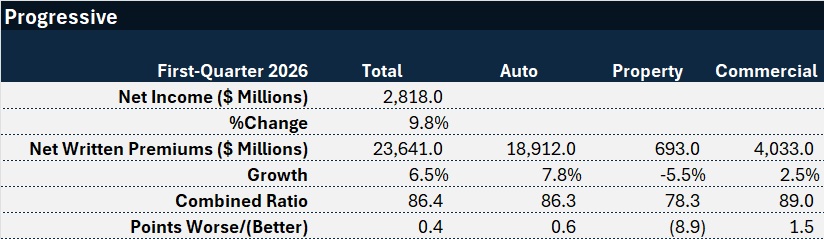

Progressive reported nearly double-digit growth in net income for first-quarter 2026, recording a bottom-line jump similar to the one recorded in last year’s first quarter, even as top-line growth fell to single digits.

According to Progressive’s March Results report published Wednesday, first-quarter net income was $2.8 billion, 9.8% higher than the $2.6 billion recorded in first-quarter 2025. Net written premiums across all coverages rose 6.5% to $23.6 billion, with the company’s biggest line—personal auto—growing 7.8% to $18.9 billion.

Policies in force as of March 31 were 9% higher than policies in force on the same date in 2025 across all lines. While policy growth for auto was almost 11% higher according to the latest report, property growth shrank 2%, down from 11% growth reported last year. Commercial lines policies in force as of March 31, 2026 were 3% above the March 31, 2025 reported commercial policy count.

Across all lines, the combined ratio for this year’s first quarter landed at 86.4, slightly worse than last year (showing 0.4 points of deterioration).

Property underwriting results improved, with lower catastrophe losses contributing to the 8.9-point drop in the combined ratio for the segment. Catastrophe losses added 12.5 points to Progressive’s first-quarter 2026 property combined ratio, according to supplemental information in the report, compared to 19.8 points in last year’s first quarter.

For personal auto, the combined ratio across the agency and direct books averaged to 86.3 by Carrier Management’s calculation, compared to about 85.7 for first-quarter 2025—moving less than a point. While the agency book continued to have a better combined ratio than the direct book in first-quarter 2026—82.8 vs. 88.9—the agency book experienced 0.9 points of combined ratio deterioration while the direct book combined ratio worsened by just 0.3 points.

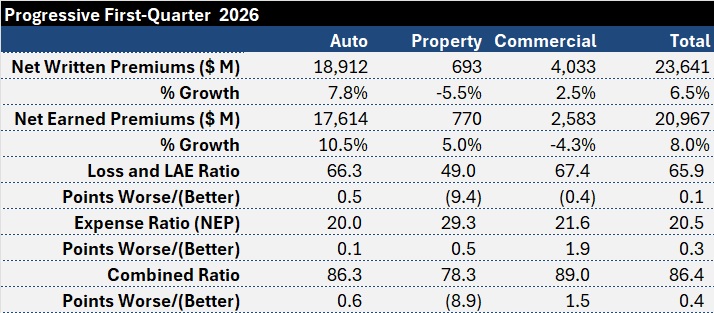

The chart below shows changes in the loss and expense ratio components of the combined ratio for each of the reporting segments and the company overall. Most movements in key ratios were less than a point. For auto, the loss ratio ticked up half-a-point and the expense ratio hardly budged.

The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Liberty Mutual Introduces Its Newest Brand Character: Liberty Biberty

Liberty Mutual Introduces Its Newest Brand Character: Liberty Biberty  A Matter of Trust

A Matter of Trust  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age