If there is a bright side to the tumultuous ride that was 2020, it’s the surprisingly agile turn property insurers took to move away from traditional reactive approaches toward more proactive customer experiences.

Executive Summary

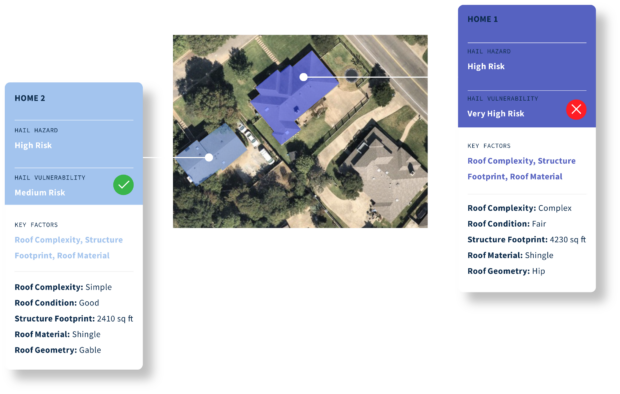

With use cases of geospatial imagery and analytics expanding from claims response to upfront underwriting and pricing, the job of curating data and matching individual images to specific properties being assessed probably isn't a do-it-yourself exercise, according to representatives of two geospatial analytics vendors who help insurers make sense of the visual information increasingly available from manned aircraft and satellites.At the center of this change is the drive in demand for aerial and satellite imagery.

At the onset of its introduction into the property/casualty sector, geospatial imagery typically was procured after catastrophe losses. The imagery provided a way for property carriers to analyze large swaths of damaged properties in a short amount of time, leading to faster claims resolution. Fast forward to the present, and geospatial imagery is being tapped by a variety of departments, including underwriting and risk management, in addition to claims.

According to Neil Pearson, chief strategy officer for Chicago-based Arturo, a spinoff of an American Family Insurance research and development initiative, gone are the days of an agent completing a labor-intensive questionnaire about a property with the insured’s assistance to secure property coverage.