This year will mark the fourth year of a hardening market for commercial lines underwriting cycle, according to the latest U.S Commercial Lines Market Update released by Fitch Ratings..

The Council of Insurance Agents & Brokers’ (CIAB) commercial lines market survey indicates overall rates rose 8.8 percent in the first-quarter of 2023, compared with 6.6 percent in first-quarter 2022.

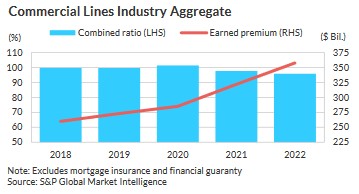

Underwriting performance for the commercial lines market improved nearly two points in 2022, with a 95.8 combined ratio marking the fifth consecutive year of a combined ratio under 100.

Boosted by socioeconomic uncertainty during the pandemic, rate momentum was pushed up even more by high inflation. Weak loss experience and higher reinsurance rates led to a rebound in pricing momentum this year in both property and auto segments.

Property rates rose by 20 percent in first-quarter 2023, according to CIAB, due to large increases in reinsurance costs, while commercial auto moved 8.3 perecent higher compared with 5.9 percent in first-quarter 2022, the Fitch report noted, adding that general liability and umbrella rates continue to move upward.

Following large increases the previous two years directors and officersliability and cyber risk, experienced a sudden flattening of rate changes.

According to Fitch’s analysis, workers compensation posted the best product segment underwriting profits, with an average combined ratio of 89 for the past five years. The line showed “strong premium growth in 2022 from exposure changes, falling claims frequency and highly favorable reserve experience bolstered recent performance,” the report stated.

Related article: Eight Straight Years of Workers Comp Profits: What Could Go Wrong

On the other side of the coin, the combined ratio for commercial auto line worsened to 105 in 2022, up five points from 2021.

Even with higher commercial auto premium rate increases, claims severity tied to higher parts and repair costs and litigation exposures continue to challenge the line in 2023.

With an average hurricane season forecast, catastrophe losses should run as expected, leading to a modest underwriting profit in 2023, according to the ratings agency, which projects a 97–98 combined ratio for the commercial lines sector this year.

While the 10 percent growth in 2022 commercial lines net written premium remained above historical norms, revenue expansion in 2023 will slow to 607 percent, the agency added.

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz