In striking contrast to last year’s double-digit rate hikes for public directors and officers liability insurance and 100-200 percent jumps for cyber coverage, some buyers renewing those coverages this spring won’t see their insurance bills increase at all.

And many will see double-digit declines, according to the latest Insurance Marketplace Realities Report published by global broker and advisory firm WTW in late April. On the low end of the range of rate changes projected by WTW experts in this year’s report, public D&O insurance buyers could see rates actually drop as much as 10 percent, and cyber insurance buyers might experience flat renewals.

“The strong financial market in the last few years has mitigated claims activity, and insurance carriers are aggressively pursuing market share, which is helping drive down pricing at rates unseen in more than a decade,” John Drummond, head of Broking, North America, wrote in the executive summary to the latest report.

Separately, Aon reported the sharpest declines in D&O insurance pricing in the more than a decade for the first quarter of 2023.

The broker view was supported by insurance carrier executives including RLI Corp. Chief Operating Officer Jen Klobnak, W.R. Berkley Corp. President Robert Berkley, Chubb Chief Executive Officer Evan Greenberg, and Markel Corp. Insurance Operations President Jeremy Noble, who called out the line as one they are cautious about during first-quarter earnings conference calls.

Klobnak reported a broker tally of the 20 newcomers to public D&O market in recent months. “We believe these new entrants are late to the party and are providing brokers with more mouths to feed,” she said, noting that premium for RLI’s Executive Products Group dropped 14 percent in the quarter.

Berkley described the large account D&O marketplace as being “in a state of free fall as far as rate adequacy or pricing.” Like Klobnak, Berkley noted the new entrants and added that there isn’t new demand to balance the new supply. “We have seen a dramatic reduction in IPOs,” Berkley said. “We’ve just seen a dramatic reduction in a lot of the activity that would drive D&O purchasing,” he said.

“The reality is that the demand has been reduced and the supply has increased, and that has led to an unattractive, competitive environment from our perspective.”

Said Chubb’s Greenberg: “There are a lot of players with no data and no experience, and they’re receiving, many of them, capacity by those who don’t seem to have their eye on the ball…We’ll always trade in that case, volume for the right underwriting. And it’s not an area that I think is devoid of risk, particularly as you look forward—everything from recession and volatility in financial markets to climate change and claims of greenwashing and all of that,” he said.

At Markel, Noble said his company is not comfortable with the pricing trend for the large account D&O space. “As a result, we are shrinking, selectively allowing some business to lapse and being very discerning around new accounts.”

Noble cited excess casualty lines as another area where Markel is pushing hard for rate and willing to let existing business lapse where they are unable to get it.

Chubb’s Greenberg, who referred to a general reacceleration of commercial insurance pricing for North American P/C business, noted markets hiking prices in response to loss trends in property and excess casualty lines. Unpacking his overview of improved pricing line-by-line, he ended up declaring the trajectory of commercial insurance prices as “a mixed bag.”

That’s precisely the description that WTW’s Drummond used in his introduction to the Marketplace Realities report. But while Greenberg was reporting the balance of his observations tilting in the direction of improved pricing from a carrier perspective, Drummond said, “The long curve, the larger trend, is bending in a positive direction for buyers.”

Noting that “the financial markets remain strong, and unemployment is still low,” Drummond said that while the economic environment remains uncertain for 2023, “our insurance market is, for the most part, telegraphing positive signs for our buyers.”

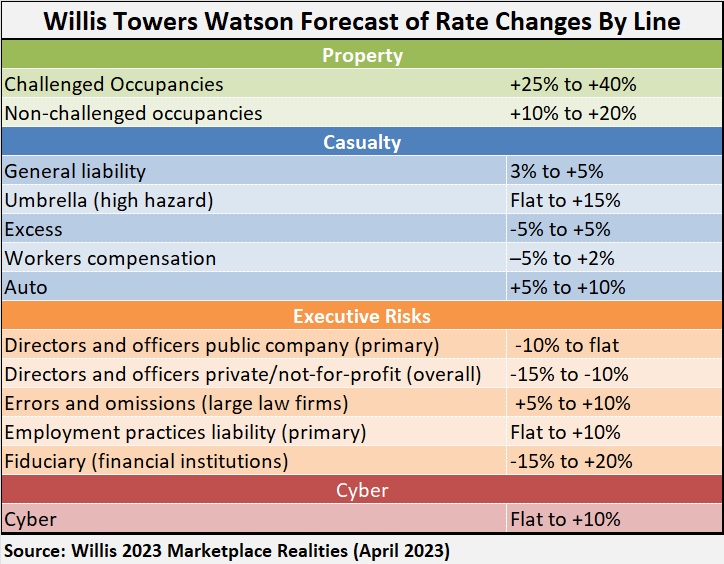

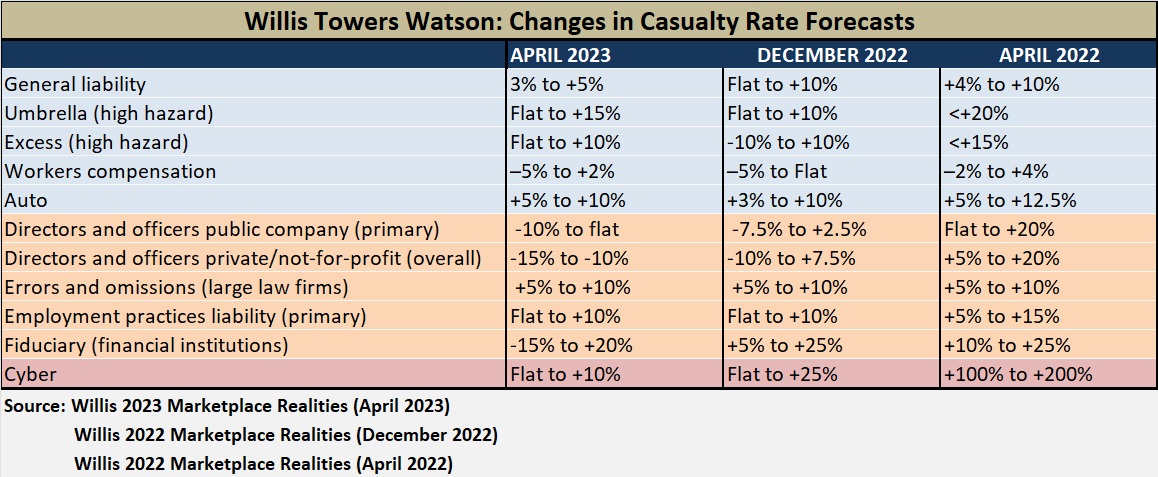

The summary of WTW’s rate forecasts for casualty lines for April 2023, compared to April 2022 and year-end 2022 forecasts set forth below, bears that out, with greater levels of softening apparent as you move down the chart from standard casualty to management liability lines and cyber.

Property, on the other hand, continued to move in the opposite direction, with prices rising for both challenged and non-challenged occupancies.

AXA XL to Acquire S-RM

AXA XL to Acquire S-RM  As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act

As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act  Will AI Be the End of Insurance Agents?

Will AI Be the End of Insurance Agents?