Although analysts at Fitch Ratings estimate that combined ratios for the directors and officers liability line remained below breakeven in 2022, with competition fueling price declines and the economic conditions uncertain, the line is under pressure.

Fitch delivered the conclusion in a report, “U.S. Directors and Officers Liability Market,” yesterday, summarizing a 5-point rise in direct loss ratios, a 9 percent drop in direct written premiums and a 10 percent climb in earned premiums (the lagged impact of prior-year price hikes). The insights are based on an analysis of data from D&O supplemental filings in statutory financial statements.

The information in that supplement does not provide complete information loss adjustment expenses and excludes other underwriting expenses. Fitch approximated the missing figures by using information available for the other liability-claims made line, which includes D&O as well as professional liability and employment practices liability, to estimate a 2022 D&O combined ratio in the 97-98 range. That’s up from 93 in 2021 but way down from an average of 107 for 2017-2020, the report says.

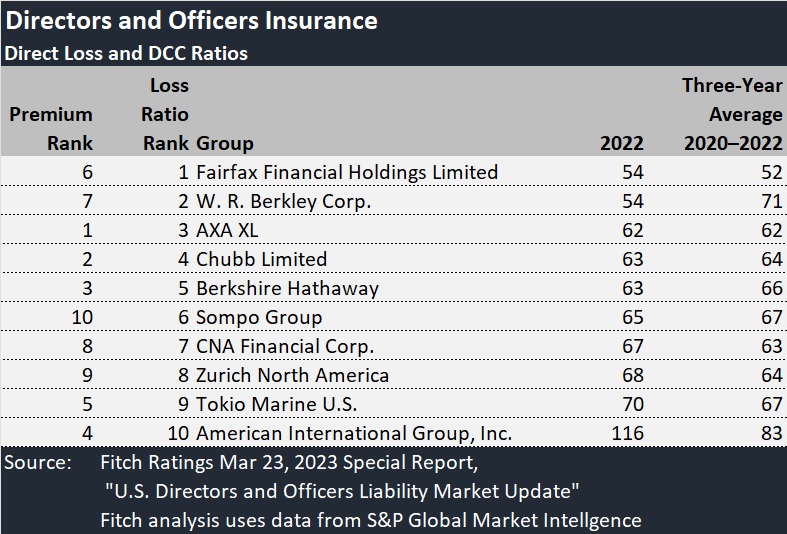

The direct loss ratio (including defense and cost containment expenses but not unallocated adjustment expenses) came in at 69 for the industry, up from 64 in 2021. For individual carriers, these ratios varied from a low of 54 for Fairfax Financial Holdings and W.R. Berkley to a high of 116 for American International Group, a chart in the Fitch report shows.

The 5-point uptick in the industry aggregate figure from 2021 to 2022, following an improvement from an average loss and DCC ratio of 75 from 2017-2020, is just one of the factors that Fitch analysts point to in concluding that the 2021 rebound was short-lived.

“An uncertain loss environment and anticipated reduction in earned premiums in the near term point to a likely increase in the loss ratio to 70 or higher in 2023,” the report says.

While earned premiums were still rising as written premiums fell last year, price declines continued throughout the year, Fitch noted, citing the decline in Aon’s Public D&O Quarterly Pricing Index for three consecutive quarters beginning in second-quarter 2022. The declines came after three consecutive years of reunderwriting with more restrictive coverage and double-digit rate hikes. Aon’s Index for primary policies renewing at the same limit and deductible dropped 5.1 percent in fourth-quarter 2022.

“A more fragile economic environment and persistently high inflation adds risk to the D&O market, particularly if more bank failures, business insolvencies or a sharp equity market downturn materialize,” the Fitch report notes. “D&O claims risk evolves with socioeconomic changes, exposure emerging related to COVID-19, cryptocurrency, cyber risk and other new technology.”

While heightened activity tied to federal court class action merger objection lawsuit filings from 2017-2019 subsided last year, carriers are still seeing adverse loss developments from those years. In fact, the 2018 accident year has generated 10 points of unfavorable development since inception (for the other-liability claims made line in total).

Going forward, growing regulatory and compliance obligations expand potential for litigation tied to ESG, climate risks, and employment practices.

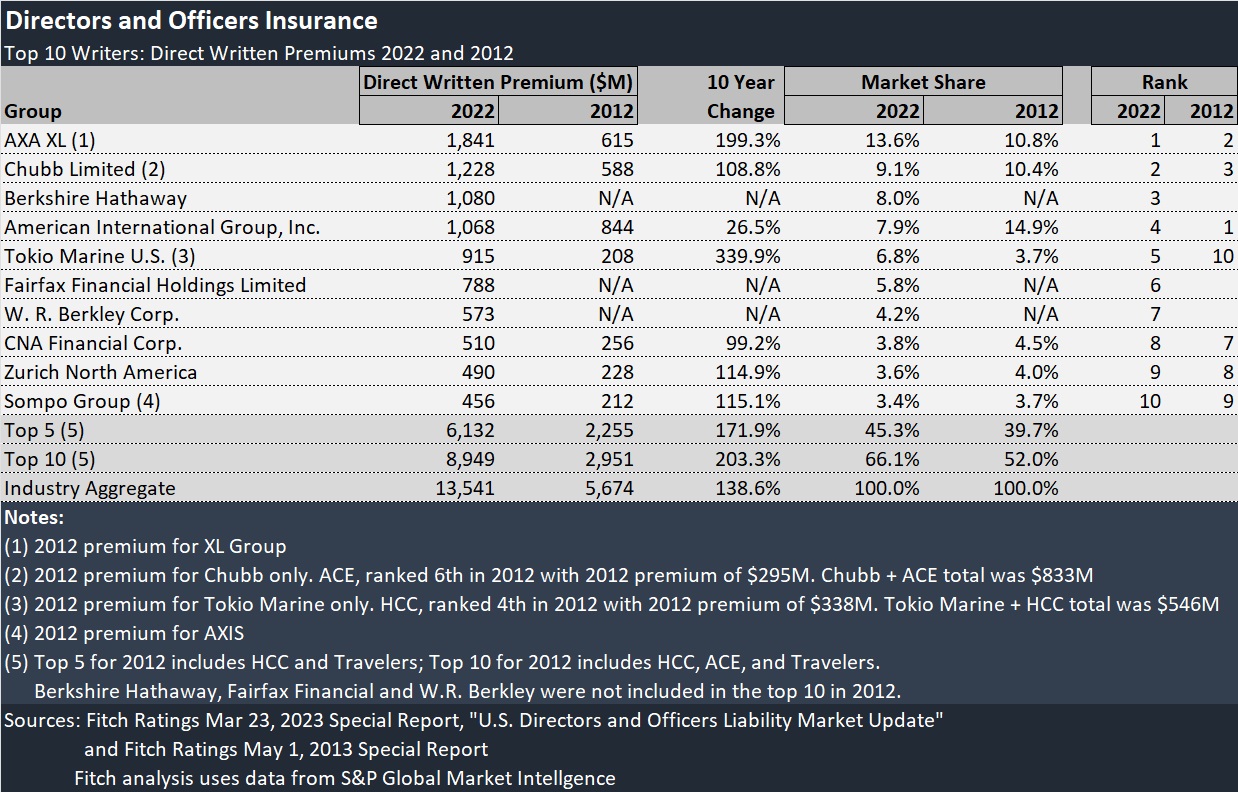

The report also includes a ranking of writers in the U.S. D&O market, based on 2022 direct premiums, putting AXA and Chubb at the top of the heap. AXA and Chubb recorded premium declines of 19 percent and 9 percent last year—and every other carrier listed among the top 10 saw drops in written premium with the exception of Berkshire Hathaway group.

Berkshire’s 2022 deal to buy Alleghany fueled a 78 percent jump in D&O premiums for the combination and landed Berkshire in third place on the premium ranking.

Below, Carrier Management has combined information from yesterday’s Fitch report with a similar report published in May 2013 to reveal the market leader changes over the decade. Several of the top writers in 2012—XL Group (now AXA XL), HCC (now part of Tokio Marine), and ACE (now part of Chubb)—were involved in M&A activity that pushed them up the higher on the ranking.

AIG fell from first place in 2012 to fourth in 2022. While Fairfax Financial and W.R. Berkley climbed into the top 10, Travelers (ranked fifth in 2012) dropped off the list.

With premiums for the top 10 carriers almost tripling over the last 10 years, the top-10 cohort now commands two-thirds of the D&O premiums in the industry, up from just over half in 2012.

The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment  As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act

As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act  Business Uncertainty Drives Changes in C-Suite Strategy: Sentry

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry