As more insurers integrate aerial imagery into underwriting, rating and claims workflows, state insurance departments are responding with a growing body of guidance. While each insurance department bulletin reflects local law and priorities, a fairly consistent regulatory narrative is emerging—one that accepts the technology but insists on disciplined, fair and transparent use.

Insurers’ Uses of Aerial Imagery

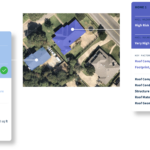

On the underwriting and pricing side, insurers use imagery to get a clearer picture of the risk without always dispatching an inspector. Underwriters use this information to refine eligibility decisions, adjust coverage terms and set more risk‑appropriate premiums. Insurers can confirm building footprints, number of stories, outbuildings, additions and other structures on the parcel. That helps correct misreported or outdated information, align coverage limits with actual exposure and improve rating accuracy.

Over time, periodic imagery allows insurers to monitor changes—for example, a new garage or shed, a newly installed pool, or accumulating debris and lack of maintenance between policy terms. These changes may trigger underwriting review, risk‑mitigation outreach to the policyholder or adjustments at renewal.

In claims handling, aerial imagery is valuable after catastrophes. By comparing pre‑event and post-event images, insurers can quickly gauge the extent of damage across large areas, prioritize inspections and route adjusters to the most severely affected properties. In some cases, insurers can verify roof or structural damage remotely, speeding up claim decisions and payments. The same comparisons can also help flag inconsistencies or potential fraud where claimed damage does not align with what the imagery shows.

Finally, many insurers are feeding aerial images into analytics and AI models. Computer‑vision tools translate raw imagery into structured data—such as roof condition scores, defensible space metrics or hazard indicators—that underwriters and claims teams can use at scale. These scores may influence underwriting tiers, inspection decisions or claim triage rules, making aerial imagery not just a visual aid but a foundational data source in modern property insurance operations.

Common Themes in the State Insurance Guidance

Insurance regulators generally acknowledge that aerial imagery—whether captured by satellite, fixed-wing aircraft or drones—can improve efficiency, reduce inspection costs and enhance risk evaluation. The message is not “don’t use it” but “don’t rely on it blindly.”

Across jurisdictions, state insurance departments emphasize that aerial imagery should typically be one input among several, not the sole basis for cancellations, nonrenewals, declinations or significant rating changes. Where imagery is ambiguous, outdated or low quality, regulators expect insurers to seek additional information, often via a traditional on-site inspection, before taking adverse action.

Quality and Recency of Images

A recurring theme is the importance of the quality and recency of the images themselves. Insurance regulators have expressed concern that imagery can easily mischaracterize a risk: structures may be obscured by trees or shadows, misaligned, or even mis-identified; older images may bear little resemblance to current conditions.

Some regulators are now referencing or considering specific expectations around image recency, and most stress that companies must exercise due diligence to ensure that any imagery used is sufficiently accurate, current and appropriately interpreted.

Risk vs Cosmetic Issues

Another focus is the distinction between risk and cosmetic issues. Several insurance department bulletins caution against using aerial images to justify adverse action based solely on what appear to be cosmetic roof or property conditions—such as staining, streaking, discoloration or minor aesthetic flaws.

Regulators are urging insurers to reserve adverse underwriting outcomes for conditions that materially increase the risk of loss, rather than superficial issues that may not affect the property’s integrity or hazard profile.

Consumer Communication

Transparency and consumer communication are central to this regulatory trend. When aerial imagery leads to an adverse action, many insurance departments now expect insurers to provide specific, meaningful reasons in their notices, rather than generic references to “underwriting judgment” or “hazard increase.”

In some states, regulators encourage or effectively require insurers to share the underlying images or, at a minimum, clearly describe the conditions identified so policyholders understand what prompted the decision. There is also an emphasis on providing insureds with a reasonable opportunity to cure—such as making repairs or removing debris—before a cancellation or nonrenewal is finalized.

Consumer Dispute Mechanism

Closely related is the expectation that consumers have a mechanism to dispute aerial imagery-based findings. Where a policyholder challenges the insurer’s interpretation or presents contrary evidence (for example, a contractor’s report), insurance regulators increasingly expect insurers to follow up, often with a physical inspection, before maintaining an adverse position.

This dispute-and-confirmation step is emerging as a regulatory “best practice” when the imagery is not clearly conclusive.

Use Must Conform to Existing Statutory and Regulatory Frameworks

Finally, state insurance bulletins repeatedly tie use of aerial imagery back to existing statutory and regulatory frameworks. If imagery influences underwriting or rating, regulators expect to see that reflected in filed underwriting guidelines and rating plans, not deployed informally or inconsistently.

And the use of imagery remains fully subject to unfair trade practices, anti-discrimination and consumer protection laws. Insurance regulators are signaling that they will scrutinize image-based practices that result in unfair, unsupported or opaque outcomes.

Taken together, these themes point to a clear policy direction for the insurance industry. Aerial imagery is viewed as a legitimate and useful tool that can modernize underwriting and claims handling. However, insurers are expected to embed guardrails: validating image quality and recency; distinguishing material risk from cosmetic appearance; documenting standards in filed rules; providing clear notice and an opportunity to cure; and allowing challenges backed by follow-up inspection where appropriate.

For insurers, aligning with these emerging expectations is not simply a compliance exercise. It is also an opportunity to standardize and defend internal practices, improve customer experience, and reduce regulatory friction as aerial imagery and related analytics become more deeply integrated into the insurance life cycle.

Interplay between the NAIC AI Model Bulletin and the State Specific Aerial Imagery Guidance

The NAIC’s Model Bulletin on the Use of Artificial Intelligence Systems by Insurers (NAIC AI Model Bulletin) and the growing body of state insurance department bulletins on aerial imagery are part of the same regulatory story: both aim to put guardrails around data‑driven underwriting and claims tools so that they are accurate, fair and accountable. The connection is not just conceptual. For many insurers, aerial imagery is now fed into AI or advanced analytic systems—computer vision models that “read” roof condition, vegetation or external hazards and then inform underwriting, pricing or claim decisions.

State by State: Regulatory Guidance of Insurance Use of Aerial Imagery

- Alabama Bulletin 2025-03

- Delaware Domestic/Foreign Bulletin 150

- Louisiana R. S. 22:1339

- Massachusetts Bulletin 2025-02

- Maryland Bulletin 25-10

- Maine Bulletin 483

- Michigan Bulletin No. 2025-12-INS

- North Carolina Bulletin 25-B-09

- New Hampshire Bulletin INS 25-016-AB

- Pennsylvania Notice 2024-06

- Rhode Island Bulletin 2025-3

- Tennessee Bulletin 25-03

- West Virginia Insurance Bulletin No. 25-02

The NAIC AI Model Bulletin effectively is the overarching governance framework for those systems, while the aerial‑imagery bulletins are issue‑specific applications of similar principles.

The NAIC AI Model Bulletin sets a high‑level obligation: don’t run AI models on bad data. The aerial imagery bulletins specify what “bad data” looks like in this context and require insurers to validate image quality and recency before using it in underwriting and claims—especially when AI or image‑scoring tools are involved.

The NAIC AI Model Bulletin says insurers cannot outsource accountability; they must manage vendor AI and data as if it were their own. Aerial imagery bulletins apply the same idea: insurers remain responsible for how vendor imagery and scoring are used and must build those standards into filed rules and internal controls. A computer‑vision model that systematically downgrades older roofs in certain neighborhoods or misreads shadows as damage can create systematic disparities.

The NAIC AI Model Bulletin provides the framework for testing and monitoring such models; the aerial imagery bulletins set substantive boundaries on when imagery‑based “signals” may be used at all (e.g., not for cosmetic issues, not without confirmation). The AI Bulletin sets a general expectation that regulators should be able to understand and review an insurer’s AI. The aerial imagery bulletins give examiners specific hooks: they can ask to see how imagery is integrated into underwriting rules, how often it leads to adverse actions, whether images are current and adequate, and how disputes and inspections are handled.

In other words, the NAIC AI Model Bulletin is the umbrella policy, and the state aerial imagery bulletins are specific applications of that policy to a high‑risk, high‑visibility use case.

Aligning the insurer’s aerial‑imagery program with both sets of expectations is increasingly the regulatory baseline for responsible use of these tools.

Diversity Crackdown Reverberates Throughout U.S. Boardrooms

Diversity Crackdown Reverberates Throughout U.S. Boardrooms  Zurich CEO Says Staff Let Go as Regulator Finma Imposes Partial Sales Ban

Zurich CEO Says Staff Let Go as Regulator Finma Imposes Partial Sales Ban  Waymo Driverless Cars Crash Less Than Human Drivers: IIHS Study

Waymo Driverless Cars Crash Less Than Human Drivers: IIHS Study  Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak