A new report from S&P Global Market Intelligence is filled with information about record line-of-business loss ratios achieved in 2025—with some property/casualty lines coming in at record lows, and others reaching record high levels.

Not surprisingly, the highs occurred for commercial liability insurance lines. The lows were in personal lines, including the wildfire-impacted homeowners line, which benefited from the absence of landfalling U.S. hurricanes last year.

Ultimately, the lows outweighed the highs, according to the firm’s report on P/C insurance statutory financial results, “Spectacular P&C statutory profitability may prove fleeting.” But the real story of last year’s record results wasn’t personal vs. commercial lines but rather property vs. casualty, S&P GMI researchers pointed out in the report.

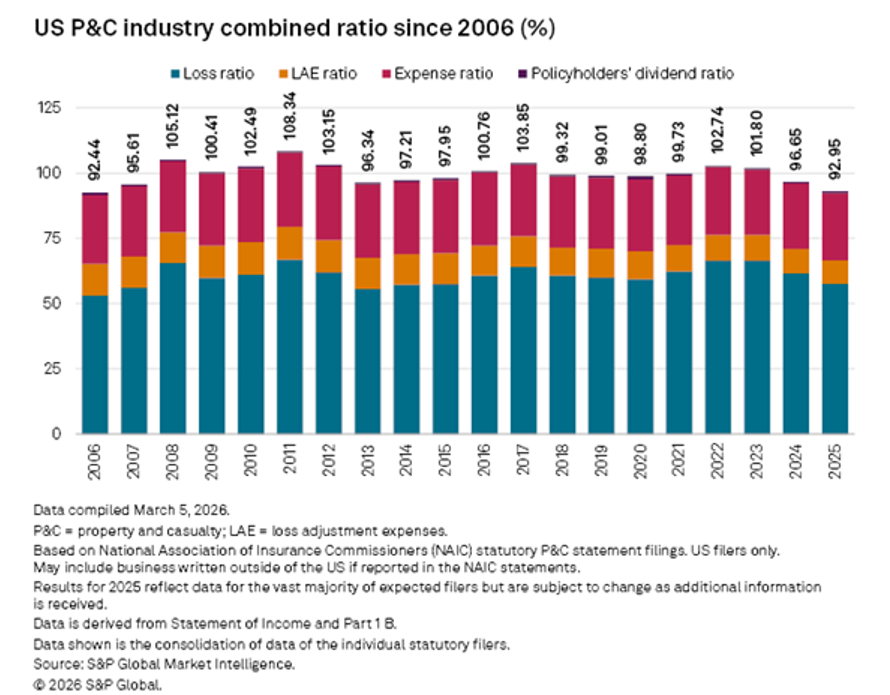

“We can say with conviction that the industry will not replicate these results in 2026, or, quite possibly, at any point in the foreseeable future,” wrote S&P GMI’s Jason Woleben, Tim Zawacki and Husain Rupawala in the report published on Monday. They noted that the 2025 underwriting results overall—the strongest in 19 years—were driven by a beneficial combination of “cyclical tailwinds, reduced catastrophe losses, and profit improvement plans.” Lagging premium growth and rising competition dim the prospects of a near-term replay, the report suggests.

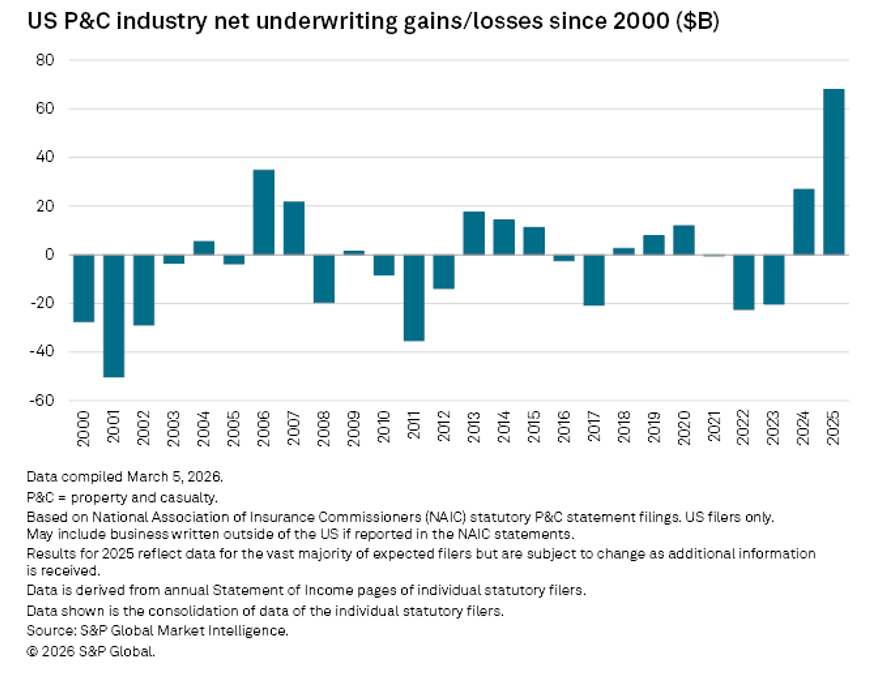

In dollars, the P/C industry’s net underwriting gain reached $67.9 billion in 2025, surpassing the inflation-adjusted profit of $54.2 billion in 2006.

The combined ratio was just under 93.0, only surpassed by a 92.4 ratio recorded 19 years earlier in 2006.

As for the line-of-business lows and highs, S&P GMI shared these research findings about 2025 net loss ratios:

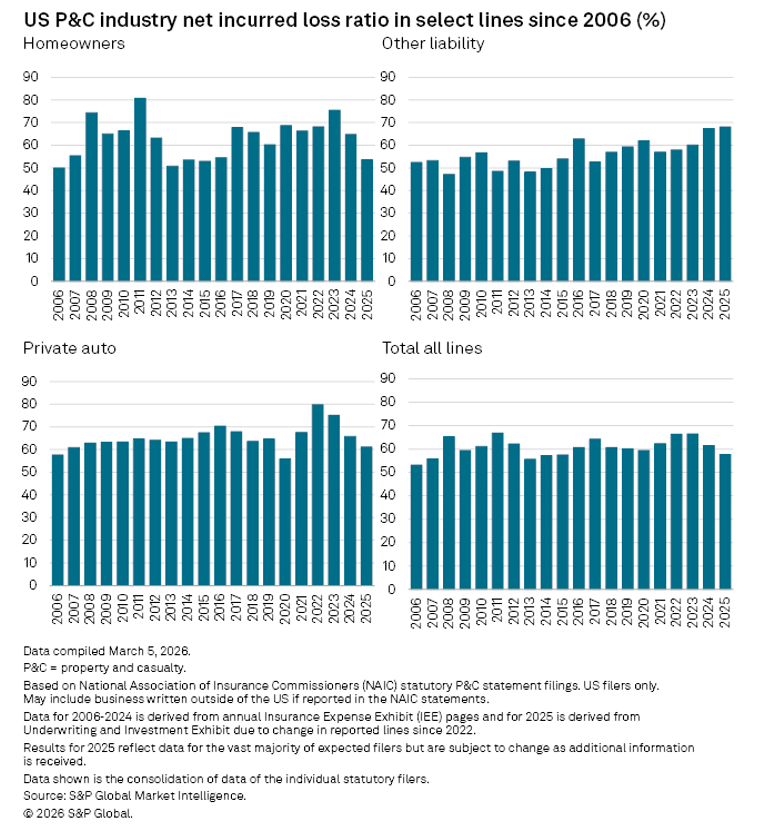

- The homeowners line net loss ratio was 53.7, 11.1 points better than 2024 and marking the lowest level since 2015.

- The net loss ratio for private passenger auto, coming in at 61.1 for 2025, was 4.7 points better than 2024 and the lowest net loss ratio for the line since 2020. In particular, the personal auto physical damage net loss ratio was 52.2, the lowest in at least 30 years.

- The net loss ratio for an S&P GMI aggregation of casualty lines increased to 66.7 in 2025. Among the lines, the loss ratio for other liability coverage reached a 21-year high of 68.0, and medical professional liability also topped out a 21-year high (57.9).

Notably, private passenger auto liability business came in at 67.9—hardly a record for the subline. While the result was 2.1 points less than 2024, according to the report the personal auto liability loss ratio has been lower than 67.9 in 20 of the last 30 years. This data point underscored the analysts’ point that the property vs. liability divide was more important than personal vs. commercial lines in terms of how overall 2025 P/C underwriting results played out.

“[E]ven as underwriting results on a total-filed basis improved to levels we may only see once or twice in our lifetimes, several commercial casualty lines showed noteworthy deterioration,” the S&P GMI analysts wrote.

“In addition to the unique confluence of circumstances that led to 2025’s outsized profitability, written premium growth is significantly lagging earned premium growth at respective rates of 4.9% and 6.3% as heightened competition returns to the private auto market and the scourge of social inflation is not going away,” they wrote, further explaining why the industry’s success in 2025 is unlikely to be replicated in 2026.

The report authors also commented on the timing of State Farm’s declaration of $5 billion in policyholder dividends, which would have lowered last year’s P/C industry results had it been recorded in 2025; an outsized underwriting loss for CNA Financial Corp. related to adverse reserve development, which is included in the 2025 results tallied by S&P GMI (without accounting for the benefit of retroactive reinsurance coverage from Berkshire Hathaway); and the possible impact of first-quarter 2026 East Coast winter storms on the homeowners loss ratio for 2026.

The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz