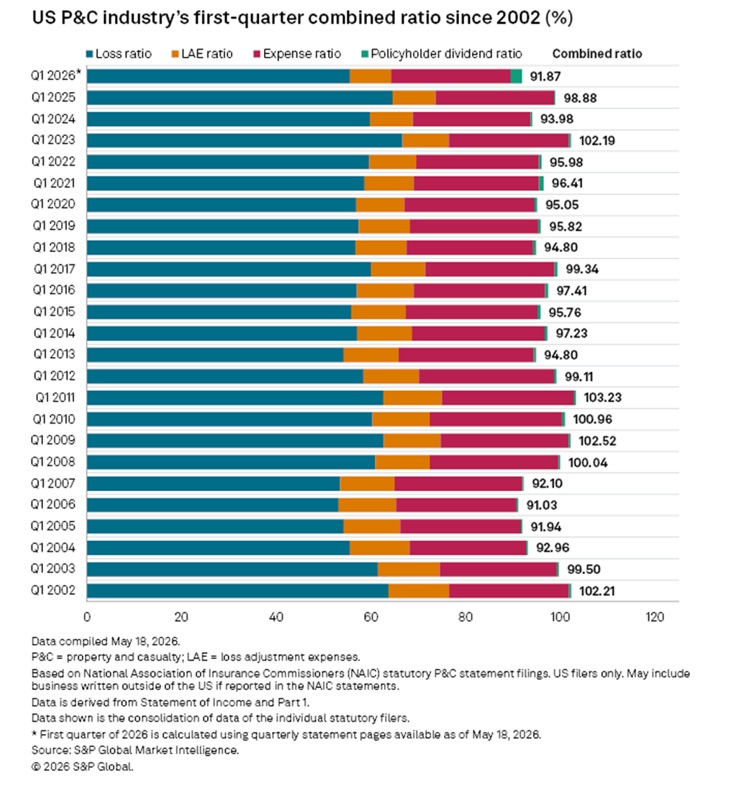

The U.S. property/casualty insurance industry posted another record in the first quarter of 2026, with a combined ratio of 89.5—before policyholder dividends—standing as the best first-quarter underwriting result in at least 25 years.

The insight comes from S&P Global Market Intelligence, which also said the first-quarter 2026 ratio including policyholder dividends was 91.9, better than any comparable result recorded since 2006.

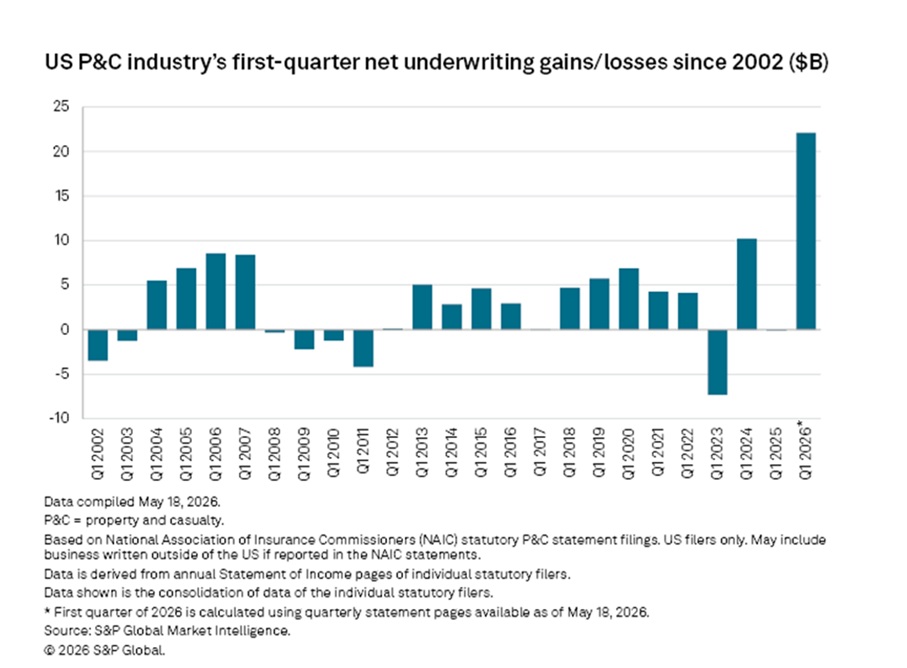

Translated into dollars, the underwriting gain is roughly $22.1 billion, a figure that was driven primarily by exceptional results in the homeowners multiperil and private auto lines, according to S&P GMI.

The result comes amid heightened competition in key markets and ongoing challenges in certain casualty segments, S&P GMI noted in a media statement.

Earlier this year, S&P GMI reported that the full-year 2025 combined ratio for U.S. P/C insurers, at just under 93, was also the best in nearly two decades, surpassed only by a 92.4 ratio recorded 19 years earlier in 2006.

Earlier this year, S&P GMI reported that the full-year 2025 combined ratio for U.S. P/C insurers, at just under 93, was also the best in nearly two decades, surpassed only by a 92.4 ratio recorded 19 years earlier in 2006.

Separately, S&P GMI analysts highlighted the “historically large” multibillion-dollar policyholder dividends being issued by State Farm and USAA based on 2025 results. The $5 billion from State Farm and $4 billion from USAA were “historically large” for the industry and the companies, S&P GMI analysts wrote in a March 2026 research note. The State Farm dividend was recorded in first-quarter 2026, pushing the industrywide policyholder dividend ratio for the quarter up to nearly 2.4—the second-highest ratio in 25 years, this week’s report notes. (In the second quarter of 2020, the dividend ratios was nearly 2.6, S&P GMI revealed in a report published yesterday, noting that several mutuals and reciprocal exchanges used dividends as a mechanism for rebating auto premiums during the worst of the COVID-19 pandemic.)

In the earlier note, S&P GMI revealed that the dividends for State Farm and USAA together put the dollar-level of industry dividends at a record high for this century.

Related articles: P/C Statutory Results: The Highs and The Lows; How State Farm, USAA Boost Customer Retention: Historic Dividends

As for the loss ratio component of the combined ratio:

- S&P GMI notes that first-quarter 2026 homeowners multiperil loss ratio shrank to 44.3, compared to a high of 102.3 for first-quarter 2025.

- Other property lines—fire and the property portion of commercial multiperil also showed significant improvements.

- The direct incurred loss ratio for private passenger auto business in the quarter was 60.4, only 0.6 points lower than first-quarter 2025, but 15.4 points lower than first-quarter 2023 when the industry faced rapid loss-cost inflation challenges.

Explaining the methodology for their analysis in a research report published on May 20 titled, “Outsized P&C profits persist as Q1 underwriting profit hits new high,” S&P GMI analysts note that the industry-level results for the first quarter of 2026 are an aggregation of individual company results filed with the NAIC available as of May 19. Results for prior first-quarter periods are S&P GMI’s previously published aggregations.

They also disclose the possibility that the first-quarter 2026 combined ratio before policyholder dividends could drift above 90 in coming week, noting that the May 19 data excludes significant workers compensation state funds, including California’s State Compensation Insurance Fund which recently reported a first-quarter 2026 underwriting loss.

They also note that quarterly results for New Jersey-domiciled entities are unavailable due to a state statute that deems those filings to be confidential.

According to S&P GMI, the biggest personal auto insurers–Progressive, Allstate, Berkshire Hathaway’s GEICO, State Farm, USAA, Farmers Group, and Liberty Mutual—all posted underwriting gains over $1 billion in this year’s first quarter. The report specifically highlighted State Farm, which posted nearly an underwriting gain of almost $2 billion, representing a swing of more than $7 billion from a wildfire-impacted underwriting loss of more than $5.0 billion in first-quarter 2025.

For the industry overall, the $22.1 billion gain tallied by S&P GMI from an aggregation of individual company results (filed with the National Association of Insurance Commissioners and obtained by S&P GMI as of May 19), is more than double the $10.2 billion reported in the last first-quarter with a large industry underwriting profit—Q1 2024. It also sits above an inflation-adjusted underwriting profit number calculated by S&P GMI from 20 years ago—$14.2 billion for Q1 2006, demonstrating unprecedented profitability levels.

“The industry faces significant headwinds including rapidly mounting competition in private auto, plunging commercial property rates, and persistent challenges in casualty lines where other liability loss ratios reached 65.8, the highest first-quarter result in 24 years,” S&P GMI said, also noting that the direct incurred loss ratio for commercial auto liability deteriorated to 71.1 in the quarter, up 3.2 points from first-quarter 2025.

Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?

Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?  This Year’s SCS Loss Totals Will Fall Below Average: KCC Analysis

This Year’s SCS Loss Totals Will Fall Below Average: KCC Analysis  Waymo Driverless Cars Crash Less Than Human Drivers: IIHS Study

Waymo Driverless Cars Crash Less Than Human Drivers: IIHS Study  Deja Vu as Berkley Calls Out MGUs During Quarterly Call

Deja Vu as Berkley Calls Out MGUs During Quarterly Call