Carriers can toss out old playbooks that helped them map financial metrics into A.M. Best ratings, according to rating agency analysts, who are putting finishing touches on a new capital adequacy model that they’ll use in rating reviews next year.

Gone are the days when a Best’s Capital Adequacy Ratio of 150 could have meant a possible “A” rating, 175 meant an “A+,” and anything below 40 was a D.

Gone are the days when a Best’s Capital Adequacy Ratio of 150 could have meant a possible “A” rating, 175 meant an “A+,” and anything below 40 was a D.

During a webinar in October last year, and in two more recent interviews with Carrier Management, A.M. Best analysts gave insight into methodology changes where BCAR numbers won’t be mapped to letter grades, and where the BCAR scores of financially strong firms might look like 27 instead of 150.

They also described a two-part update that will do more than simply use stochastic simulation to develop various risk factors for BCAR—the initial goal of the BCAR revamp. A.M. Best also plans to revise the entire Best Credit Rating Methodology (BCRM)—the procedure that describes how BCAR scores and other indicators of balance sheet strength fit together with assessments of operating performance, business profile (by line, geography, distribution channel, etc.) and enterprise risk management to help analysts determine insurers financial strength ratings. Draft documents are scheduled to be published in March.

The real role: “Even when we look within the balance sheet strength piece of the puzzle, BCAR alone does not equal the assessment of the balance sheet. There’s a number of other factors we consider ranging from other types of financial metrics; financial flexibility; view of investments; the quality of capital; liquidity; asset-liability management; and internal capital models, just to name a few,” he said.

Insurers still don’t appreciate the real role of BCAR, and don’t grasp the idea that a Best credit rating encompasses more than capitalization. That lack of understanding means that the BCAR model update is generating “a good deal of anxiety in the industry,” Easop said, suggesting that the concerns are unfounded.

Don’t Freak Out

“My score dropped. Oh, no, I have an issue. I used to have a 300 BCAR; now I have a 50 BCAR.”

That’s how insurers may have reacted if A.M. Best didn’t decide to hold up the release of the BCAR draft criteria to coincide with a BCRM update, Matthew Mosher, executive vice president and chief operating officer, told Carrier Management during an interview in last month. Mosher confirmed what Easop and Thomas Mount, a vice president in Best’s Criteria Research and Analytics group, said during the October webinar—that overall P/C BCAR scores are inherently going to be lower under the proposed calculation. (See next section, “Why the New BCARs Are Lower.)

That doesn’t mean overall ratings will drop, however, the analysts said. “As a starting point, the industry is very well capitalized. So capital is not really a ratings driver,” Mosher told Carrier Management. “When you look at our overall methodology, our view is that our ratings are appropriate right now,” he said.

Going a step further, Easop said, “We don’t believe the updates to the BCAR or… the application of BCAR within the rating will result in sweeping change in any ratings. The goal [of the update] is fundamentally to deploy more advanced techniques so we can better understand and evaluate the risks facing insurers. This is no different than the process that most insurers are going through right now to develop advanced tools in the underwriting, risk management, or other disciplines,” he said.

The stochastic modeling process results in a better view of the risks insurers face. “Our view of the [BCAR] model is that it’s much more robust. Your BCAR score might go down, but it doesn’t impact what that BCAR score means to the overall rating because our view of what’s necessary for a rating has changed as well,” Mosher said.

Why the New BCARs Are Lower

As analysts fine-tune the risk charges with better technology and better data, a few of those charges are changing dramatically. One example: the charge related to investments in unaffiliated common stocks. Previously this was a factor of 15 percent applied to the holdings; now an economic scenario generator captures scenarios of future stock volatility, churning out factors in the 35-40 percent range.

As analysts fine-tune the risk charges with better technology and better data, a few of those charges are changing dramatically. One example: the charge related to investments in unaffiliated common stocks. Previously this was a factor of 15 percent applied to the holdings; now an economic scenario generator captures scenarios of future stock volatility, churning out factors in the 35-40 percent range.

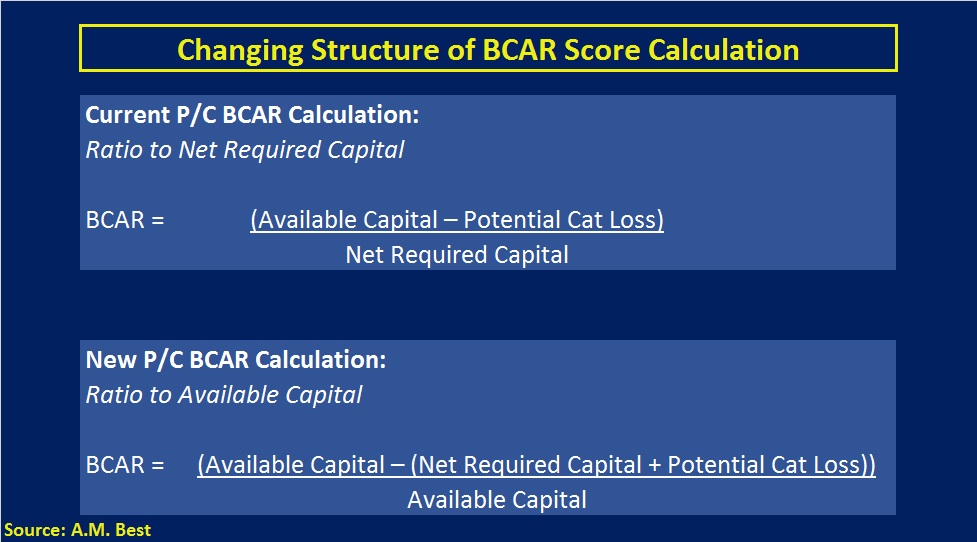

Still, that’s not a big driver of overall BCAR score changes, especially for insurers that aren’t heavily invested in stocks. Yet BCAR score values will be lower across the board—for all P/C companies. In fact, no company will have a score over 100 anymore. That’s because A.M. Best has turned the calculation for the ratio on its head—literally flipping the numerator and denominator—so that a straight comparison of old BCAR scores and new ones is impossible.

The BCAR ratio was—and remains—essentially a comparison of required capital to available capital (policyholders surplus with some adjustments), where net required capital is a combination of risk charges for underwriting and investment activities (each now being determined through computer simulation). The old calculation is a ratio of available capital (reduced by potential catastrophe loss) divided by net required capital. For the new one, analysts reduce available capital by net required capital (and the potential catastrophe loss), dividing that difference by available capital.

Why the change?

“The benefit of this is [that] a lot of the current risk appetite and risk tolerance statements talk in terms of company’s willing to lose a certain amount of their surplus,” Mount explained during the October webinar. “This now allows us to tie BCAR more directly into those risk appetite and tolerance statements. So if a company were to say, we’re willing to lose 10 percent of surplus, we can see how much excess capital a company has above its net required capital and make that comparison directly,” he said.

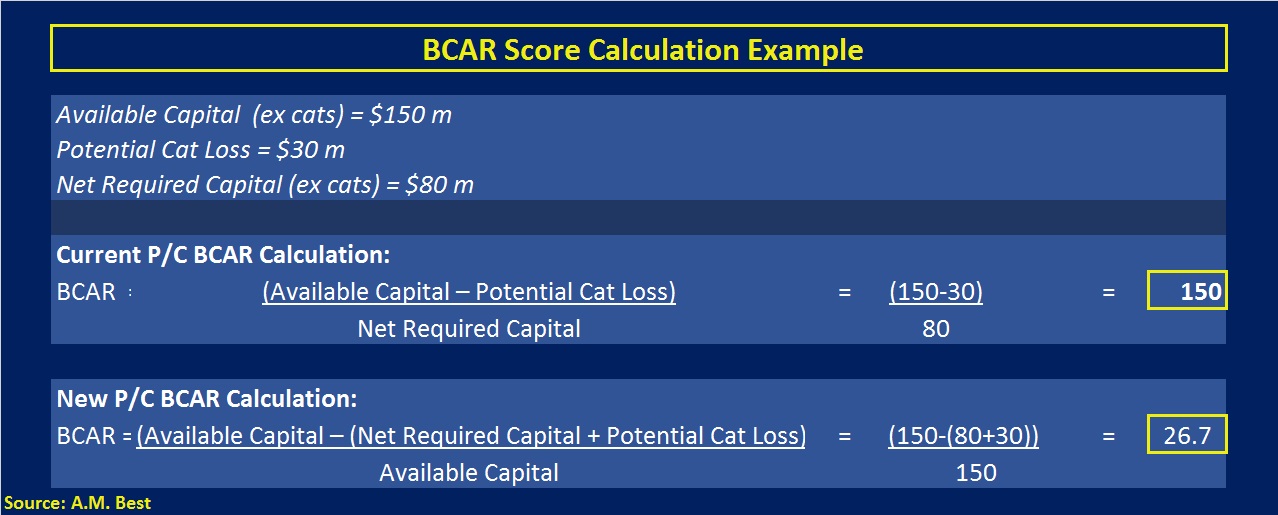

“You’re not going to be able to compare the planned BCARs—which are a ratio to the surplus—to the old BCAR scores, or ratios to net required capital. They’re completely different,” Mount said, after reviewing an example for a P/C company that has a 150 BCAR under the current method, which will have a BCAR of 26.7 under the new BCAR.

Ranges of scores extended from 0 to 999.9 in the past, and you wanted a BCAR greater than 100, signifying that the carrier had more available capital than it needed. With the new one, the range extends from -999.9 to a maximum of 100.0. Now, you want at a BCAR score greater than 0, he said.

(Editor’s Note: Even if A.M. Best had not changed the structure of the BCAR ratio from one in which net required capital is the denominator to one where available capital is the denominator, another change in the calculation—adding the catastrophe loss to net required capital rather than subtracting it from available capital—has an impact on its own. In the example Mount reviewed during the webinar, just that change moved the BCAR from 150 to 136.6.)

Five VaRs

Easop noted that advanced simulation modeling techniques are giving analysts better tools to understand certain types of risks. “Tail risk and asset volatility are two obvious examples,” he said.

With particular attention to tail risk, A.M. Best analysts are using a value-at-risk metric (probability of ruin or VaR) from stochastic models—and calculating the BCAR scores at five individual points in the tail of the simulated probability curves for the various risks facing an insurance company.

With particular attention to tail risk, A.M. Best analysts are using a value-at-risk metric (probability of ruin or VaR) from stochastic models—and calculating the BCAR scores at five individual points in the tail of the simulated probability curves for the various risks facing an insurance company.

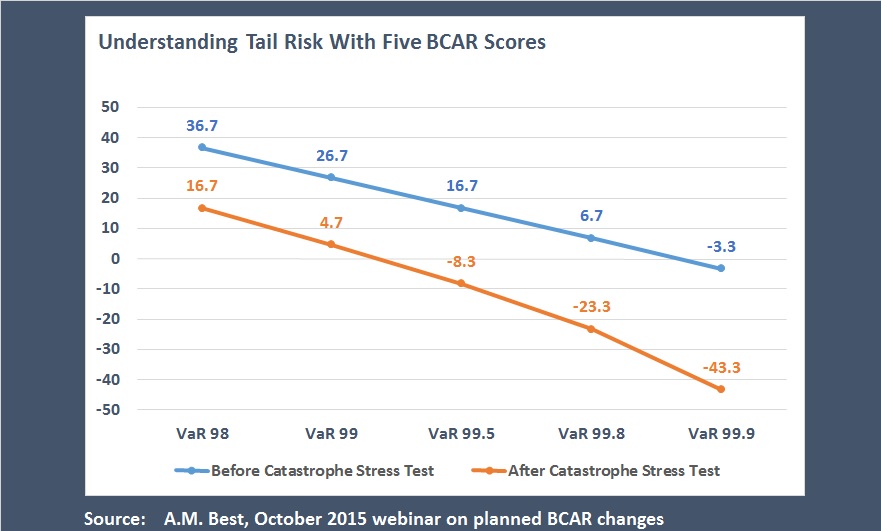

Mosher notes that while the current model is loosely tied to a 99 percent confidence interval, going forward, Best analysts will now also look at results for the 95 percent confidence interval, 99.5 percent, 99.8, and 99.9. “When you look at a 99.9 percent confidence interval, you’re at 1-in-1,000-year type of loss as opposed to 1-in-100 year” at the 99 percent level, allowing the analysts to evaluate exposure to tail events.

As the confidence levels go up, the BCAR scores go down, Mount said, noting that analysts will be able to see how quickly scores fall from positive values—which indicate a company has sufficient capital available to absorb all of its risks—to negative ones. Reviewing an example for a company with a 26.7 score at the 99 percent confidence level, he showed that increasing levels of required capital at each higher confidence level ultimately produced a BCAR of negative 3.33 at the 99.9 confidence level. “The interpretation is that the company did not have enough capital at the 99.9 percent level to absorb its net required capital including cats. That shortfall amounts to 3.3 percent of capital,” he said.

The hypothetical company in the example had available capital of $150 million, potential catastrophe losses of $30 million and $80 million of net required capital for other risks (other than cat losses) at the 99 percent confidence level. At the 99.9 percent level, available capital remained unchanged (at $150 million) while the cat loss rose to $60 million and the other net required capital to $95 million.

According to Easop, this particular company could achieve an A++ rating even though it does not have adequate capital at the highest confidence level of 99.9. “The reason is, when you take [into account] other balance sheet factors, [and] when you look at operating performance, business profile and enterprise risk management, that can enhance our view of a company’s strength,” he explained.

Reinsurance Dependence Examined

Mount also noted that A.M. Best will continue to perform catastrophe loss stress tests, as it has in the past, but now carrying out what-if scenario adjustments (reducing available capital for a 1-in-100-year probable maximum loss, adding 40 percent of ceded loss recoverables onto credit risk, adding 40 percent of the net PML to loss reserves) at all five confidence levels.

Continuing the hypothetical example, the stressed BCAR score fell below 0 at the 99.5 percent confidence level. And at the 99.9, the unstressed minus-3.3 score became a minus-43.3.

“The company may have other options not reflected in the BCAR model,” he said. “The BCAR model is pointing out, hey, you may have an issue here. But maybe you have contingent capital, maybe you have lines of credit for liquidity risk, maybe you have guarantees from a parent company or affiliate.

“This just points out there may be an issue,” prompting analysts to ask, “How does you company manage this issue,” he said, reinforcing Easop’s statement that risk management activities not captured in the numerical score will be considered as part of the Best Credit Rating Methodology.

Mount highlighted “dependence on reinsurance” as one particular issue to be addressed outside the BCAR model that could have negative consequences to a rating. Beyond simply simulating reinsurance recoverability (with inputs reflecting type, reinsurer rating and recoverable duration) in the net required capital calculation, he noted that reinsurance “can be viewed as short-term capital. You purchase it one year at a time and the market may dry up,” he said, analyzing the worsening BCAR scores of the hypothetical company exposed to the stress test. “You may be left with a high exposure to catastrophe risk [because] you can’t—at least on an affordable basis—get protection.

Mount made similar comments later in the webinar when asked whether the new BCAR model might drive small or geographically concentrated insurers to buy more reinsurance.

Interpreting the question to infer that the insurer’s PMLs “out in the tail may be high relative to surplus,” Mount again said that reinsurance is a short-term solution. “Really, that’s an underwriting issue or a risk appetite issue. They may not want to change their underlying underwriting portfolio” long term, he said.

By looking at five confidence intervals, Best analysts are getting a greater understanding of the risk profile of the company. “Before, …we were only looking out to the 1-in100 where you can buy reinsurance up to that point. You may not be able to buy up to these points in the tail which is something that the analyst can see now right there in the BCAR model,” he said.

Net Required Capital

Mount was also asked how BCAR scores account for the difference in risk between an insurer with three reinsurers on its panel and one with 30 reinsurers.

Reinsurance credit risk (for uncollectible recoverables), investment risks (bond defaults and stock price volatility), insurance pricing risk (potential for underwriting losses on business written) and reserve risk (potential for unanticipated adverse reserve development) will all now be estimated stochastically with some insurer specific input assumptions going into the computer simulations. For reinsurance credit risk, for example, Best is going to look at duration of recoverables, type (paid, unpaid, unearned premium) and reinsurer ratings.

“If you have a concentration in an individual reinsurer, and you simulate a default, you lose all of those recoverables. That’s a severity issue,” Mount said, noting that risk factors for reinsurance recoverability “will jump up” out in the tail (at high confidence levels). A default produces a big dollar amount for a carrier with a concentrated reinsurance panel, even if nothing shows up at low confidence levels.

For an insurer that has more reinsurers, and recoverables spread evenly across those reinsurers, the impact of any one of them defaulting is less out in the tail. “So the [reinsurance] risk factors would be lower for someone that’s more diversified,” he said.

Discussing the other stochastically modeled risk charges, Mount, Mosher and other analysts have indicated that despite the specificity of the inputs for the underwriting factors (with 84 simulations possible for 21 lines of business and four company size categories), there is little notable movement in the insurance pricing and reserve risk factors, especially at the 99 percent confidence interval (which aligns with the current model). More significant changes are apparent for the asset risk factors—for stock and bonds (with distinct default risks simulated for different bond maturities and durations).

Carriers will be able to see the results for themselves within a few weeks, when A.M. Best releases the P/C BCAR criteria for public comment along with company BCAR output and the BCRM update. The releases are expected in early March, Mosher told Carrier Management.

Video excerpts of Carrier Management’s interview with Matthew Mosher are available at these links:

- BCAR Revisited: Why A.M. Best Is Updating Its Capital Ratio

- Widespread Rating Changes Not Expected When A.M. Best Rolls Out New BCAR

Other related articles detailing the interview with Mosher and earlier A.M. Best webinars about the development of the new BCAR include:

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?  Design the Team Before You Design the Solution: Commercial Trucking Case Study

Design the Team Before You Design the Solution: Commercial Trucking Case Study  Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment