Hurricane Ian may result in one of the largest losses in the history of the National Flood Insurance Program and add to its current $20.5 billion debt.

According to a market segment report from AM Best, the projected range of Hurricane Ian losses of between $3.5 billion and $5.3 billion from the Federal Emergency Management Agency would potentially be below the program’s reinsurance attachment. But recent estimates from modeler CoreLogic are much higher — breaching and perhaps blowing through the reinsurance layer.

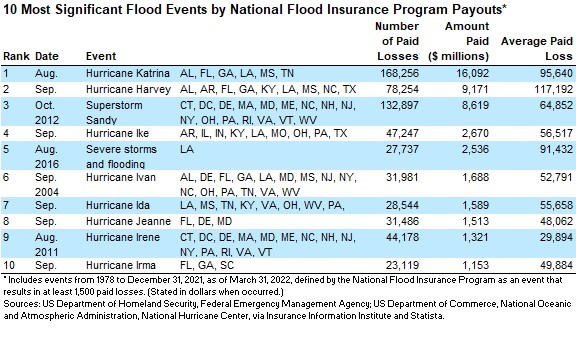

CoreLogic said flood losses from Ian, which made landfall in Florida on Sept. 28, could be between $8 billion and $18 billion. Hurricane Katrina in 2005 caused $16.1 billion in losses to the NFIP, the most ever (see chart). The NFIP had to borrow $17 billion to pay claims related to Katrina and hurricane Rita and Wilma, which also struck in 2005.

Hurricane Nicole, which also struck Florida after Ian, will result in additional losses.

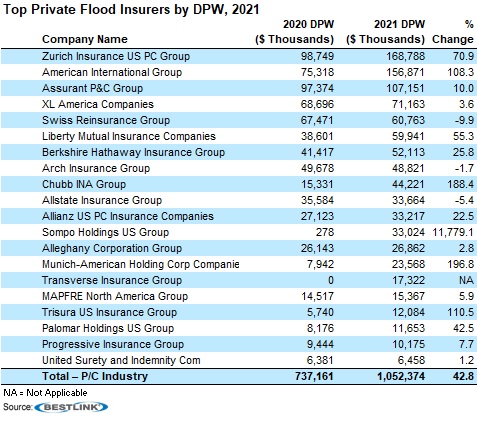

The AM Best report, “NFIP Adrift but Private Flood Insurance Gains Traction,” also pointed out that private flood insurers increased direct premiums written by 42 percent in 2021, the first year Risk Rating 2.0 was implemented to allow for more adequate rates and make private flood insurers more competitive. However, the private flood insurance market remains one-third the size of the federal flood market.

Last year 88 percent of Florida homeowners with flood insurance saw an increase in NFIP premiums and many will see additional rate increases in 2022 and 2023, “likely driving even more homeowners into the private flood insurance market,” AM Best said.

“The full effect of Risk Rating 2.0 has not yet been reached,” the insurance industry rating agency said. “Premium increases are capped at 18 percent a year on single family primary residences. Based on the limitations on incremental rate increases, the flood premium for many homes will not reach their full actuarially sound rate for another four years.”

(AP Photo/Rogelio V. Solis)

East Coast Cities More Dangerous for Drivers According to New Allstate Report

East Coast Cities More Dangerous for Drivers According to New Allstate Report  Viewpoint: Boom in Hyperscale Data Centers Puts Insurers to the Test

Viewpoint: Boom in Hyperscale Data Centers Puts Insurers to the Test  Travelers Builds Insurance-Specific LLM

Travelers Builds Insurance-Specific LLM  The Price of Loyalty: How Higher Premiums Are Reshaping Carrier Retention

The Price of Loyalty: How Higher Premiums Are Reshaping Carrier Retention