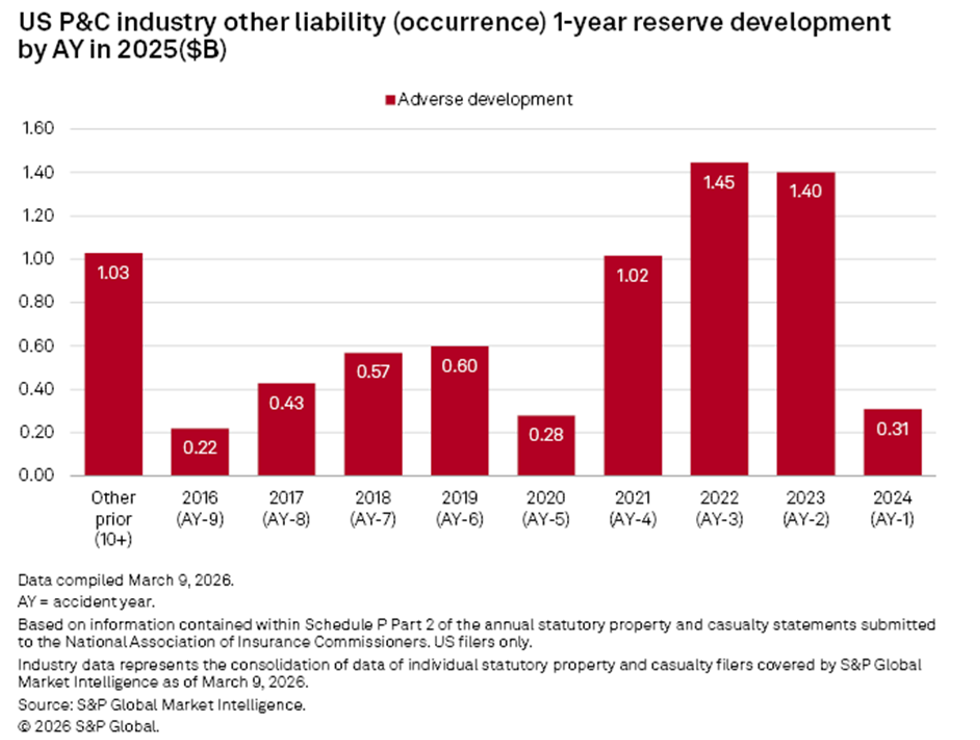

The U.S. insurance industry saw $7.3 billion of adverse loss development in the other liability (occurrence) line during 2025, with more than half of the total coming from recent accident years, according to a new report.

The report published by S&P Global Market Intelligence last week shows $3.9 billion of one-year adverse development for accident years 2021-2023 for the other liability (occurrence) line—and nearly $3 billion of reserve strengthening in accident years 2022 and 2023 alone.

When adverse development clusters in recent accident years, it signals that loss trends are outrunning pricing, according to S&P GMI’s report.

Adverse development is now centered on recent accident years rather than legacy runoff, the report notes, referring to the smaller $1.0 billion boost for accident years prior to 2016.

“When Schedule P one-year development turns adverse, it is not accounting noise but proof that last year’s booked ultimate was too low, and when that adverse development clusters in recent accident years, it signals that loss trends are outrunning pricing,” state the authors of the report, “Other liability (occurrence) trouble shifts to recent years in 2025.”

Does that mean that pricing is set to change?

“Our view is that pricing in a broad sense does need to go higher—and is going substantially higher in certain coverages like personal umbrella/excess— but it will struggle to catch up to loss costs in certain coverages given both the impact of competitive pressures on the magnitude of price increases and the role social inflation is playing in some jurisdictions,” Tim Zawacki, principal research analyst at S&P GMI, told Carrier Management in an emailed response.

Given the level of ongoing prior-period development (PPD), competitive pressures won’t fuel the level of softening that’s likely to impact other lines this year, such as private passenger auto, according to William Wilt, president of Assured Research. Wilt wrote that “the ingredients are in place for a ‘gradual recalibration’ in liability lines rather than outright softening” in a reserve analysis Assured Research published this week. Overall, Wilt’s analysis indicates a $20.7 billion redundancy in industry carried reserves across all lines but a $12.5 billion deficiency for the other liability (occurrence) by itself.

“It’s my perspective [based on prior research] that adverse PPD is one of the main drivers of other liability (occurrence) rates,” he told Carrier Management in an email explaining his view that outright softening is not on the cards for this line of business.

Wilt highlighted the impact of recent accident years on his projected deficiency for the line, with accident years 2021-2023 accounting for more than 70% of the $12.5 billion deficiency. (His figures reveal a $2.1 billion deficiency for AY 2021, $3.1 billion for AY 2022 and $3.5 billion for AY 2023).

In terms of loss ratios, Wilt projected ultimate loss ratios for accident years 2021-2023 that are roughly 5 points higher than the published industry ultimate loss ratios for these accident years. But that difference is cut nearly in half for accident year 2024 and there is almost no deficiency indicated for accident year 2025. (In other words, Wilt’s estimate ultimate loss ratio for accident year 2025 is just about the same as the industry published loss ratio).

Insurers have become more conservative in their loss ratio picks for the two latest accident years, he noted.

Putting all this together, “the ingredients are in place for other liability (occurrence) rates to remain elevated as adverse PPD comes through on AYs 21-23, but assuming less comes through on AYs 24-25, it seems less likely to me that rates move higher than loss trend,” he explained.

“If rate increases on other liability occurrence products stay elevated and come down more gradually than most or all other lines, I’d call that a recalibration rather than an outright softening,” he wrote.

Related article: P/C Industry Loss Reserves Redundant by More Than $20B: Assured Research

Focus on Recent Accident Years

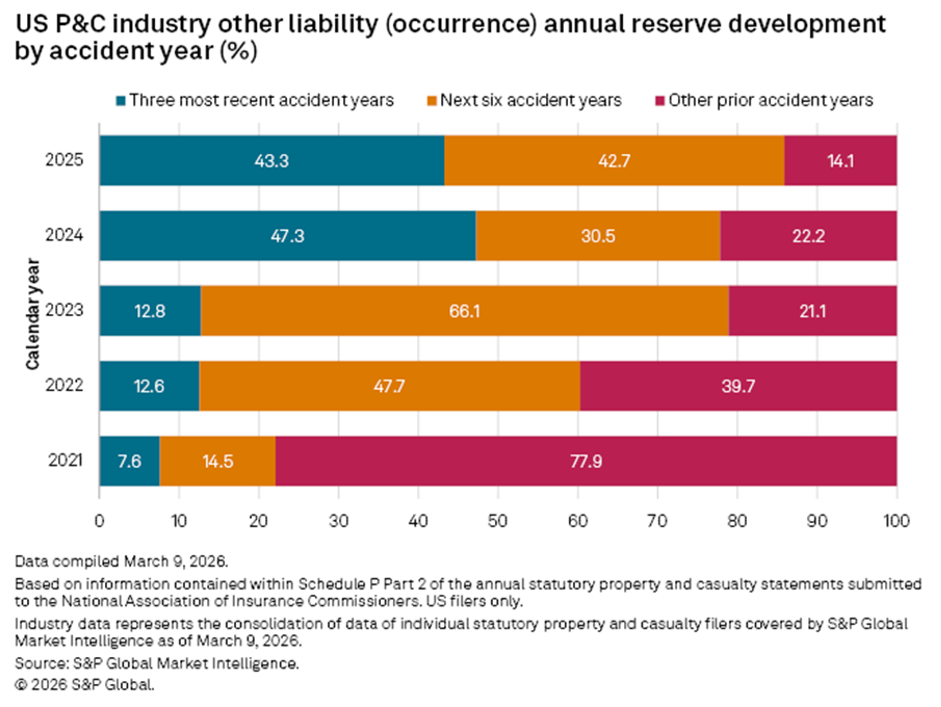

The S&P GMI report displays the distribution of reserve strengthening for the other liability (occurrence) line across various accident years for each of the last five calendar years, which is republished below.

“The industry is spending nearly as much reserve strengthening on near-current underwriting years as on the mid-tail, and far less on truly old years than it used to,” the authors observe, pointing to the fact that only 14.1% of the lines adverse development during 2025 related to the oldest accident years. In calendar year 2021, the comparable figure was 77.9%.

S&P GMI analysts refer to the challenge of adverse reserve development for the other liability line as a “systemic one,” highlighting a long list of commercial insurers—primary carriers and global reinsurers—reporting reserve strengthening for the line in 2025. A list of the 2025 reserve changes for 20 other liability writers presented in the report shows half with adverse development and half with takedowns. Liberty Mutual had the biggest amount of adverse development, $1.3 billion, followed by Chubb roughly half as much ($.0.7 billion). On the other end of the spectrum, Swiss Re had the largest amount of favorable development, at just over $700 million.

According to S&P GMI, the “systemic challenge is shaped by each company’s business mix, attachment points, and prior reserving stance, compounded by shifting litigation and social inflation dynamics.”

“Other liability (occurrence) serves as a long-tail stress test for the U.S. P/C industry, concentrating the legal system’s loss amplifiers. Even small assumption changes can lead to significant reserve movements, with tort reform legislation having mixed impacts across different states,” the analysts said.

Two Decades of Favorable Development

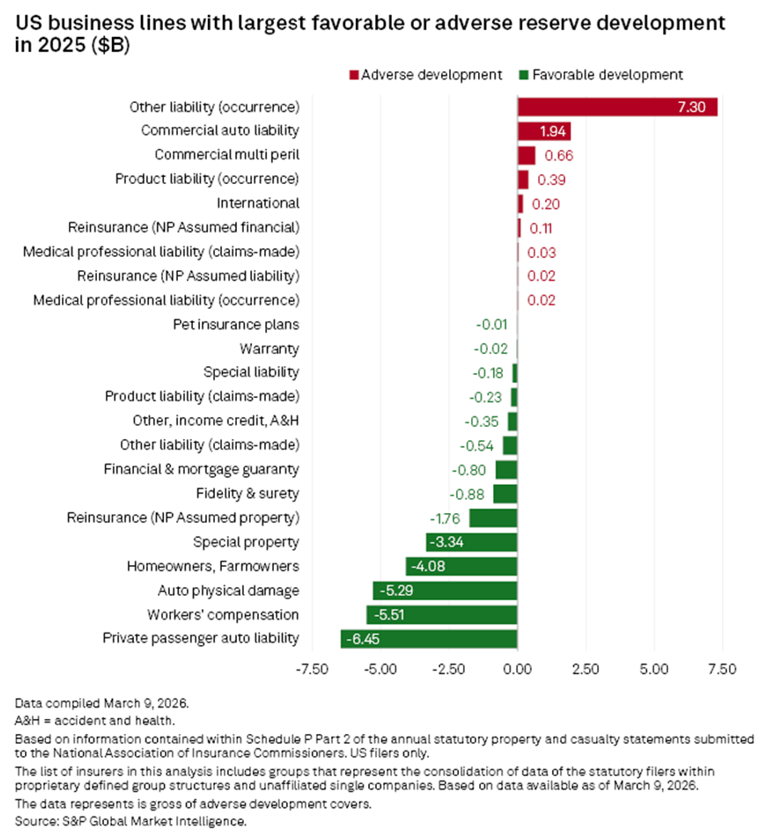

Across the industry, the $7.3 billion in adverse development for other liability (occurrence) is the largest adverse loss development figure reported for any business line during calendar year 2025.

But overall, loss reserves across all P/C lines combined developed favorably, with total favorable development of $18.7 billion. More than 90% of the total came from favorable development in the private passenger auto liability ($6.5 billion), workers compensation ($5.5 billion) and auto physical damage lines ($5.3 billion).

Based on Carrier Management records, 2025 marked the 20th straight year of favorable overall development.

Who Gets Credit for Successful Renewal During Soft Re Market?

Who Gets Credit for Successful Renewal During Soft Re Market?  Robotaxis Operating Without Manual Controls, Like Brake Pedals, Coming Soon

Robotaxis Operating Without Manual Controls, Like Brake Pedals, Coming Soon  Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  UN, Scientists Warn Strong El Niño Will Add Fuel to ‘Planet Already on Fire’

UN, Scientists Warn Strong El Niño Will Add Fuel to ‘Planet Already on Fire’