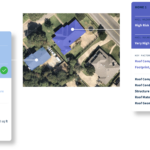

It’s been broadly established that imagery-derived data provides benefits to both property insurers and reinsurers, across a variety of use cases.

Executive Summary

Cape Analytics CEO Ryan Kottenstette outlines four criteria property insurance carriers can use to evaluate imagery-based AI technologies based on his discussions with 60 U.S. carriers. He recommends, for example, that carriers verify whether models can be tuned for specific use cases and gives examples to clarify the difference between precision and recall metrics that measure different types of model uncertainty.These use cases touch most aspects of the carrier workflow, from providing more accurate information at the point of quote to streamlining underwriter decision-making and optimizing inspections. More recently, we’ve even seen the first imagery-derived property condition variables being approved and implemented for use in ratemaking.

Even so, as carriers look at the set of available options today, the landscape of imagery and AI technologies can be challenging to parse. Evaluating new AI outputs and connecting them with specific use cases that affect the combined ratio can be daunting. However, after discussions with over 60 U.S. carriers, I’ve identified four base criteria carriers can use to quickly and quantifiably evaluate offerings.