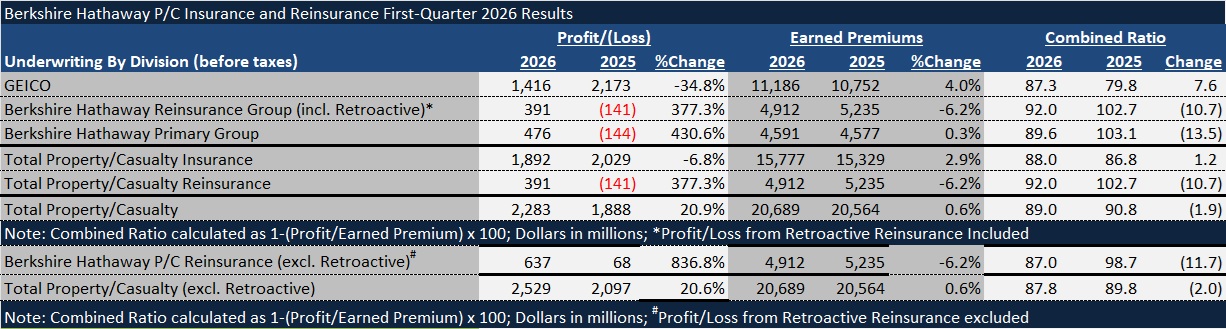

While GEICO’s first-quarter 2026 underwriting earnings before taxes totaled more than $1.4 billion, accounting for more than 62% of the total underwriting earnings across all of Berkshire’s insurance and reinsurance operations, the dollar figure was $757 million, or 35%, lower than GEICO’s first-quarter 2025 underwriting profit.

And GEICO’s first-quarter 2026 written premiums grew just 1.5% to $11.7 billion.

The Management Discussion and Analysis section of Berkshire’s first-quarter report said the small increase in premium volume reflected an jump in commercial auto business, partially offset by lower average premiums per policy for private passenger auto insurance.

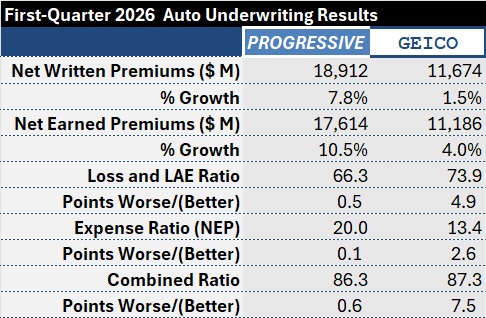

Abel discussed another contributor to lagging premium growth, reporting that policies in force as of March 31, 2026 grew by just 2% above the total in force at the end of March in 2025. “Now, compare that to the No. 1 competitor in our industry, Progressive [which] grew by 11%,” he said, referring again to the PIF growth metric for personal auto.

Carrier Management compiled other comparative figures for the two competitors below.

Related article: Progressive Q1 2026 Income Up Nearly 10%

At the Berkshire meeting, Abel said that GEICO employees are charged with finding ways to balance among three key measures of success this year—the combined ratio, the rate of customer retention and PIF growth—at a time when competition in the auto insurance space is ramping up. Both he and Nancy Pierce, the CEO of GEICO, highlighted a particular focus on customer retention.

“What I’m really focused on is our customer loyalty and retention. We want to improve those,” said Pierce, who appeared in a prerecorded video projected during the meeting. “It’s a very competitive market right now. Everybody has come out of an unusual period out of COVID in regards to frequency and severity. So, I think everybody now, all of our competitors are in the mode to try and grow,” she said.

“The best way for us to grow is to retain every one of our customers,” said Pierce, who also reviewed the 90-year history of GEICO, its commitment to delivering competitive prices and strong service, its culture centered on integrity, reputation, and “doing the right thing for customers” across all 50 states. She also reflected on her 40 years with the company, starting in as a claims associate after college.

Griffith joined Progressive as a claims representative in 1988. Throughout her 38 years at Progressive, she also served in managerial and executive positions in claims, as chief of human resources, as president of customer relations and as chief operating officer before becoming CEO in 2016.

Pierce, who became CEO of GEICO in December of 2025, started as a claims associate in 1986, “right of a college,” and has since worked in “almost every department or every sector that GEICO has,” she said during a 2026 annual meeting video, listing roles in claims, pricing, product management, and underwriting, as well as stints leading operations in different parts of the country.

Like Griffith at Progressive, Pierce was COO of GEICO before stepping up the CEO position late last year, when former GEICO CEO Todd Combs left to join JPMorgan Chase & Co.

Abel praised Pierce and the GEICO team for the “exceptional” 87.3 first-quarter 2026 combined ratio result, noting that the ratio reveals that more than 12% of underwriting income came from each dollar of earned premium.

A driving force behind a string of first-quarter combined ratios averaging roughly 83 over the last three years was a recognition by the GEICO team that the carrier wasn’t getting the proper rate for risk, and its work to align the two, Abel reported. Correcting the problem “meant our premiums went up for our customers across certain classes of drivers. They worked hard to segment that customer,” he said, explaining to Berkshire shareholders that similar moves were made across the auto insurance industry.

Related articles: Staff Cuts Help Fuel GEICO Profit; Not ‘Pouring Money’ Into AI: Jain (2025); Berkshire’s ‘Most Important’ Biz Drives Q1 Results; GEICO Still Behind on Tech (2024); Progressive ‘Crushing It’ on Profit: Berkshire’s Jain and Buffett (2021)

(Editor’s Note: GEICO, writing directly, retains an expense ratio advantage over competitors. In recent years, GEICO lowered its expense ratio further by cutting staff, Berkshire Vice Chair of Insurance Ajit Jain revealed at last year’s annual meeting, highlighting the corresponding benefits to GEICO’s overall combined ratios.)

The result: Not only have profits fueled more aggressive competitor behavior this year to attract customers, but customers have been shopping to find lower insurance prices, he said.

“Anytime you increase a customer’s insurance premium, and especially over a period of time— I’m talking about both GEICO and our competitors—listen, people start evaluating and shopping. And we’ve seen unprecedented shopping activity across the auto space,” Abel said.

Competitors are also “pursuing the GEICO customers” with advertising, he said.

Abel continued: “There’s an important balance I want to highlight to all of you. Yes, we have to get the price to risk right, but there’s two other important things we really need to balance. The second piece is we really do want to retain our customers…. And then the third piece of that balance is to grow GEICO.”

Expanding on the second goal, Abel said, “There’s no more valued customer than our GEICO customers. Many of you as shareholders and owners of Berkshire are GEICO customers. We want to retain all of you. We want to retain every GEICO customer.”

Having found the correct price for each risk, Pierce and her team “have that as a clear objective and they’re working hard on that,” he said, referring specifically to the retention goal.

As for growth, offering up the GEICO 2% PIF growth comparison to Progressive’s 11%, Abel said, “It’s not going to be easy to just restart the growth engine. We acknowledge that, but they [the GEICO team] understand the objective.”

“As we go through 26 and into 2027, two important objectives they have [are] let’s retain our customers and let’s start growing GEICO again,” he concluded.

Primary Insurance and Reinsurance Results Improve

Abel started his Berkshire business update by noting that the overall improvement in first-quarter 2026 underwriting results—a 2.0-point reduction in the combined ratio across all the property/casualty insurance and reinsurance operations—contradicted statements that he made in his February annual letter to shareholders. In the letter, Abel projected that Berkshire Hathaway was unlikely to see stronger insurance results in 2026.

While the annual letter had focused on GEICO’s dual problem of restoring retention and maintaining discipline, a first-quarter earnings scorecard projected on a screen in the Omaha arena showed improvements of more than 10 points for both Berkshire Hathaway Primary Group (the P/C primary insurance operations other than GEICO) and Berkshire’s P/C reinsurance operations.

Related article: What Berkshire’s CEO Abel Said About Insurance

Abel explained that higher underwriting profits for these groups were the result of lower catastrophe losses, noting that Berkshire incurred an $860 million after-tax charge associated with property catastrophes last year, including the January 2025 California wildfires. “Our 2026 results do not reflect any catastrophic events …. There were some storms in the Northeast part of the United States, but relative to 2025 and past years, it was very benign,” he said.

“The last time there was a hurricane that hit landfall in the U.S. was 19 months ago. So, our quarterly results, our results for last year do not reflect those types of outcomes. That means we have more capital coming into that industry.”

“Yes, we like those results, but the reality is, as our insurance business softens and we cannot realize the value we should for the related risk, [then] we start writing less premium.”

Translation: Premium growth will be hard to achieve outside of GEICO too.

Translation: Premium growth will be hard to achieve outside of GEICO too.

“We still want to write [business] at an underwriting profit because there’s still opportunities there. And there’s a number of risks we’ll insure. But we’ll be much more cautious, specifically across the primary and reinsurance businesses,” Abel stated.

Premium growth figures included in the first-quarter financial report bear this out.

- Written premiums for the Primary Group in first-quarter 2026 grew just 1.0% over last year’s first-quarter, reaching about $4.5 billion in total across operations that include RSUI, NICO Primary, MedPro, Berkshire Hathaway Specialty Insurance and Berkshire Hathaway Direct.

- Individually, RSUI and NICO Primary both reported declining premiums—down 14% for RSUI, with the drop primarily related to property business, and down 7% for NICO Primary, reflecting declining commercial auto writings.

- Premiums written for the P/C reinsurance operations fell 2.3% to roughly $6.0 billion, with the decline primarily attributable to volume reductions in property reinsurance business, partly offset by increased casualty business and favorable foreign currency translation effects, according to the MD&A section of the first-quarter 2026 report.

GEICO’s Technology Transformation

In Abel’s February letter to shareholders, his report on GEICO included another bit of information: “Alongside retaining its customer base with a more nuanced pricing strategy, GEICO is investing in technology to improve efficiency and service, while preserving its position as the industry’s low-cost provider.”

During the annual meeting over the weekend, Berkshire’s CEO interrupted himself during a discussion of results for Berkshire’s BNSF railway to describe a “technology transformation” at GEICO, which he suggested could offer learnings to BNSF and other Berkshire businesses that find themselves behind sector peers on technology.

Related article: Progressive ‘Crushing It’ on Profit: Berkshire’s Jain and Buffett (2021)

Abel recalled hearing about how GEICO’s technology-build supported its price-to-risk and customer-segmentation goals during a meeting of the Berkshire management team four years ago. “What I heard in that discussion was a clear technology transformation that was happening at GEICO. It was obvious that the technology was going to be a big part of the solution as GEICO tackled certain challenges,” he said, noting in addition to GEICO’s operational and commercial teams, the tech team was in attendance.

“Many of you as shareholders and owners of Berkshire are GEICO customers. We want to retain all of you. We want to retain every GEICO customer.”

Greg Abel (AP Photo/Nati Harnik, 2018)

Abel hung back as the meeting wrapped up to learn more from the tech team about what was changing. “First and foremost, we recognized we were going to become a builder of technology rather than just a buyer of technology,” he said, starting to summarize what he heard. “We had a number of systems, and we often bought the related applications or software that came with it. And yes, it’s a valued application, but it was disconnected from all our systems…. We didn’t have that ability to then use the information, get to the data,” he said, noting that the solution involved “simplifying the infrastructure—making sure we would build what we needed ourselves and deliver solutions back to our customers, and we would have clear access to the data.”

Reported Abel, those sensible solutions don’t happen overnight. “We’re still on that journey at GEICO in Year 5,” he said.

The most senior leader of the team put in place to drive the transformation forward at GEICO has since taken on the lead role in the technology transformation at Berkshire Hathaway Energy, and serves as senior technology officer at BNSF, according to Abel, who went on to describe the need for different talent resources in all the operations.

“Now we’re hiring engineers. We hire developers in our technology group that help us start to build the solutions we need for these businesses. And it’s going beyond GEICO now. We still have our valued employees there, and they may be retraining or transitioning to other roles. But the reality is we need less people managing the applications and the software and more people building outcomes that our businesses need.”

‘Narrow AI’ and the Safeguards

Abel went on to report that AI is a big part of the transformation. “It’s effectively what goes on top of a lot of our systems. And that’s what they’re building. They’re using AI to build applications,” he said, referring to Berkshire’s tech teams.

“That’s all great, but we also know there’s certain risks around humanity,” he continued, going on to report governance and accuracy checks that provide comfort that AI risks to Berkshire’s businesses are minimized. Specifically, the tech team outlined three principles associated with the use of what they refer to as “narrow AI” at Berkshire.

First, while highly skilled engineers support the builds, “we still have our employees, our senior management team involved in implementing the recommendations that we then receive associated with the architecture or the framework they put in place. [As] important decisions are being made, there’s human involvement. Our managers, our employees are involved. That’s part of the governance that’s effectively in place.”

The second piece, which the tech team calls the safeguard, is essentially a check that AI outputs are repeatable within limited time frames. Abel explains: “If we ask for an outcome–we want a recommendation or an action, and we ask it now and then a half hour later, do we get the exact same outcome? If we can receive that same outcome, it’s effectively the safeguard. We know we’re utilizing that application properly. And importantly, it means we’ve got a defined data set that we’re comfortable with,” Abel said.

A day later, a marginally different answer will emerge as new information updates data sets. “But if we ask it [to] ignore today’s information and just focus on yesterday, [and] we get the same answer,” then we’ve safeguarded the system, he suggested.

Finally, Abel said the narrow AI has to be additive to Berkshire’s businesses. “We’re not going to do AI for the sake of AI. You can spend a lot of money in this area, and we need to know what we’re trying to achieve and [whether] we see a value proposition for the businesses,” he said, without disclosing Berkshire’s exact amount of AI spend for GEICO or other businesses.

Top featured image: AI-generated image (ChatGPT)

This Year’s SCS Loss Totals Will Fall Below Average: KCC Analysis

This Year’s SCS Loss Totals Will Fall Below Average: KCC Analysis  Rising Pro Boxer Killed While Riding Bicycle in Bizarre Texas Crash

Rising Pro Boxer Killed While Riding Bicycle in Bizarre Texas Crash  Secondary Perils Responsible for Virtually All 2025 Nat-Cat Insured Losses in North America: Swiss Re

Secondary Perils Responsible for Virtually All 2025 Nat-Cat Insured Losses in North America: Swiss Re  Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent

Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent