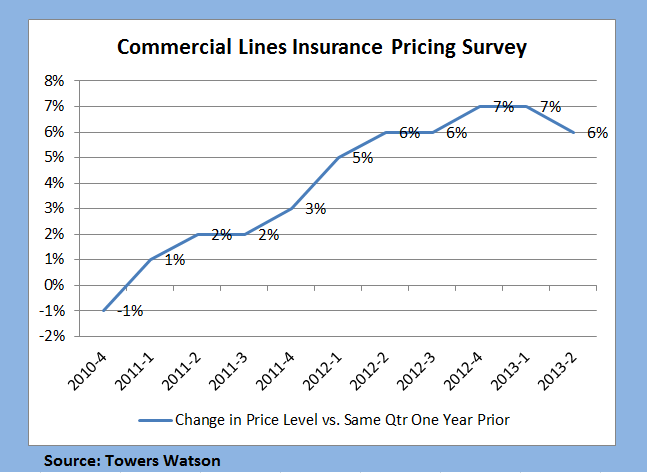

Commercial insurance prices rose by 6 percent in aggregate during the second quarter of 2013, marking the 10th consecutive quarter of price increases, according to the latest Commercial Lines Insurance Pricing Survey (CLIPS) conducted by global professional services company Towers Watson.

CLIPS compared pricing data reported by carriers on policies underwritten during the second quarter of 2013 to those charged for the same coverage during the second quarter of 2012.

Workers compensation and employment practices liability lines experienced the largest price increases year over year, as has been the case since the third quarter of 2012.

Price increases for most lines of business fell in the mid- to upper-single digits, with no lines having an overall price increase of less than 4 percent.

While still significant, price increases for commercial property insurance underwent a slight dip in the second quarter.

All account sizes for standard commercial lines showed price increases, with larger increases in midmarket accounts. In addition, companies using predictive models in pricing or underwriting saw higher price increases.

“As we expected, pricing increases in property insurance have tempered, consistent with the abundance of capital in the market. Given midyear reinsurance renewal pricing levels, I would not be surprised to see a repeat in the third quarter, especially if we continue to see favorable windstorm experience,” says Tom Hettinger, Towers Watson’s P/C sales and practice leader for the Americas, in a statement.

A line graph displaying the price changes that Towers Watson has captured for all lines together (dating back to second-quarter 2003) shows that each of the nine quarters prior to second-quarter 2013 had a price increase either better or the same as the quarter before. The 6 percent figure for second-quarter 2013, however, fell a percentage point below the first-quarter jump of 7 percent for all commercial lines taken together.

Historical loss cost information reported by participating carriers points to an improvement in loss ratios in accident-year 2013 relative to 2012 (excluding catastrophes), as earned price increases more than offset reported claim cost inflation for the second straight year. Carrier estimates of claim cost inflation continue to be moderate for year-to-date 2013.

CLIPS data are based on both new and renewal business figures obtained directly from carriers underwriting the business. Survey participants represent a cross section of U.S. P/C insurers that includes many of the top 10 commercial lines companies and the top 25 insurance groups in the U.S.

Source: Towers Watson

Deep Dive: Understanding Data Center Perils

Deep Dive: Understanding Data Center Perils  Two Trailers Containing $1.3M in Stolen Copper Wire Recovered in Illinois

Two Trailers Containing $1.3M in Stolen Copper Wire Recovered in Illinois  Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak  Reframing Like a Fox: How Insurance Leaders Can Catch Strategic Drift Before It Compounds

Reframing Like a Fox: How Insurance Leaders Can Catch Strategic Drift Before It Compounds