The integration of new technologies into the claims ecosystem is gathering pace as insurance and reinsurance organizations seek to enhance both the speed and accuracy of payments. One example is the advancement in satellite capabilities.

Executive Summary

The potential for satellite technology to revolutionize claims management has long been recognized but has only recently been realized with technological advancements. Satellite-based data can give the insurer a “head start” on the event, according to Stephen Lathrope and Andy Read at the ICEYE, the microsatellite manufacturer and catastrophe monitoring company.Radar satellite technology is helping carriers gain near real-time hazard insights on flood and wildfire perils anywhere on the planet at data resolution levels previously not possible. Such information supports enhanced claims triage, prompt—sometimes instant—claims settlements, efficient resource distribution and sharper post-event capital allocation.

So, how has this technological leap “up” come about?

New Level of Remote Sensing

Traditional optical and radar satellites have been around for decades, but such technology is limited in its ability to image with the frequency, clarity and accuracy needed to support the critical claims-related operational decisions insurers must make during a loss event.

Over the last five to 10 years, however, the emergence of new space technologies and the growth of the private space industry has radically expanded the potential of satellite technology. Two developments in particular stand out.

First, new manufacturing techniques and design changes have significantly reduced the weight, manufacturing times and cost of satellite production. This has facilitated the development of larger satellite constellations which now orbit the Earth much more frequently, imaging relevant areas of the planet much more quickly, with much higher revisit rates.

The other groundbreaking advancement is in synthetic aperture radar (SAR) technology. Unlike optical systems, SAR sensors emit their own energy to illuminate and record objects or areas on the ground. This provides the unique advantage of being able to acquire images day and night, since no sunlight is needed.

Also, SAR sensors can pierce clouds, rain, fog and smoke—a game-changer when trying to assess damage concealed by slow-moving weather systems or smoke from wildfires.

In the past, the key limiting factor with SAR was the cost and scale of the equipment making satellites cumbersome and inflexible and limiting revisit rates. SAR miniaturization means this technology can be integrated into smaller and more agile satellites, which can revisit locations multiple times per day and provide a level of image resolution not possible before.

Combining these two advancements means actionable data can now be delivered directly to insurers— sometimes within hours—as a natural catastrophe event, such as a flood or wildfire, is developing. This provides a completely new level of situational awareness and understanding of the impact on policyholders in almost real time.

Elevated Loss Perspective: Capturing Idalia

SAR imagery and satellite constellations in and of themselves, however, do not provide the hazard insights necessary to enhance the claims process. That is where advances in AI and machine learning and the breadth of specialist expertise from the fields of meteorology and advanced geospatial analytics come into play.

Let’s use the recent example of Hurricane Idalia to demonstrate the stages from image capture to producing the actionable information that delivers the heightened situational awareness so important to the claims process.

On Aug. 26, Tropical Storm Idalia formed in the Gulf of Mexico. At that point, ICEYE’s meteorological team had already been monitoring the development of the weather system for 24 hours. (ICEYE is a microsatellite manufacturer and catastrophe monitoring company. The authors are executives of the company.) On Aug. 29, the day before the storm made landfall in Florida’s Big Bend region as a Category 3 hurricane, the data capture and analysis processes were well underway.

This involves the capture of SAR imagery along the track of the storm plus auxiliary data sources all filtered through a custom algorithm. For flood, sources include elevation models, water sensors and river gauges, plus other open-source evidence of flood-related developments.

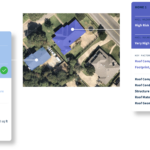

Applying these multiple lenses to the flood means an accurate depiction of the event can be generated that is granular enough to show not only the extent of the water but also the water depth in feet at the individual building level within hours of the flood reaching its peak.

In the case of Idalia, ICEYE analyzed over 7,000 properties that had been inundated by floodwater across Steinhatchee and Suwanee, Fla., and Charleston, S.C., where 535 properties had experienced flood waters exceeding five feet, 623 properties between two and five feet, and 5,844 up to five feet.

Apply this technology to the wildfire context, and a similar level of rapid situational awareness is possible. SAR sensors can pierce the smoke as the event is developing and register whether a particular property has remained intact or been destroyed simply by analyzing the outline of the building.

Supercharging Claims Process

This new level of situational awareness is creating opportunities to ramp up key stages in the claims process, from preemptive actions through to post-event analysis.

Satellite-based data can give the insurer a “head start” on the event. By monitoring weather activity or small-scale wildfires near built-up areas, carriers can put staff on alert for a potential loss. Should the conditions develop, and the data show the emergence of an event likely to impact people or assets, this information can be used to trigger preemptive communications to at-risk policyholders encouraging them to take safety measures to protect lives and locations.

As the loss event evolves and high-resolution impact data becomes available, which in the case of a flood will include extent and inundation information at the property level, or for wildfire the number of buildings destroyed, the carrier can gain a rapid understanding of the scale of the loss. By mapping their property-specific portfolio data to the hazard information for the affected area, they can quickly establish the portfolio impact of the event.

This data feed facilitates a much more rapid decision-making process. Operating with verifiable, “live” information, insurers can allocate resources to those areas or regions most badly affected by the catastrophe. Further, they can be much more precise in their capital allocation as they are able to gain a much more accurate sense of the financial impact much earlier in the process.

Proactive Claims Communications

Communications can be sent proactively to policyholders in the flooded or burned areas, with details of how to make a claim should they have experienced a loss. Based on the number of residential policyholders that have experienced damage to property, insurers can also start to allocate funds and resources for securing temporary accommodation located in non-impacted locations. For businesses, this enables carriers to start calculating the potential business interruption-related costs.

Perhaps most significantly, the data can also support much faster and more effective claims triage processes. If the data shows a single-story property is inundated to a level of eight feet during a flood, the carrier may wish to expedite the claims process and pay the loss quickly—without the expense of bringing in a loss adjuster.

Instances of instant claims payments due to confirmation of loss based on satellite and auxiliary data are on the increase. For example, auto payments in flooded areas are being made where the satellite data is recording a high level of water in an area in which the particular vehicle is shown to be, based on its unique location data.

In tandem, the technology can also be used to spot instances of fraudulent claims. If, for example, a claim for property damage related to flood is made, by using the hazard data mapped to the building characteristics of the specific building, it will be possible to decide whether the submission needs to be red-flagged.

Further, as this hazard insight pool continues to grow, it also becomes a source of claims trend data that is vital to adapting the insurer’s overall strategy to meet the demands of an evolving and more volatile risk environment.

Data-Driven Claims Innovation

Another area in which the application of satellite-based hazard data is having a potentially game-changing effect is in the development of innovative insurance solutions to provide financial support to vulnerable communities in highly exposed regions.

The recent pioneering New York City flood insurance program, involving Swiss Re, Guy Carpenter, the NYC Mayor’s Office, the Center for NYC Neighborhoods, (CNYCN) and the Environmental Defense Fund, provides a clear example of how satellite technology can be used to power parametric solutions to fund speedy payments to vulnerable communities in exposed regions.

The initiative is part of a multi-agency effort to enhance the financial resilience of low- and moderate-income (LMI) households exposed to flood risk in the New York City region. The parametric solution is designed to facilitate rapid cash payments by the CNYCN following a flood event.

As part of the program, ICEYE monitors several NYC neighborhoods for potential flood events. In addition to using imagery from the earth observation constellation, the team also has access to data from New York City’s extensive water sensor network, Flood Net, as well as the ability to monitor precipitation forecasts, river gauges and other open-source evidence of developments likely to cause flooding.

Learn More

Carrier Management featured a series of articles focusing on the use of satellite technology and geospatial information systems for insurance underwriting and claims management in the fourth-quarter 2021 magazine, “Eyes in the Sky: Geospatial Information Systems.”

Articles include:

- Seeing Through Clouds: Why Now Is the Time for Geospatial Technology in Insurance

- Found in Space: How Skytek Tracks Supply Chain Risks—and More

- Eyes in the Sky and Beyond: Why Geospatial Information Matters to Insurers

The award-winning series also included a series of videos and a video roundtable discussion. Links to all the videos are available here: Satellite and Geospatial Insurance System Videos.

By combining high-resolution SAR satellite imagery—which can see through clouds and at night—with very localized data from multiple street-level sources, the impact of a flood across these neighborhoods can be quickly gauged.

When a flood occurs, the hazard data is used to determine the overall flood extent as well as flood depth at the individual building level. This information is provided soon after the peak flooding data is captured and is used to establish whether the payment threshold of the insurance structure has been met or exceeded. If triggered, CNYCN will receive an instant payment to fund cash grants to those affected by the flood. (Editor’s Note: According to a Swiss Re statement, the program leverages Swiss Re Corporate Solutions’ models for precipitation and storm surge-induced flooding. Qualifying flood events are based on a mix of ICEYE’s near real-time satellite data from a dedicated fleet of 24 satellites, as well as on-the-ground real-time sensors and social media.)

Looking Forward, Looking Up

The potential for satellite technology to revolutionize claims management has long been recognized but is only now being realized with recent advancements in vehicles, sensors and AI. Granular hazard data in near real-time is now available in a format that can be easily integrated into existing infrastructure to support more effective claims decision-making at every stage in the claims life cycle. The industry simply needs to look up.

Top photograph: An artist’s depiction of ICEYE SAR microsatellite in orbit over a hurricane

Self-Driving Car Firms Must Address Emergency Vehicle Interference

Self-Driving Car Firms Must Address Emergency Vehicle Interference  Four Insurers Join Ward’s Annual Top 50 P/C Ranking for 2026

Four Insurers Join Ward’s Annual Top 50 P/C Ranking for 2026  NY AG Suing 3M, Other Chemical Companies Over PFAS Pollution

NY AG Suing 3M, Other Chemical Companies Over PFAS Pollution  The Hanover Announces CEO Succession Plan; Roche to Retire at End of 2026

The Hanover Announces CEO Succession Plan; Roche to Retire at End of 2026