When State Farm reported a $13 billion underwriting loss for 2022, it was the largest in the auto insurance giant’s history.

A year later, and another record.

The underwriting loss figure climbed to $14 billion for 2023, with a nearly $5 billion underwriting loss for property lines outpacing almost $4 billion of improvement in State Farm’s auto results.

“In 2023, State Farm property and casualty insurance companies experienced growth in policies while also reporting underwriting losses due to continued elevated claims severity and significant catastrophe activity, for both the auto and homeowners insurance companies,” the company said in a media statement.

“While we improved overall auto lines profitability in 2023, our results remain below the level we expect and we’re taking a state-specific approach as we operate,” said Senior Vice President, Treasurer and Chief Financial Officer Mark Schwamberger, who also highlighted the responses of State Farm claims and operations team members, along with the State Farm independent contractor agents, to the widespread catastrophe losses that dented results.

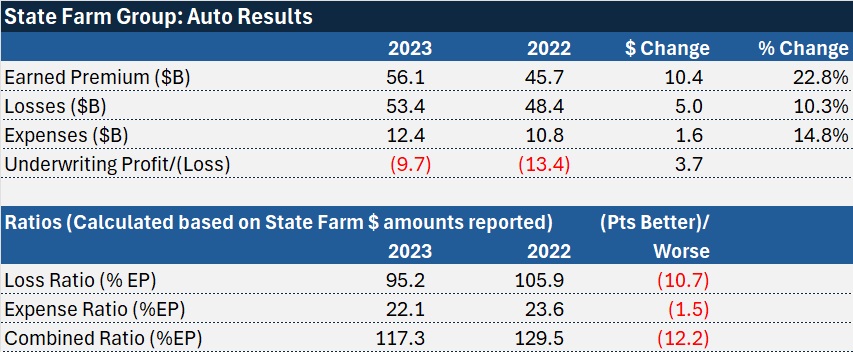

By the numbers, the auto companies recorded earned premium of $56.1 billion, up 23 percent from 2022. Incurred claims and loss adjustment expenses were $53.4 billion in 2023 and other underwriting expenses totaled $12.4 billion, bringing the underwriting loss figure to $9.7 billion for the year—down from $13.4 billion in 2022.

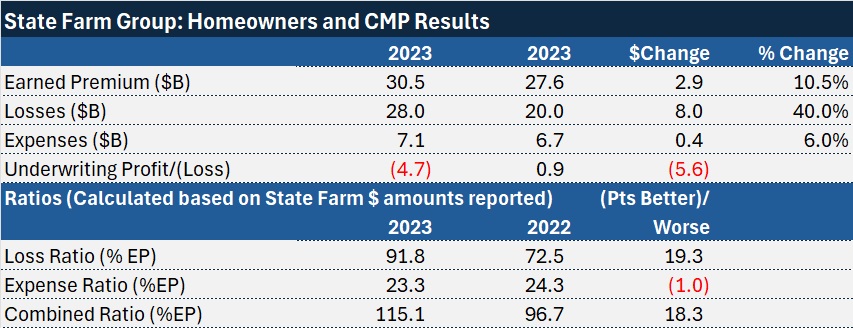

Other P/C lines—homeowners, commercial multiple peril and other lines—generated an underwriting loss $4.7 billion in 2023, compared to an underwriting gain of $849 million in 2022.

Even though State Farm recorded $2.9 billion more earned premiums on its books for the non-auto property lines in 2023, translating to a growth rate of 10.5 percent, incurred losses grew by $8.0 billion, or 40 percent above the total incurred for these lines in 2022.

While the homeowners and CMP lines represent only 35 percent of the P/C companies’ combined net written premium, that damage was enough to impact the overall underwriting result for the whole company.

In total, State Farm said that this P/C group of companies reported a combined underwriting loss of $14.1 billion on earned premium of $87.6 billion. The 2023 underwriting loss, combined with investment and other income of $5.6 billion, resulted in a P/C pre-tax operating loss of $8.5 billion, compared to a $8.3 billion loss reported in 2022 and the $313 million operating loss in 2021.

Total revenue, which includes premium revenue, earned investment income and realized capital gains and losses was $104.2 billion for 2023, up 16.7 percent from $89.3 billion for 2022. On the bottom line, the investment gains helped State Farm to report a lower net loss in 2023 than in 2022—$6.3 billion vs. $6.7 billion.

Auto Improvement vs. Competitors

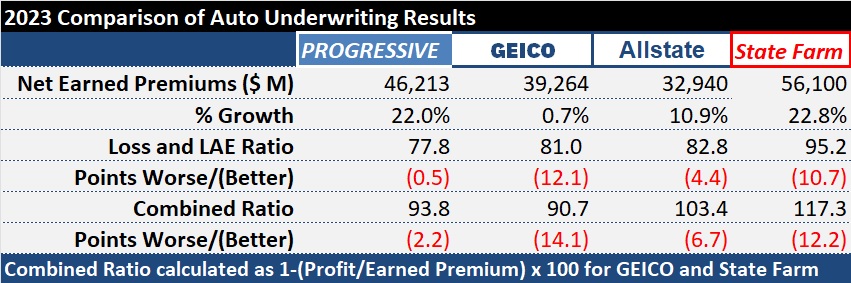

Focusing on just State Farm’s personal auto results, State Farm’s nearly 10.7-point improvement in its loss and loss adjustment ratio was larger than two competitors, Progressive and Allstate. Another large competitor, GEICO, recorded a 12.1-point improvement.

All four carriers reported improvements in underwriting results, but State Farm’s personal auto loss and LAE ratio, at 95.2, remains higher than the auto combined ratios of Progressive and GEICO. (The combined ratios include underwriting expenses).

According to figures compiled by Carrier Management from financial reports of all four carriers, State Farm reported the most growth in auto earned premiums in 2023, with its 22.8 percent growth rate just edging out Progressive’s 22 percent jump in earned premiums.

Still Strong

The State Farm media statement about the financial results stressed the financial strength of State Farm Mutual Automobile Insurance Company in spite of unfavorable operating results. The net worth for State Farm Mutual Automobile Insurance Company ended the year at $134.8 billion compared to $131.2 billion at year-end 2022. The change during 2023 includes an increase in the value of the P/C companies unaffiliated stock portfolio, driven by increases in the U.S. equities market, partially offset by the P/C group of companies pre-tax operating loss, the statement said.

According to the statement, the State Farm life insurance companies paid out more than $725 million in dividends to policyholders, and issued a record $118 billion in new policy volume bringing the year-end 2022 individual life insurance in force to $1.1 trillion.

The two life companies, State Farm Life Insurance Company and State Farm Life and Accident Assurance Company, reported premium income of $6.5 billion and net income for 2023 was $1.2 billion.

The State Farm insurance operations consist of 14 P/C companies and two life insurers, each of which is managed on an individual affiliate level. In addition to auto, homeowners and CMP, the P/C companies are also engaged in health and reinsurance lines of business. The life companies are primarily engaged in individual life insurance and annuity business.

In addition, State Farm group makes third-party products, such as annuities, banking, health, mutual funds and pet medical insurance.

A Matter of Trust

A Matter of Trust  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment  California Utility’s Idle Transmission Tower Caused Deadly ’25 Eaton Fire

California Utility’s Idle Transmission Tower Caused Deadly ’25 Eaton Fire