Statutory financial statements are painting an unattractive picture for three InsurTechs that have chosen to become real insurers so far.

Executive Summary

With permission of the authors, Carrier Management is republishing this analysis of the statutory financials of InsurTech insurers Lemonade, Metromile and Root, originally published onthe LinkedIn pages of Matteo Carbone or Adrian Jones.In this part, they break down the startups’ expense spends and discuss the impacts of InsurTech insurer underwriting results on their reinsurers.

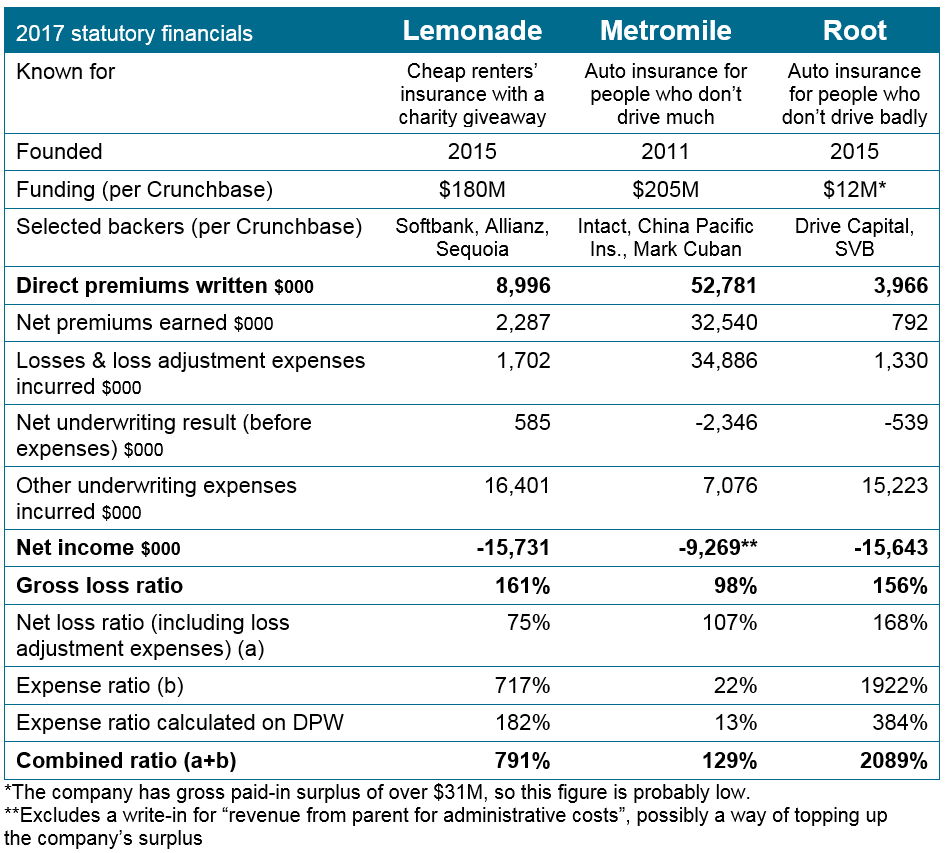

In Part 1 of this three-part article, we revealed that loss ratios for Metromile and Root were over 100 in 2017. While Lemonade reported a 75 loss ratio, a 791 combined ratio seems to jump off the page when expense ratios are added.

Here, we investigate what the expense ratios of all three mean in dollar terms, and what the overall underwriting results mean for the reinsurers supporting these carriers.

It costs $15 million a year to run a startup InsurTech carrier

All three companies incurred right about $15 million in run-rate expenses last year, of which $5-6 million is headcount expense. It may be possible to keep the overall expense total closer to $10 million if one is especially lean, but the cost of operating in a regulated environment and building a book quickly mount.

Some startups have organized as managing general agencies instead of a carrier. Thus they pay a “front” a fee of around 5 percent to produce their policies. However, even MGAs are state-licensed entities that are subject to most of the same regulation as carriers. So, the expense saving of being an MGA is only a true savings at small volumes.

The upshot: The capital raises of around $20-30 million that we have recently heard about may only be good for about two years of operating expense, before any net underwriting losses.

Scale matters in insurance and venture capital, but it’s a double-edged sword in insurance. Scaling too quickly without underwriting excellence magnifies underwriting losses; staying too small leaves the book volatile and the expense ratio high. Some startups have been active for several years and have not yet scaled, or even saw a reduction of premiums in the last year. But this may be better than scaling without sustainable underwriting results. Future financial statements will tell if any of the new players will gain a sustainable market share in a major business line in the U.S., or at least in a niche.

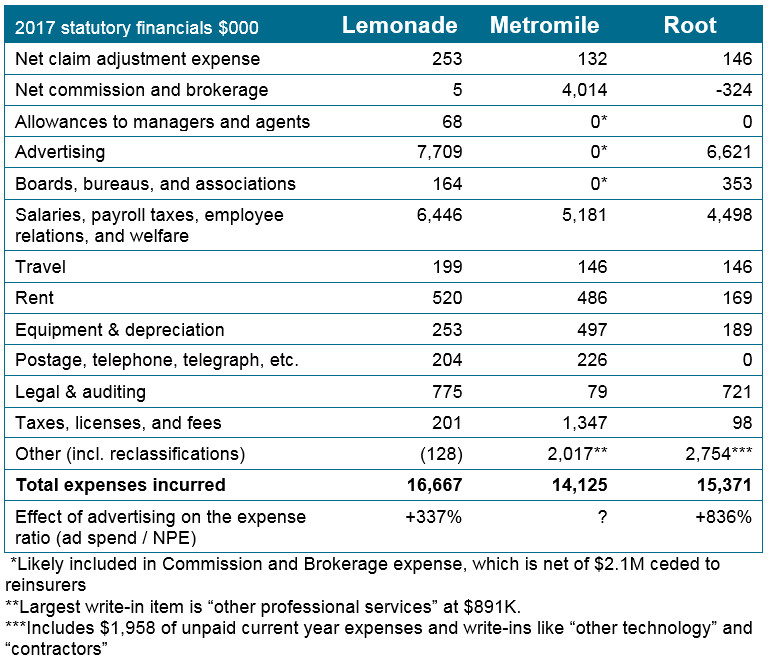

Customer acquisition costs and back-office expenses (so far) matter more than efficiencies from digitization and no legacy systems

Insurance investors need to understand back office expenses and distribution expenses, both of which are typically fixed costs for startups distributing directly to consumers. Here’s a look at what the three P/C insurance startups are spending money on. Beware that holding company expenses and affiliated agencies may or may not be reflected in the figures below, depending on the intercompany arrangements in place.

Lemonade

- This startup is spending almost $1 in advertising for every $1 of premium they wrote ($7,709,000 of advertising for $8,996,000 of premium written). If we assume (as we did in Part 1) that Lemonade has insured 100,000 homes and apartments, then the customer acquisition cost (CAC) assuming only advertising expense is around $77. This is probably a measure that encourages the company’s backers, since the CAC of a renewal policy written directly is minimal and the industry-average churn rate is single digits in U.S.

- The regulatory and overhead costs are considerable. Notice lines like Legal & Auditing, Taxes Licenses & Fees, and some of the salary expense.

- The volumes have to continue to grow exponentially for some years to get the cost base (also net advertising) lower than the 20 percent of the premium required to make a profit for the parent company. (For reference, the market average expense ratio in 2018 was 28). Recall that Lemonade Insurance Company’s parent or affiliates take a 20 percent flat fee up front for their profits and expenses and give to charity anything left after paying claims and reinsurance.

Metromile:

- Has the highest tax expense, perhaps because it is selling the most, with many states charging premium tax as a percentage of the policy value.

- Their “Legal & Auditing” expense is probably much higher but is put into “other.”

- Note the absence of advertising expense but large commission and brokerage expense, partially ceded to reinsurers. Accounting treatments, as ever, can vary by company.

Root:

- The company’s small volume makes it difficult to run the same absolute expenses as Lemonade and Metromile, but it might not be wise to grow a book running a loss ratio over 150.

- Has no telegraph expense (woo-hoo!).

- Unclear why the company has almost $2 million of unpaid expense.

Advertising expense vs. pricing

Old-fashioned insurance agents are a variable cost that scales up with the business. The agent absorbs fixed advertising, occupancy, and salary costs in exchange for a variable commission. But in the direct distribution models favored by many startups, variable costs and agents’ costs become fixed costs borne by the startup. (True, some can be kept variable, as we discuss below.) Fixed costs need to be amortized over more premium volume, which requires yet more fixed costs (e.g. advertising) to solve.

InsurTech carriers from the dot.com era like Esurance and Trupanion are still investing heavily in advertising and producing losses or barely breaking even. They would probably argue that they could eliminate much of their expense and “harvest” an attractive book of business for years to come—which may be true. The U.S. churn-rate in personal auto and home insurance can be as low as single-digits, far lower than many western countries. Since customer retention cost is much lower than customer acquisition cost, loyalty is absolutely critical to non-life insurers, particularly in a direct distribution model. (Bain & Co. has done excellent work on loyalty in insurance. Both of us are Bain alumni.)

Founders and investors today need to be prepared mentally and financially for a long road to profitability with tens of millions sunk before it becomes apparent whether the underwriting works and whether the relationship between CAC/distribution, fixed expenses, and customer loyalty can produce a sustainable and profitable business.

The API approach—a B2B2C model based on distributing the product through the digital fronts of third parties—has become “the new black” to transform fixed acquisition costs in success fees linked to the volumes. This model shows promise, provided that distribution partners do not extract too much value from the competitive insurance market.

The point for founders and investors today is to be prepared mentally and financially for a long road to profitability with tens of millions sunk before it becomes apparent whether the underwriting works and whether the relationship between CAC/distribution, fixed expenses, and customer loyalty can produce a sustainable and profitable business.

Reinsurers are supporting InsurTech by losing money too

Some members of the traditional industry have strongly supported the development of InsurTech through investment in equity, providing regulatory capital, providing risk capacity, and sharing technical expertise. Startup insurers typically are reliant on reinsurance as a form of capital because (1) it can be cheaper than venture capital, (2) startups typically need reinsurance to hold their rating, and (3) the strong backing of a highly rated reinsurer shows validation of the company’s business model, just like the backing of the best VCs provides.

The carrier model has real advantages concerning reinsurance: Reinsurance is easier to arrange and more flexible than an MGA relationship. Many successful agencies find that their economics would be better if they were able to retain some of the risk they produce instead of writing on behalf of a licensed carrier and ceding that carrier all but a commission.

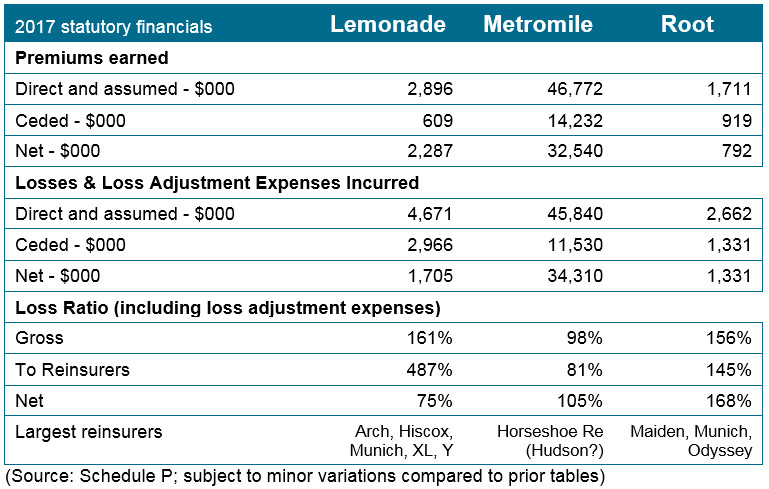

Here is a look at results disaggregated for reinsurance:

Observations:

Observations:

- Lemonade seems to have a great reinsurance scheme, but they have to hope that reinsurers continue to take $5 in losses for every $1 in premium ceded to them. The amounts ceded are small, and Lemonade has a big panel of reinsurers.

- Metromile and Root do not appear to get much loss ratio benefit from their reinsurance.

It is a great experience for a giant reinsurer to work with a small and innovative startup. The expected losses in dollar terms are negligible if compared with the value of the lessons learned, the culture created, and the halo the reinsurer may partially claim. Startups need to find reinsurers who are both flexible and prepared for losses, potentially for several years. But startups cannot count on reinsurers to take losses forever.

In Part 3 of this three-part series of articles, the authors offer conclusions about winning strategies of startup insurers.

A version of this article, originally titled, “Five Dispatches from InsurTech Survival Island,” was previously published on Mar. 12, 2018 by Matteo Carbone and Adrian Jones on their LinkedIn pages.

The authors’ opinions are solely their own, and only public data was used to create this article.

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment  Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It  Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  Zurich CEO: El Niño May Mean Fewer Hurricanes, Insurance Losses in North America

Zurich CEO: El Niño May Mean Fewer Hurricanes, Insurance Losses in North America