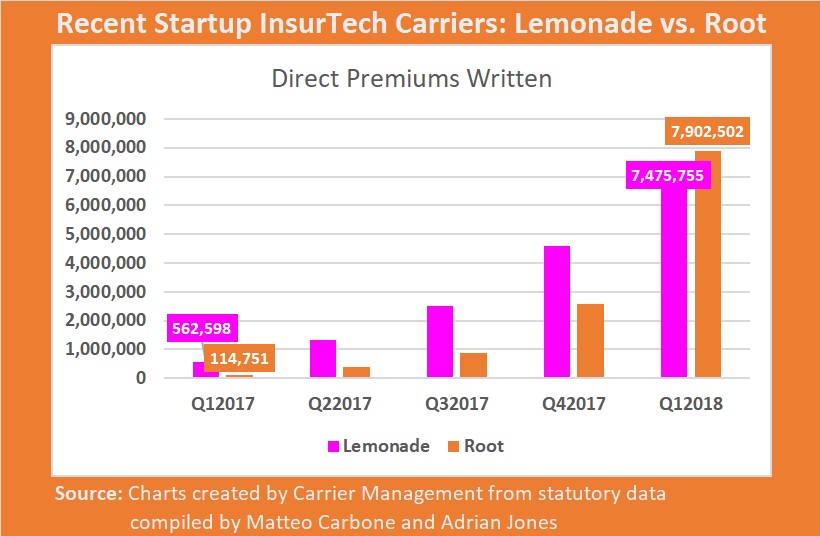

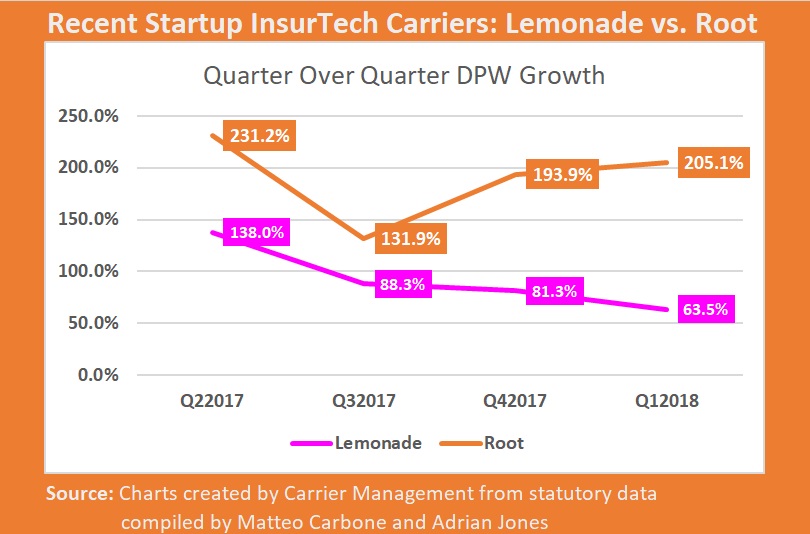

Considering differences in “share of voice” commanded by InsurTechs Lemonade and Root, a surprise of first-quarter 2018 is the fact that the Columbus, Ohio-based Root has squeezed past Lemonade in terms of premium volume.

But like auto insurer Metromile, which continues to tower over the other two in terms of premiums written, Root, an auto insurer focused on the best drivers, and Lemonade, focused on renters insurance, all reported loss ratios above 100 in the first quarter of this year, just as they had for all of last year.

Is it too early to judge these startups based on loss ratios? Do loss ratios scale?

We present the statutory results for Root and Metromile, and address the questions here. In Part 1 of this article, we provided financial details for Lemonade (and speculated about the trajectory of a key component of Lemonade’s business model—a promised Giveback to insured cohorts with good loss ratios. See related articles, “Bigger and Redder: A Look at Q1 2018 for InsurTech Lemonade and Other Carriers” and “Hands Still Tied at Lemonade“)

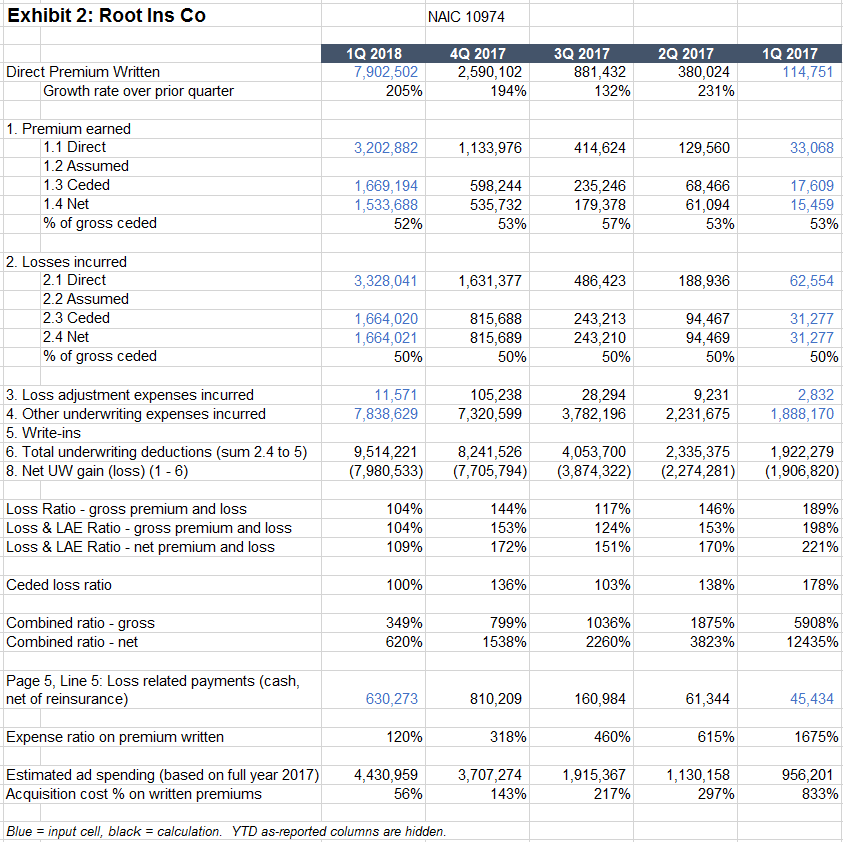

Root Ins. Co.

Root has grown explosively, with gross premiums written having trebled since fourth-quarter 2017. $2.9 million of $7.9 million of gross premiums written were in Texas, with Ohio and Arizona also chipping in more than $1 million each.

Potentially most impressive is the fact that Root apparently has achieved their growth without a massive advertising spend. If ad spending as a percent of total expenses remained constant this quarter compared to last year (a big “if”, since overall expense are rising rapidly), then Root has greatly cut its ad spending as a percent of the premium. See the bottom line of Exhibit 2.

As with Metromile and Lemonade, Root’s loss ratio remains unsustainably high, but the company’s $51 million fundraising round in June gives it a few years of runway to make improvements.

Following our previous article, the CEO of Root commented that his company’s loss ratio was high in part due to prudent reserving. Indeed, Root was the only of the three startup insurers to report favorable development in the quarter, to the tune of $239,000 of gross positive development, which would cut almost 10 points off the 2017 gross loss ratio. (In reality, it cut about 7 points from the 1Q18 loss ratio, since prior year results aren’t restated when reserves develop.)

There could continue favorable development, but so far the 2017 loss ratio would be cut from 138 to 128— still well above a sustainable level. Further, the company in 2017 paid $1.36 of losses for every $1 of premium earned (on a net basis).

Root’s reinsurance comes up for renewal at the end of June 2018 and currently consists of a 50 percent quota share and $1 million XS $100,000 tower, which limits volatility in results.

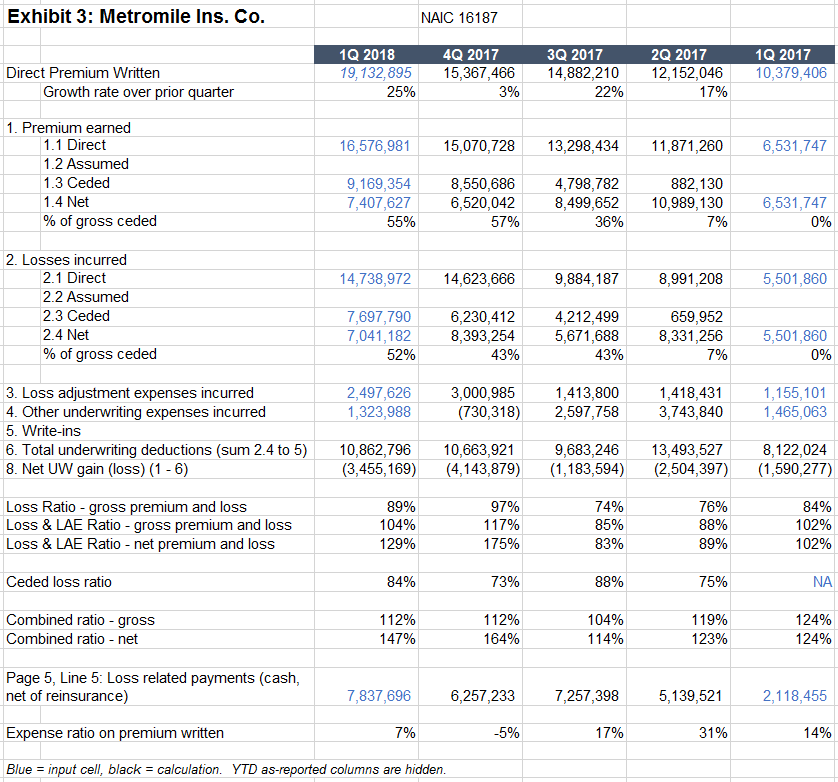

Metromile Ins. Co.

Metromile, the oldest and the biggest of the three, continues to grow premium—achieving an impressive 25 percent growth rate quarter over quarter. California continues to be the largest state, accounting for $11 million of $19 million of direct premium written this quarter, as compared to $5 million part of $10 million in the first quarter of 2017, which suggests that the company relies on one state but has room to expand. The company appears to be losing money in each state.

As with other InsurTechs, distribution has been easier than profitability. The gross loss ratio including loss adjustment expense at 104 remains close to the results posted in 2017 but above a sustainable long-term rate. For comparison, Progressive’s personal lines loss and LAE ratio was 74 in 2017 (30 points lower), with a combined ratio of 93. The gross loss ratio is affected by $1.5 million of adverse development, which added about 8 points to the loss ratio this quarter.

Does loss ratio scale?

We have been surprised to hear some investors comment that they expect loss ratios to decline with scale and to consider them as any other costs on the insurance income statement. There are some elements of loss ratio that scale, but only in a limited way, i.e. a few points, not cutting the loss ratio in half.

- Claims: Taking claims in-house at the right time can reduce the loss and LAE ratio. TPAs get paid to manage and settle claims, which isn’t always exactly what carriers or MGAs want. (Claims is a moment of truth that drives loyalty, and on the other hand, insurance fraud is real.) Bigger insurers also have better ability to drive favorable pricing with repair shops, contractors, and outside adjusters.

- Portfolio management: Scale can enable the company to be more selective about risks underwritten, thus avoiding the worst risks. It’s hard to manage a portfolio (i.e. cut the worst risks) when also growing it rapidly from a small base.

- Underwriting: Scale can help the company understand its own loss experience and adjust its underwriting accordingly. When companies start, they assess what risks are good or bad using industry data and placing bets that certain segments are more attractive, thus targeting those segments or distributors that target them. As the company gathers data on the performance of its own book, through time and scale, they can adjust underwriting and pricing to attract customer segments that perform particularly well for their particular business model. Again this has a tradeoff against growth.

- Mathematics: The law of large numbers will cause actual loss ratios to converge closer to the expected loss ratio. This isn’t really the loss ratio scaling down, but rather limiting the probability of a single really bad loss poisoning a year’s results.

However, when an insurer says that “we are indifferent to the level of claims” and then turns in a loss ratio that is double a sustainable level, investors should ask themselves, “what if they really are indifferent?”

More of the Same

We have been grateful for the positive feedback on our first article covering 2017 results, with both startups and incumbents featuring highly on the list of companies whose employees read the article. So far, 2018 results do not lead us to change our conclusions from 2017.

The three companies we’ve analyzed have several years of cash on hand, during which time they will probably continue to grow rapidly. They will probably improve their loss ratios, and expense ratios will scale down. The question is whether the figures get to a sustainable level.

We won’t know for a few years whether these daring startups are really groundbreakers or just expensive follies—as long as they are not acquired in the meantime. We’re cheering for them and think that we will see rapid growth and also profitability improvements in future quarters.

We were asked a few times about other companies, particularly in non-U.S. markets. Many countries have similar filings to the U.S. statutory filings, but we’ve not published anything on them yet. Also, agencies and brokers typically do not file public financials. We have begun to observe a trend, such as with Next Insurance, of InsurTech agencies converting to carriers or at least exploring the idea seriously. There are many reasons why this makes sense at a certain point in a company’s development, and it will provide more InsurTech carriers’ financials to analyze in years to come.

The authors’ opinions are solely their own, and only public data was used to create this article.

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It  A Matter of Trust

A Matter of Trust  Driver Death Rates High for Small Cars, Big Engines: IIHS

Driver Death Rates High for Small Cars, Big Engines: IIHS  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums