“All the insurance players will be InsurTech” is a phrase we have uttered on many occasions in the past few years, but some InsurTechs have chosen to be insurers. Real insurers. Which means they file detailed financial statements.

Executive Summary

With permission of the authors, Carrier Management is republishing this analysis of the statutory financials of InsurTech insurers Lemonade, Metromile and Root, originally published on LinkedIn. Originally published as a single article, we present it as a three-part series.In Part 1, the authors present overall loss ratio, expense ratio and combined ratio results from statutory filings of the three insurers.

For the complete original article, visit the LinkedIn pages of Matteo Carbone or Adrian Jones.

These obscure but public regulatory filings are a rare glimpse into the closely guarded workings of startups.

Full-year 2017 filings for U.S.-based insurers were released earlier this month. Here’s what we found:

- Underwriting results have been poor.

- It costs $15 million a year to run a startup InsurTech carrier.

- Customer acquisition costs and back-office expenses (so far) matter more than efficiencies from digitization and no legacy systems.

- Reinsurers are supporting InsurTech by losing money too.

- In recent history, the startup insurers that have won were active in markets not targeted by incumbents.

We explain and show data for each of these points in this article.

Context and Sources

The most notable recent independent U.S. property/casualty InsurTech startups that operated throughout 2017 as fully licensed insurers are Lemonade, Metromile and Root.

Despite the lack of interest, being a fully licensed insurer may prove to be a more durable business model than the alternatives like being an agency or otherwise depending on incumbents, and the three carrier startups that we analyze all have strong teams with powerful investors.

The statutory filings we reviewed provide many of the traditional KPIs of insurance companies. Startups may use additional internal measures as they scale their company. Statutory statements typically do not include the financials of an insurer’s holding company or affiliated agencies, and companies have some flexibility in how they record certain numbers. But for all their limitations, statutory figures have the benefit of being time-tested, mostly standard across insurers, and measuring critical indicators like loss ratio and net income.

The Statistics

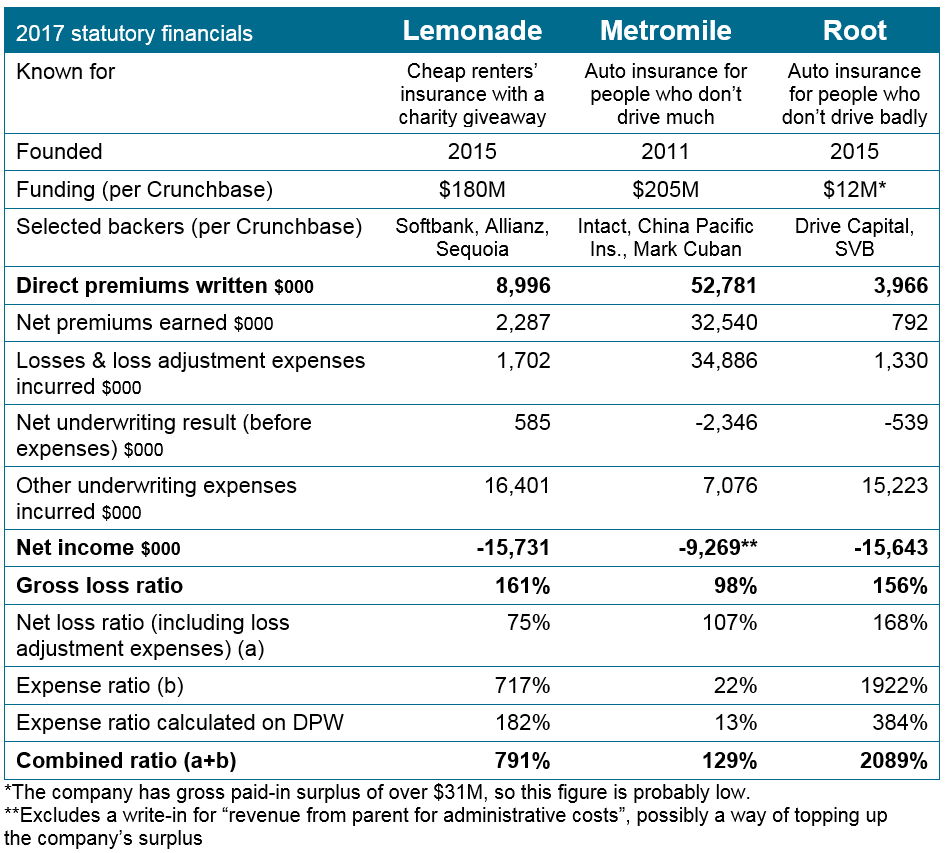

Here are the key stats on three companies—from top line to bottom line:

The ratios are typically calculated on net earned premiums, but we also show a row where the expense ratio denominator is total direct premiums written, which may be more appropriate for growing books.

Lemonade Insurance Company

- Considering the statutory top line before reinsurance of $8,996,000 of gross premium written, it’s unclear how Lemonade calculated that “our total sales for 2017 topped $10 million.” The premiums reported by Lemonade Insurance Co. may already have deducted the 20 percent fee paid to the affiliated agency—the parent company’s only source of income due to the giveaway model. (This would also explain why there is no commission and brokerage expense showing.)

- Lemonade claims to have insured “over 100,000 homes.” If we assume that this figure includes rented apartments, then it implies premium written per policy of $90, or $7.50/month if premium written is based on an annual policy.

- Lemonade’s giveaway does not appear to be separately disclosed. Nonetheless, one of the brilliant aspects of the business model is the fact that even with a 791 combined ratio, Lemonade still has at least one or two pools doing well and thus enabling the PR of a giveback.

Metromile Insurance Company

- As the oldest startup in this group, Metromile has by far the highest premium, but the loss ratio is still nearly 100. The expense ratio appears to have scaled down to a reasonable number, but the company puts $7 million of expense into “loss adjustment expense,” which may flatten the expense ratio.

Root Insurance Company

- As with Lemonade, the loss ratio around 160 is cause for concern. Is this a few volatile claims (bad luck) or a problem with pricing? Time will tell. (See related article, “InsurTech Carrier CEO Explains Poor 2017 Results; Fields Questions on Reddit.”)

Additionally, a few other notable companies are worth a mention:

Berkshire Hathaway Direct Insurance Company sells online via biBERK.com but isn’t a venture-backed startup. They wrote $6.4 million in premium last year—their second year of operations—most of it workers compensation. Their loss ratio gross of reinsurance was 124.

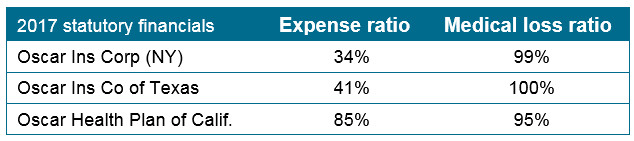

Oscar is a startup brought to you by Josh Kushner and others who have plowed in $728 million already, with more funds being raised currently. Oscar shows no signs of profitability in its three main states:

Bottom Line: Underwriting Results Have Been Poor

All three companies have a gross loss ratio of near 100 or higher. (For reference, the industry average in 2016 was 72.) That means they have paid $1 as claims for each $1 earned from policyholders in the last 12 months.

An insurance startup has to prove two critical things.

- Does the underwriting model work?

- Does the distribution model work?

We’ve been in debates over which is more important, and we always start with underwriting, since it takes no special talent to distribute a product that has been poorly underwritten (i.e., selling below cost). Underwriting quality/discipline is one of the “golden rules” of the insurance sector. Disrupt it at your investors’ peril.

Poor results are to be expected at first, even for the first several years. A single big loss can foul a year’s results in a small book. It can be hard to tell if that single loss is an anomaly or a failure in the model. Building an underwriting model is like playing whack-a-mole with a year’s time lag. Sometimes it’s difficult or impossible to address even widely known underwriting issues.

Other articles in this series:

- In Part 2, the authors break down the startups’ expense spends and discuss the impacts of InsurTech underwriting on the books of their reinsurers.

- In the final part, they offer conclusions about winning strategies of startup insurers.

For the complete original article, visit the LinkedIn pages of Matteo Carbone or Adrian Jones.

The authors’ opinions are solely their own, and only public data was used to create this article.

Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  A Matter of Trust

A Matter of Trust