Property/casualty insurers in the U.S. that focused on difficult-to-place risks distanced themselves from their peers in key metrics measuring earnings, underwriting profitability, balance sheet growth and other indicators of success, according to S&P Global Market Intelligence.

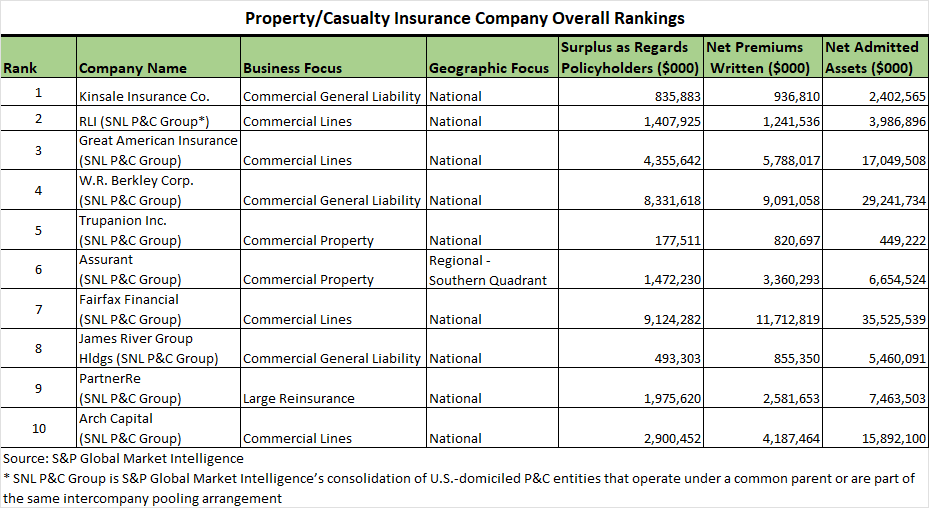

Kinsale Insurance Co., the Richmond, Va.-based primary operating subsidiary of Kinsale Capital Group Inc., ranked as the top performing U.S. property/casualty insurer, said the S&P Global Market Intelligence rankings, an inaugural annual report that evaluates the performance of the top 100 net written premium writers in the U.S. for the previous year.

The report said four of the eight top performers specialize in excess-and-surplus lines (E&S) business: Kinsale Insurance, RLI Corp., W. R. Berkley Corp. and James River Group Ltd.

Kinsale writes a diversified mix of casualty, property and professional lines business focused on small and midsize business customers. “Kinsale headed a list dominated by commercial lines writers in an outcome that reflects the highly favorable underwriting performance that industry segment delivered in 2022,” the report said. (See related chart).

“The U.S. commercial lines combined ratio of 94.4 for the calendar year was the best result since 2015, with profitability in the casualty lines, which accounted for a substantial majority of Kinsale’s premium volume, leading the way,” the S&P report continued.

“Specialty commercial insurers RLI Corp. and Great American Insurance (the name American Financial Group Inc. uses to conduct business) placed second and third, respectively,” the report said.

“Excess-and-surplus lines insurers, which focus on niche markets that require specialized underwriting expertise and risk appetite, continue to grow rapidly as they supply urgently needed property insurance capacity in coastal regions and remain leading providers of liability coverage for a wide range of unique risks,” said Tim Zawacki, principal research analyst at S&P Global Market Intelligence, in a statement accompanying the report.

“The U.S. Property and Casualty Insurance Performance Rankings, which gave several leading E&S carriers top marks for both growth and profitability, suggest that public and private investors’ recent enthusiasm for this business model has been well placed,” he added.

Personal Lines

The effects of inflation and natural catastrophes created one of the toughest environments in more than two decades for carriers focused on personal auto and homeowners insurance businesses, according to the section of the report covering personal lines, which “identifies those select carriers that managed to defy unusually steep odds.”

“The Progressive Corp., placed as one of only three personal lines-focused entities in the top 50, outperformed peers in one of the most challenging operating environments in more than a generation in its core private-passenger auto business,” the report said, emphasizing that the industry’s personal lines combined ratio of 109.9 was the highest since 2001. (Combined ratios above 100 indicate an underwriting loss).

Progressive ranked No. 1 among the 32 personal lines-focused entities reviewed in terms of return on statutory equity and No. 2 in return on average assets. Its operating ratio ranked third among the personal lines-focused companies. Progressive also led its personal lines peers in asset growth and placed second in surplus growth.

“During a year in which the private auto combined ratio exceeded 112 likely for the first time since the 1980s on an industrywide basis, Progressive ascended to the No. 2 position in terms of private auto market share while at the same time outperforming many of its rivals from an underwriting profitability perspective. While Progressive’s GAAP combined ratio straddled management’s 96 benchmark in its two private auto channels, its statutory performance relative to personal lines peers in the key profitability metrics we selected stood out,” the report noted.

Second- and third-placed personal lines writers American National Group Inc. and the group led by Arbella Mutual Insurance Co. Inc. showed top-quartile performance among personal lines-focused carriers from a rates-of-return standpoint, and they placed among the top five in the two metrics we use to measure relative underwriting profitability.

American National, a multiline carrier with business spread across personal and commercial P/C as well as life and annuity, became a subsidiary of Brookfield Reinsurance Ltd. in 2022. “It produced leading results among the personal lines-focused companies in the underwriting profitability and balance sheet growth metrics. With our rankings of personal lines-focused carriers based on the relative success of the entire P&C group, American National’s diversification paid off in 2022 as its loss and loss-adjustment expense ratio in the commercial lines was 13.8 percentage points lower than in the personal lines,” the report said.

On the other hand, the report said, the comparable lack of diversification across Arbella Mutual’s personal and commercial lines made its “presence on the personal lines podium particularly noteworthy.”

Arbella’s geographical concentration in the New England region helped account for its outperformance, S&P explained. “The group’s homeowners loss and LAE ratio of 48.3 percent was 28.9 percentage points better than the industry’s overall, excluding state funds and other residual markets in a year natural catastrophe activity was most significant in other parts of the country, particularly the upper Midwest and Florida.”

Other top-performing personal lines insurers in the S&P Global Market Intelligence analysis included CSAA Insurance Exchange; GEICO Corp.’s parent Berkshire Hathaway Inc.; County Financial; New Jersey Manufacturers Insurance Co. (NJM Insurance); Liberty Mutual Holding Co. Inc.; Farmers Insurance Group of Cos.; and Michigan Farm Bureau Financial Corp.

Methodology

The U.S. Property and Casualty Insurance Performance Rankings are based on statutory financial results collected and compiled by S&P Global Market Intelligence. They are determined using 13 financial metrics from 2022 statutory filings grouped into six buckets: rates of return, underwriting profitability, balance sheet expansion, investment performance, prior-accident-year reserve development and premium growth.

The categories are given distinct weightings to calculate performance scores for each of the 100-largest U.S. P&C entities based on 2022 net premiums written. Similar calculations are used to rank the largest entities determined by S&P Global Market Intelligence to have commercial and personal lines-focused operations. This breakout is intended to recognize standout performances by carriers operating in market segments where overall financial results faced significant macroeconomic headwinds.

Further details on the S&P Global Market Intelligence U.S. Property and Casualty Insurance Performance Rankings can be found here.

AI Pushes Underwriting Beyond Risk Selection to Prevention

AI Pushes Underwriting Beyond Risk Selection to Prevention  Deja Vu as Berkley Calls Out MGUs During Quarterly Call

Deja Vu as Berkley Calls Out MGUs During Quarterly Call  Deep Dive: Understanding Data Center Perils

Deep Dive: Understanding Data Center Perils  California Theft Crew Busted, Responsible for $1.3M in Stolen Vehicles

California Theft Crew Busted, Responsible for $1.3M in Stolen Vehicles