The Pennsylvania Insurance Department (PID) is reminding insurers of their obligation to conduct a physical inspection to confirm the type and extent of damage to a roof supposedly evidenced by aerial imagery.

The regulatory agency said it has received consumer complaints regarding insurers using aerial imagery canceling or not renewing policies due to the condition of their roofs. The department said it found that the “aerial images in question often did not clearly demonstrate significant roofing degradation or damage, but merely showed discoloration, streaking, or other cosmetic issues that should not be the sole basis for canceling or nonrenewing insurance policies.”

in a May 29 bulletin, Insurance Commissioner Michael Humphreys stressed that the department “does not seek to broadly restrict the use of aerial imagery” but wants insurers to provide consumers an opportunity to challenge the results or fix any confirmed problems before their policies are canceled or not renewed.

“This notice reminds insurers of their responsibilities in administering homeowners’ policies consistent with state law. The department supports and encourages innovative ways to identify risk and deliver a better insurance product to Pennsylvanians. That said, such innovation needs to be reasonable,” Humphreys said in a press release. “Some of the aerial images that we’ve seen used to take adverse actions against policyholders barely identify the structure of the home, much less the detailed condition of the roof and whether it needs to be repaired or replaced.”

The department also said it has received complaints that insurers are not providing consumers with proper notice of cancellation or nonrenewal, including the specific reasons for these actions. The bulletin reminds insurers that they must clearly communicate the specific reasons for seeking policy cancellation or nonrenewal, enabling consumers to take necessary remedial actions or to seek alternative coverage if the policy is terminated due to unresolved issues.

The bulletin also reminds insurance that under the state’s Unfair Insurance Practices Act, they:

- Must state specific reasons: Insurers must provide both the legal and factual reasons, as allowed by law, for the termination of policies in force for 60 days or more;

- May cancel or nonrenew where there is a substantial change or increase in hazard: Insurers may cancel or nonrenew a policy in force for 60 days or more if there has been a significant change or increase in hazard after the policy was issued, or a substantial increase in hazard due to willful or negligent acts or omissions by the consumer;

- Must prove the risk has increased and has been substantial: Simply characterizing a condition of a property as unacceptable fails to establish an increase in risk required for policy termination;

- May not cancel or nonrenew policy on suspicion: Mere suspicion or question of a change is not a sufficient reason for policy nonrenewal or cancellation; and

- Must provide prior notice and an opportunity to cure: Insurers must give consumers prior notice and a chance to remedy any hazardous conditions to their home, especially if the hazard is not immediately obvious to the consumer.

The aerial imagery reminder comes after the department on April 9 issued guidance on insurers’ use of artificial intelligence (AI) based on a model by the National Association of Insurance Commissioners (NAIC).

The AI notice advises insurers that their use of AI must comply with all applicable insurance laws and regulations. It includes recommended best practices for how insurers obtain, develop and use certain AI technologies and systems, and advises insurers on what information they may be asked to provide during a regulatory investigation or examination.

The guidance on AI outlines specific guidelines for governance structures, accountability, monitoring, audit protocols, and training.

This article was originally published by Insurance Journal

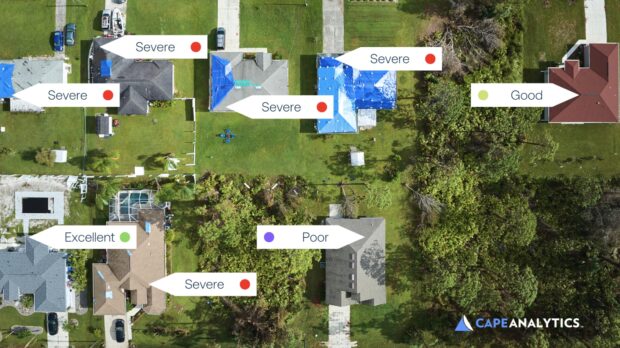

Featured image: Aerial view of roof condition from Cape Analytics (2022)

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Mapfre Acquiring Tuio Stake; Bolsters Commitment to AI, Digital Innovation

Mapfre Acquiring Tuio Stake; Bolsters Commitment to AI, Digital Innovation