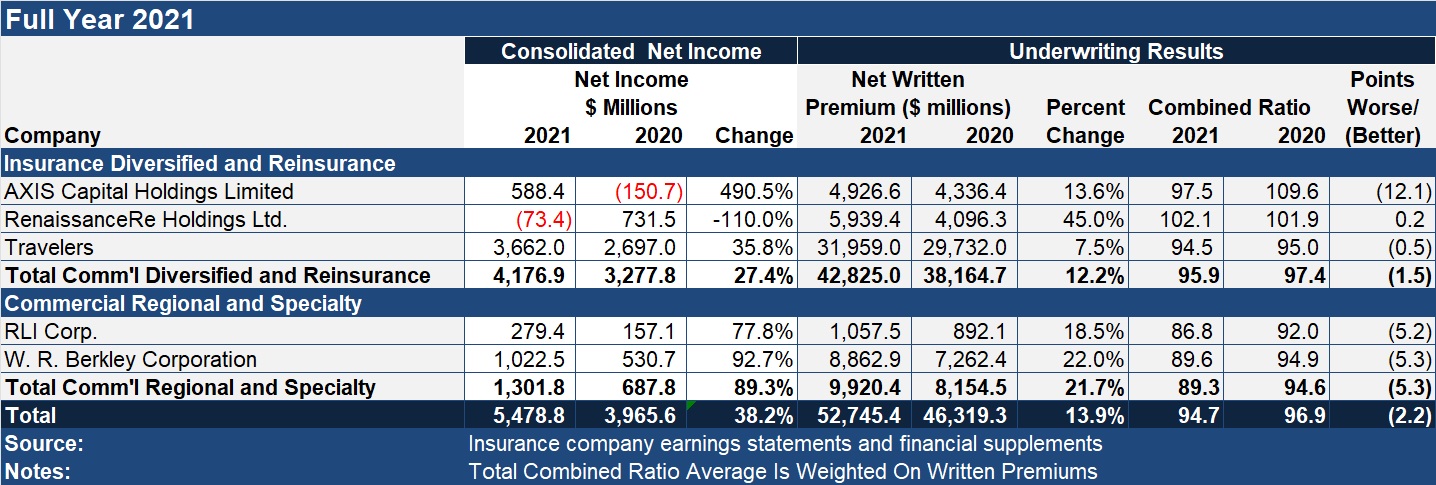

For publicly traded commercial insurers and reinsurers that reported 2021 earnings in January 2022, net income soared nearly 40 percent, with double-digit premium growth and higher levels of underwriting profit boosting bottom lines.

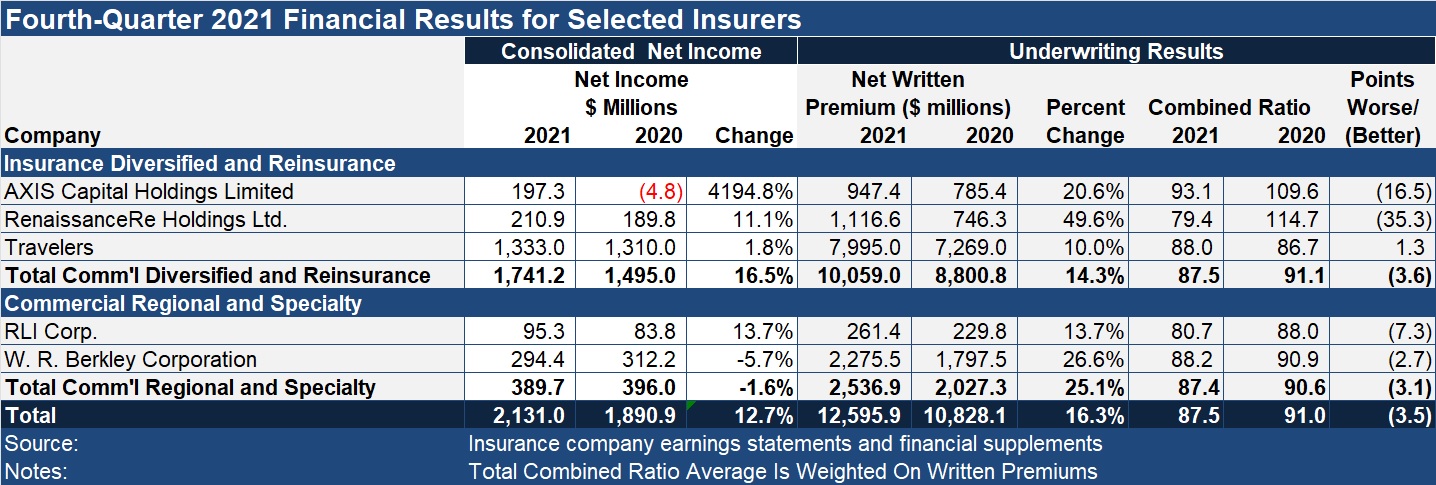

For the month of January so far, reports from five commercial lines insurers and reinsurers saw combined ratios decline almost across the board, with AXIS Capital showing the biggest combined ratio improvement of 12 points.

Executive Summary

Headline results from last week’s earnings conference calls from property/casualty commercial specialty insurers and reinsurers included reports of RLI’s 26th straight year of underwriting profits in 2021 and RenaissanceRe’s report of an operating profit in spite of incurring over $1 billion in catastrophe losses.Premium growth rates ranged from 7.5 percent for Travelers to an eye-popping 45 percent at RenaissanceRe—adding up to an average of almost 14 percent across the six-company cohort overall.

Last week’s reports came from RenaissanceRe (Jan. 26), AXIS Capital (Jan. 27), RLI Corp (Jan. 27) and W.R. Berkley Corp. (Jan. 27), with RLI and Berkley reporting sub-90 combined ratios, and AXIS reporting its best underwriting results in a decade.

At AXIS, efforts to shift the portfolio toward specialty insurance instead of reinsurance, and specific actions to reduce property and property-catastrophe reinsurance volume, were key drivers of a more than $700 million improvement in net income for 2021 over 2020.

AXIS was the only company in the group to report both red ink on its bottom line and an overall underwriting loss in 2020. RenRe was the only one to do so in 2021.

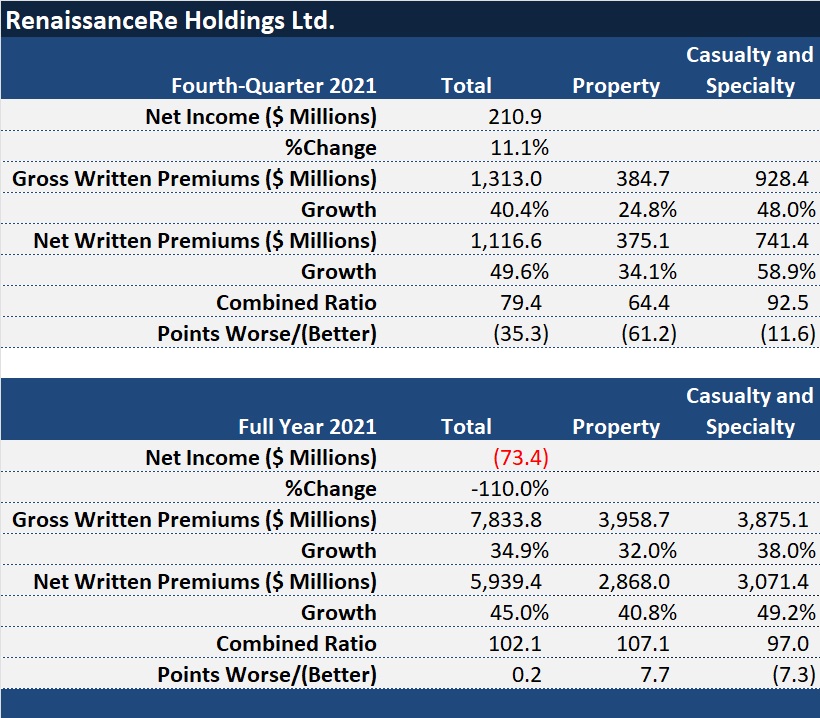

RenRe’s overall combined ratio worsened only slightly, however—by 0.2 points to 102.1, with a 7.3 point improvement in the casualty and specialty combined ratio helping to offset 7.7 points of deterioration in the property combined ratio. The reinsurer capitalized on opportunities to grow in a strong market, and in spite of incurring over $1 billion in property-catastrophe losses, managed to report an operating profit of $84 million, attributing the positive result to a diversified book of business and superior risk selection capabilities. (Editor’s Note: Together, the positive operating income figure combined with the impacts of net realized and unrealized losses on investments, net foreign exchange losses and related tax items resulted in a net loss of $73.4 million for RenRe in 2021.)

RenRe’s fourth-quarter income jumped more than 11 percent, with a property reinsurance combined ratio of 64.4, pushing the companywide combined ratio to 79.4—the best fourth-quarter combined ratio of any of the publicly traded reinsurers and commercial insurers reporting in January.

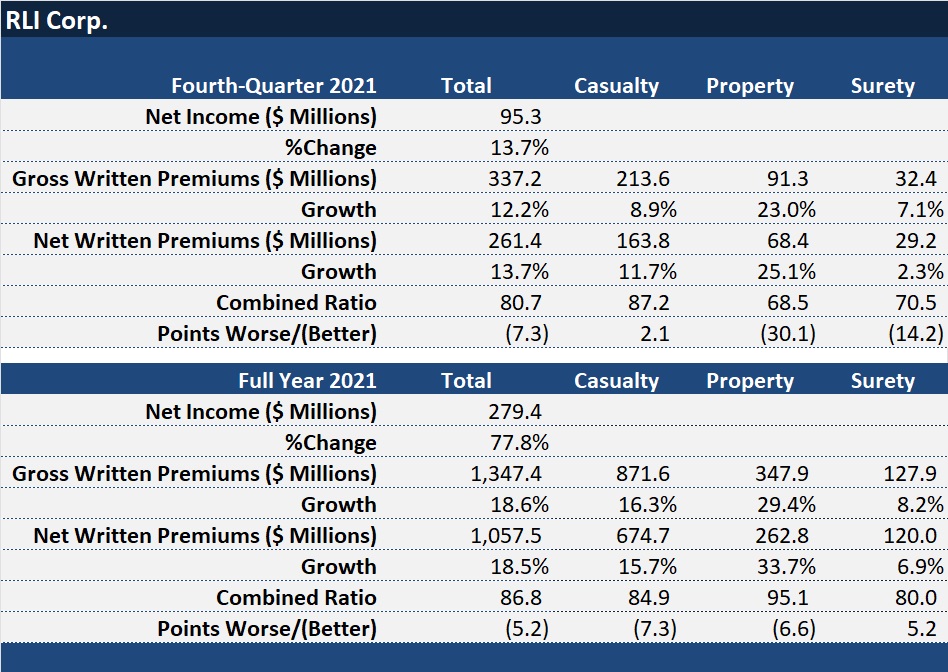

While ink colors changed for the full-year 2021 and 2020 financial reports at AXIS and RenRe, consistency was the dominant word on the lips of executives at RLI as they described the drivers of the specialty insurer’s 26th consecutive year of underwriting profitability. A casualty combined ratio of 84.9 and an overall combined ratio of 86.8 for the year were two key metrics that reveal the story of RLI’s continued financial success.

Highlights of the last week’s earnings conference calls, including market observations for 2022, discussions of two hot topics—cyber appetites and Jan. 1 reinsurance renewals—along with key growth and profit metrics for fourth-quarter and full-year 2021 are presented in summary form below.

Read more about Travelers, which reported a week earlier, in the Carrier Management article titled, “Travelers Leaning Into AI, Tech as Earnings Rise.” A separate article about W.R. Berkley’s earnings recap will be published later this week.

RLI: 26 Straight Years of Underwriting Profit

RLI’s 2021 fourth-quarter represented Chairman Jon Michael’s last quarter at the helm of the specialty insurer as chief executive officer. Craig Kliethermes, who took the reins as president and CEO on Jan. 1, described the final quarter’s results, ending a 26th straight year of underwriting profits for the company, as “emblematic of [Michael’s] track record of success during his 21-year tenure as CEO.”

Highlighting the milestones of Michael’s tenure, Kliethermes noted that RLI:

- Produced an underwriting profit in every year that Michael was CEO.

- Reported underwriting profits in 81 out of his 84 quarters over which Michael led the company. “a remarkable 964 batting average.

- Delivered total shareholder return over his tenure of over 2,100 percent, or roughly 16 percent annually, exceeding comparable benchmarks.

“Our portfolio of products is in good order, and our specialty footprint is broad. We are ready and willing to continue growing profitability where disruption and opportunities exist.”

Craig Kliethermes, RLI

Looking ahead, Kliethermes said, “Our portfolio of products is in good order, and our specialty footprint is broad. We are ready and willing to continue growing profitability where disruption and opportunities exist.”

“Recent catastrophe activity, rising labor, material and social inflation as well as rising reinsurance costs should provide continued pressure on rate levels going forward. We believe this is a market we can thrive in as rates are still moving up broadly, but it requires good underwriting selection to differentiate and truly understand the risk-reward equation,” he said.

Chief Operating Officer Jennifer Klobnak provided some of the details of factors driving an 18.5 percent jump in net written premiums last year, and Chief Financial Officer Todd Bryant reviewed the components of a sub-90 combined ratio that improved five points in 2021, including a very light fourth quarter for weather-related losses.

Klobnak said that casualty rates jumped 6 percent on RLI’s book in the fourth quarter, identifying double-digit increases for the D&O book as a primary driver. “Nearly all casualty products are still achieving positive rates in the mid-single-digit range,” she added, noting that personal umbrella, excess liability focused on the construction space, and transportation lines were standouts.

RLI’s transportation book, in particular, grew 10 percent in the quarter, including a 6 percent rate change, she said, noting, however, that with exposure levels rebounding, transportation claims are also increasing. “They have not returned to 2019 levels,” she said. “This is a trend we’re watching closely.”

Like Kliethermes, Klobnak referenced the favorable impacts of market dislocations on RLI. “We are benefiting from competitors continuing to provide lower limits than in the past, which creates opportunities for us to participate.”

- RLI executives said they put a large account cyber book into runoff.

- AXIS Capital reduced exposure and tightened underwriting, but notes that it’s book is making an underwriting profit.

- Reinsurer RenRe said the cyber reinsurance market is “particularly dislocated,” resulting in triple-digit rate increases during 1/1 renewals.

“The casualty portfolio is performing really well overall. We achieved 16 percent growth for the year on an 85 combined ratio,” she said, also revealing that RLI renewed reinsurance treaties support much of its casualty book at 1/1. “We saw mid-single-digit rate increases, and we characterize the reinsurance market as rational” for casualty, she said.

The real difference maker in results for the fourth quarter was a smaller part of RLI’s book—the property segment, she said, noting that a lack of catastrophe losses in fourth-quarter 2021, compared to the prior fourth quarter, pushed the segment’s combined ratio down more than 30 points to 68.5.

“The market in this segment continues to be challenged by losses, which we believe will support continued rate increases. Competitors are selling shorter limits than in the past, which creates room for us to participate on the insurance tower,” she said.

RLI’s gross property premium volume rose 23 percent in the fourth quarter and 29 percent for the full year last year. “All products in this segment saw an increase in submissions this quarter and for the full year,” she said at one point, highlighting growth in E&S property premiums, in particular, which grew by 34 percent in the fourth quarter. “We realized increased rates, witnessed rising building valuations, and saw reduced capacity from our MGA and carrier competitors. All of these changes improve our opportunity in this space,” she said.

During the Q&A section of the earnings call, analysts asked Klobnak to speculate on rate trends going forward in 2022, to report on the insurer’s cyber insurance appetite and to comment on the impact that inflation could have on future results.

The COO pointed to activity during 1/1 reinsurance renewals to support her view that rate hikes will continue in 2022. “My expectation would be that property will continue to have some support because I know…we paid a little bit more, and I expect everybody else did as well,” she said.

“On the casualty side, that [reinsurance] market seems to be a little more reasonable, but yet the reinsurers are charging more, especially for auto excess coverages. So, there should be some support there as well.”

As for the other hot topic, cyber, Klobnak revealed that while the carrier does continue to write cyber coverage at low limits for its small professionals book, RLI exited out of a cyber portfolio targeting large accounts within the executive products (D&O) group earlier this year. “It was not a large portfolio, but we are running off that part of the book,” she said.

Kliethermes added that the book put into runoff is heavily reinsured, putting the portion of the exposure reinsured at roughly 85 percent.

AXIS Capital: A Year of Repositioning

While RLI executives talked about consistent results building on successes of past years, at AXIS Capital, the word of the hour was “repositioning.”

“We begin 2022 as a stronger company than we were just a year ago,” said CEO Albert Benchimol. “In 2021, AXIS advanced its efforts to reposition the portfolio, manage down volatility and drive profitable growth while capitalizing on a favorable market,” he said.

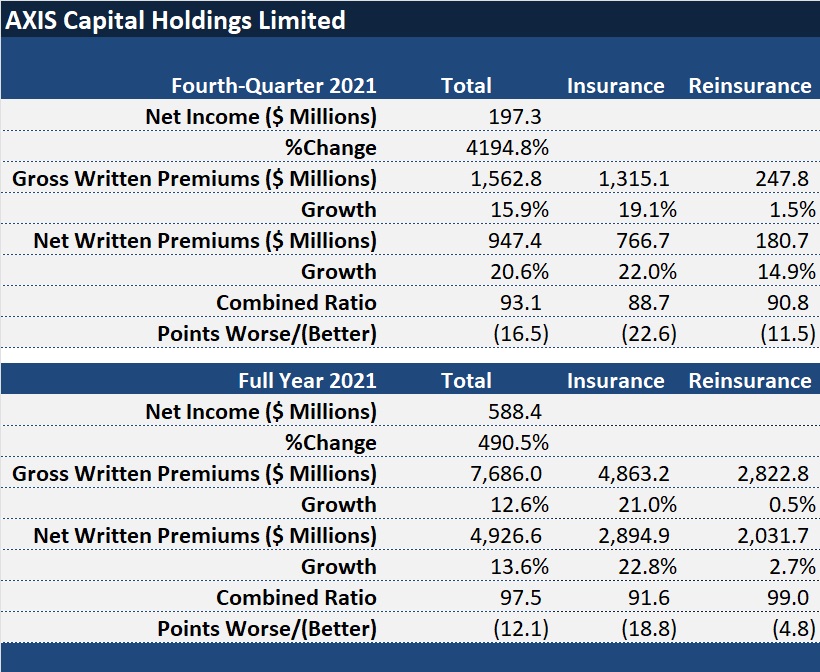

Benchimol attributed the company’s ability to record $588.4 million in net income for 2021 (compared to a $150.4 million net loss in 2020) and 12.1-point improvement in the full-year combined ratio to a “proactive reshaping of the portfolio, reduction of limits and modification of attachment points,” coupled with top-line growth in selected lines that the company believes are adequately priced.

The repositioning is seeing the hybrid insurance and reinsurance company tilt in the direction of insurance. “We’re confident that the business is on pace to establish its place among the top carriers in the specialty insurance sector,” Benchimol said during his introductory remarks.

On the other hand, Benchimol’s discussion of actions taken during the 1/1/2022 renewals gave conference call listeners a sense of what’s going on in the reinsurance side of the house. In spite of the fact that reinsurance segment combined ratio came in below 100 for 2021 (99.0 to be exact), during the first renewal period of 2022, AXIS “took decisive action and reduced our reinsurance property and property-cat premiums by 45 percent,” he reported.

2021 milestones for the company described by Benchimol and CFO Peter Vogt included:

- A 10-point reduction in the company’s current accident year ex-cat combined ratio to 88.7—the best since 2007.

- A catastrophe loss ratio that remained flat in 2021, in spite of the industry experiencing a $100 billion-plus cat year.

- Gross specialty insurance premiums rising 21 percent to $4.9 billion in 2021, or up 50 percent since 2017.

- A specialty insurance combined ratio of 91.6 in 2021—the best since 2010.

- A reinsurance current year ex-cat combined ratio of 86.3 in 2021—the best since 2012.

Benchimol said specialty now makes up 63 percent of AXIS Capital’s writings overall, and that by capitalizing on an “already well-established presence in some of the most attractive P/C markets today,” the proportion will rise to 70 percent in short order.

He also offered the company’s view of market conditions in the insurance and reinsurance sectors.

On the insurance side, he said that AXIS Capital’s average rate increase was 14 percent for both the full year and the final quarter, nearly identical to increases the company saw in 2020. “This represents the 17th consecutive quarter of rate increases and the seventh consecutive quarter of double-digit increases,” he said.

“The question on everyone’s lips is how long will it last. Looking forward, we expect that after many years of unsatisfactory performance, the industry will sustain a rational approach to pricing. And there are enough uncertainties and pressures on loss costs and profitability as well as higher reinsurance costs to bear, that we expect disciplined pricing through 2022 and potentially into 2023,” he said.

Albert Benchimol, AXIS Capital

Benchimol’s take on which lines were seeing the biggest rate hikes was generally in line with broker commentary offered late last year. The highest leaps came in cyber, which averaged 50 percent jumps for the year and 80 percent for the quarter, he said, noting that other professional lines saw average rate increases in the mid-teens. Liability, primary casualty and excess casualty are averaging increases in the high-single-digits for the quarter and the low-double-digits for the year, he said. And he said property rate increases were roughly 10 percent for the quarter and the year.

Turning to the reinsurance market, Benchimol agreed with the general consensus that prices are up about 10 percent on property-catastrophe reinsurance, but he stressed that pricing is not uniform. “Lower layers of reinsurance towers and aggregate treaties where supply was more constrained exhibited the strongest pricing increases, especially if they were loss impacted,” he said, putting increases for loss-impacted treaties in the 25-50 percent range.

“Our general view of the reinsurance market is that while it’s still running overall behind primary pricing, the market is heading in the right direction but must continue to do so to adequately compensate reinsurers for the risk and volatility they assume.”

Asked about the company’s appetite for cyber insurance business, Benchimol said AXIS Capital has reduced its exposure by about 40 percent since last June. “We’ve made some meaningful changes to our underwriting guidelines,” he added, referring to requirements about cyber hygiene in addition to reducing limits.

The CEO said that price increases are having a beneficial impact on cyber results. “The truth is that the cyber book we’re writing today is actually making an underwriting profit…It’s not like this is runaway loss costs that are draining the profitability of our company. It’s making an underwriting profit. We just don’t think it’s making this sufficient underwriting profit for the volatility and the capital requirements,” he said.

RenRe: Absorbing $1.4B in Weather Cats

Unlike AXIS Capital, executives at RenaissanceRe said the company didn’t make major moves to cut down property-catastrophe business during 1/1/2022 renewals. But reinsurance underwriters didn’t floor the accelerator to put a lot more of that business on the books either.

2021 was a year of significant growth for the Bermuda reinsurer.

- Adding property and casualty business together, full-year net written premiums grew $1.8 billion, exceeding CEO’s prediction earlier last year that growth in 2021 would surpass $1 billion.

- Top-line growth was evident across the book, with net property reinsurance premiums rising 40.8 percent and casualty and specialty premiums jumping 49.2 percent in 2021 compared to 2020.

- RenRe’s gross property reinsurance premiums grew 32 percent overall, but property-catastrophe premiums only grew 18.5 percent. Premium volume for “other property” rose 54.9 percent.

But $1.4 billion in weather-related large losses added 58.6 points to the property reinsurance combined ratio in 2021.

Observed CFO Robert Qutub, “2021 was the second highest loss year for natural catastrophes in our industry’s history, which are estimated to exceed $100 billion. In a year like this, you can see the power of the platform we have built.”

“We reported a modest operating profit, where we were able to absorb net negative impact from current-year catastrophes of nearly $1 billion because of our larger and more diversified business.”

Said President and CEO Kevin O’Donnell: “It was a difficult year where three out of four quarters were impacted by weather-related catastrophic losses and interest rates remained near record lows.”

Noting that RenRe’s full-year operating return on equity was just 1.3 percent, the CEO characterized the result as disappointing. Still, he expressed confidence that RenRe has the right strategy to deliver superior returns over the long term. Like Qutub, he supported the view by noting that a diversified book of business helped the reinsurer to post an operating ROE of 14.4 percent in the final quarter of the year, in spite of $50 million of net negative impact from fourth-quarter large catastrophic events.

Not shown on the chart above, RenRe also continues to benefit from fee income coming from its third-party capital management business, RenaissanceRe Capital Partners. Total fee income was $30 million in the fourth quarter and $129 million for the year.

Stable net investment income of $319.5 million also boosted operating results, but this was partially offset by $218 million of realized and unrealized losses, resulting in total investment returns for 2021 of $101 million, down from $1.2 billion in 2020.

Turning his attention to 2022, O’Donnell said, “In contrast to the [2021] year’s catastrophe losses—and in part due to them, we had a strong January 1 [2022] renewal….”

“In our property business, rate increases were sufficient to maintain our current book, but not enough to warrant significant growth.”

Kevin O’Donnell, RenaissanceRe

“The market trend in 2021 was to move away from property cat risk due to fears of climate change, social and monetary inflation, as well as a lack of confidence in cat modeling. However, our expertise and experience gave us the confidence to know when we were being paid adequately to assume this risk which we are uniquely positioned to understand and price…”

The CEO noted that RenRe achieved several important goals for its property book at the 1/1 renewal—getting more rate, improving terms and conditions, adjusting for an increased view of risk, decreasing exposure to aggregate deals, and keeping probable maximum losses flat.

“In our property business, rate increases were sufficient to maintain our current book, but not enough to warrant significant growth,” he said.

Later, he said, “Looking forward to the midyear renewals, we anticipate the positive trends in this market to persist and should remain first call on any opportunities that arise.”

Overall, considering property and casualty together, RenRe reduced its growth rate at the 1/1 renewal, O’Donnell said, without providing an overall figure. He did note that the reinsurer is already a lot bigger than it was a few years ago, and Qutub quantified that, stating that RenRe’s net premiums written have jumped 75 percent since the beginning of 2020.

“A significant amount of growth in our property premiums over the last few years has been in other property due largely to the substantial rate increases in the U.S. property E&S market,” O’Donnell noted at one point.

In 2021, RenRe’s gross property reinsurance premiums grew 32 percent overall, but property-catastrophe premiums only grew 18.5 percent. Premium volume for “other property” rose 54.9 percent.

Providing another highlight of RenRe’s 1/1 renewals, the CEO noted growth in the specialty portfolio, focused on cyber. “Cyber is particularly dislocated with very strong demand and limited supply, resulting in triple-digit rate increases and tightening terms and conditions,” he said.

AXA XL to Acquire S-RM

AXA XL to Acquire S-RM  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Business Uncertainty Drives Changes in C-Suite Strategy: Sentry

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry