The world is progressively witnessing heightened interconnectedness. Sensors present in physical objects capture data and link to digital communication networks. The data can then be analyzed, precipitating the execution of “smart actions.”

Executive Summary

“IoT data will allow insurers to differentiate risk much more granularly than workers compensation code and payroll,” observe The Hartford’s Dan Campany and IoT Observatory’s Matteo Carbone in this outline of The Hartford’s strategy for applying IoT innovations across commercial lines.Updating an earlier article they wrote for Carrier Management in 2021—”A Repeatable Model for Using IoT to Transform Commercial Insurance“—the authors lay out The Hartford’s vision to use sensors and data to prevent losses, improve underwriting execution, and create differentiated value with new products and services. They go on to describe the repeatable process that allowed The Hartford to engage commercial property, commercial auto and workers compensation business units in the IoT innovation journey.

This interconnectedness paradigm, referred to as the Internet of Things (IoT), is becoming omnipresent in our personal lives as consumers and via its adoption by corporate entities. Examples include the proliferation of “smart” devices in the home for security and convenience, using mobile devices as keys to access hotel rooms, tracking fitness and physical activity with smartwatches, and coordinating aircraft by air traffic control. Notably, Statista reports a global tally of approximately 15 billion interconnected devices.

It is not a question of “if” but “when” the IoT paradigm will reshape most industries. Data collected by IoT devices has enormous potential to transform and improve business processes, even in the insurance industry. The insurance sector has not been excluded by the adoption of the IoT interconnectedness paradigm.

In our previous article in 2021 (“A Repeatable Model for Using IoT to Transform Commercial Insurance“), we noted that the level of maturity in commercial insurance was still lower than in personal lines, “with many insurers clearly seeing the potential applications for IoT, [but] still figuring out how to make the transition from ‘interesting technology’ to ‘scalable ROI.'” Even after a span of two years, we characterize the level of IoT integration within the commercial insurance domain as nascent. A considerable number of carriers have yet to embark upon experiments with these solutions. Consequently, a noteworthy portion of the market continues to exhibit a constrained understanding of the IoT innovative potential.

Nevertheless, members of the IoT Insurance Observatory regularly discuss successful IoT applications within commercial insurance with their think tank peers. These insurers share lessons learned using IoT data in commercial auto, commercial property, construction, marine, agriculture, workers compensation and even medical malpractice insurance. These real cases showed concrete impacts on the insurance processes by:

- Mitigating or even preventing losses.

- Selecting risks and accurately pricing them.

- Enhancing the claims processes.

- Insuring risks in a new way, or even extending the risk appetite to new risks.

The Hartford has prominently positioned itself in this surge of innovative practices within commercial insurance. The journey of The Hartford IoT Innovation Lab—created in 2019 and introduced in our previous article—has built a successful practice using IoT data. In the past two years, they have experimented with solutions that fit business units’ requests and implemented the use cases that showed a tangible value. Over time, adoption results in accumulating data for advanced analytics at the portfolio level, unlocking more use cases and benefits.

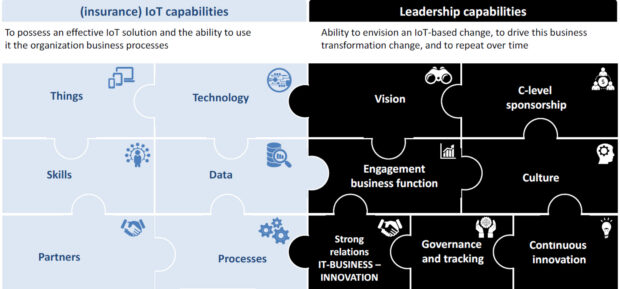

The Hartford’s IoT vision is to use sensors and data to 1) prevent losses, 2) improve underwriting execution, and 3) create differentiated value with new products and services. With the vision unchanged over four-plus years, early successes have bolstered sponsorship and business function engagement.

A specialized set of capabilities on devices, skills, data, partners and processes has been forged initiative after initiative. The Lab has built a repeatable model for experimentation continuously reinforcing both the (insurance) IoT capabilities and the leadership capabilities. The model’s key pillars—common to different use cases and across different business lines—are:

- A use case always starts with clearly established strategy: What problem are we trying to solve? For which customers? How big (prevalent)?

- A deeper assessment of the target customer follows—building their profile, identifying their needs, and the experience that will solve their pain points.

- The next leg of the journey, the approach, then begins by testing and incubating new capabilities that deliver near-term value at the account level to both the customer and insurer, which promotes more investment and adoption.

In The Hartford’s continuous innovation journey, the core focus is to:

- Extend the awareness, the understanding, and the culture or mindset necessary for IoT innovation more deeply into the enterprise by continuing to deliver increased value.

- Further broaden engagement both among different functions within a business unit where IoT programs have been introduced and across different business units.

- Scale the successful experiments.

Repeating the Process: From Construction to Existing Property

In 2021, we wrote about The Hartford’s strong water damage prevention results in construction. In some cases, risk engineers recommended technology and real-time mitigation to customers; for others, the use of damage prevention technology and mitigations were required in order to be eligible for the coverage in accordance with documented underwriting guidelines. Over the course of five years, the approach in construction has resulted in a $25 reduction in expected losses for each dollar invested in IoT prevention solutions.

The successful experience has precipitated an extension into other customer segments and property lines, most notably middle- and large-size buildings. In a continuous succession of experiments, this risk prevention capability for properties is currently being scaled and institutionalized into the core activities of the middle and large commercial segment.

Because of the compelling loss prevention results, The Hartford is offering these prevention solutions to the customers in the portfolio and fully funding the technology solutions for office buildings, medical centers and educational facilities countrywide. For other types of occupancies, the customer may pay part of the costs because the resulting loss mitigation is insufficient to fully cover the cost of the sensor. This is a strong customer value proposition showing less than 7 percent of fully funded customers opting out when the IoT solution is offered.

However, just giving away free sensors doesn’t make adoption easy. It is essential to identify and engage with the right employee inside the policyholder’s organization in order to ensure adoption of the risk mitigation solutions. The Hartford sees a concrete opportunity to continue harvesting additional benefits, with the goal of achieving a three- or fourfold increase in the current level of penetration (15 percent) on the targeted customer portfolio. To do that, it is imperative to remove friction between underwriters, loss control experts, brokers and policyholders with streamlined process enhancements, better data quality and automation.

The carrier has observed a virtuous cycle where success creates positive awareness, yielding more adoption and support, leading to the expansion to more business classes over time.

The Hartford vision at this point is also to integrate IoT prevention solutions as a core component of its standard business model to insure properties. The IoT Innovation Lab is transitioning funding and ownership of this capability to the business unit, which the carrier believes is the right place to take the last leg of the journey, so the IoT team can refocus on “what’s next,” such as the extension to other use cases.

Repeat Again: Commercial Auto Telematics

The IoT skills developed along the journey by the IoT Innovation Lab have also been leveraged in the commercial auto telematics field for the past 18 months. A coordinated enterprise approach has been supported by strong sponsorship from senior leaders. Telematics is becoming a critical component of a winning commercial auto strategy because of the opportunity for competitive advantage: increased pricing granularity, reduced selection bias, accurate exposures identification, behavior modification, etc.

In 2022, an enterprise-wide Commercial Telematics Acceleration Team was created. It comprises business unit auto product leads, IoT tech and data, risk engineering, and claims. Their role is to accelerate and support the advancement of telematics-driven use cases in commercial auto. Initially, the effort was focused on clarifying the vision, creating a common understanding and vernacular, and providing a mechanism to coordinate and share learnings across segments.

The primary focus has been on fleets that already have telematics installed, so relationships with most of the top 10 telematics service providers in the U.S., and many car makers have been built. Multiple experiments exist across various customer segments with different strategic objectives (such as behavior modification, exposure validation and premium leakage, and claim investigation).

Much of the initial focus of experiments has been on evaluating the effectiveness and logistical considerations of customer incentives to share data (pricing, subsidies, services, usage-based insurance), and deriving a reasonable range of loss prevention benefits from tech-driven behavior changes (e.g., distraction, tailgating, speeding) with various technologies, approaches and customer segments. Recently, a cloud database and API (application programming interface) connectors to land the data have been introduced. Leveraging these, the team has provided a first generation of insight dashboards to underwriters and loss control experts, allowing them to see unexpected outliers in behaviors and exposures.

Cumulatively, these commercial auto initiatives have:

- Delivered specialized “enabling” IoT capabilities for this segment of business.

- Begun to deliver value to customers and enterprise stakeholders.

- Accumulated data for future advanced modeling applications.

Next Up: Workers Compensation

Worker safety has been a third area at the center of the IoT Innovation Lab effort since inception. The strategy is to win and retain profitable business by improving customer value with better ROI on employment expenses and lowering their total cost of risk as a natural by-product. Ultimately, there is a virtuous cycle where safety technology investments reduce claims, which unlocks differentiated customer value in the form of lower premiums, higher productivity, improved employee morale, less lost time to injury, etc. With better customer value comes profitable growth, which unlocks the opportunity to invest for expanded customer value and the advantages of large datasets.

The Hartford’s IoT programs for worker safety put in place over the past few years have revealed a precious set of lessons learned about the technology, the target segments and the insurance approach.

Technology. Wearable devices include: harnesses, belts, arm bands, hard hats, watches, etc. They can measure a variety of non-biometric safety-related attributes: lifting, twisting, bending, steps, elevation, falls, force, location, temperature, humidity, proximity to hazards, etc., as well as biometrics such as heart rate, hydration, blood pressure, blood oxygen levels, etc. The Hartford’s focus has been exclusively on non-biometric wearable devices dedicated to ergonomic safety to mitigate the risk of injuries related to pains and strains.

Wearable devices follow the worker wherever they go on the worksite and provide deep insights at the employee level, which can be evaluated by the employer across job functions, shifts and other meaningful segmentation factors. This makes them effective at isolating ergonomic risk levels for both coaching and training on proper lifting technique, and at systemic identification and engineering of root cause risk factors (e.g., ergonomically incorrect workstation designs). Many ergonomic wearables also have built-in haptic feedback (vibration warnings) that alert a worker in real time when they are performing an unsafe movement and as a reminder to follow best practices for safe material handling.

Another technology category, computer vision, is a more nascent but rapidly evolving safety technology one. Computer vision algorithms or artificial intelligence (AI) can review video footage and identify key attributes much like a human, but with much greater speed and lower cost. The AI can be trained to look for a broad array of environmental and behavioral risk factors such as: lack of personal protective equipment, unsafe lifting, unsafe forklift operation, proximity of workers to equipment in operation, jumping/falling, etc. These solutions can generally be implemented with modern cameras that are already installed onsite. Whereas wearables follow workers around a worksite, cameras monitor a particular zone of activity.

Currently, The Hartford sees opportunities for both these technologies in a risk engineering team’s toolkit. Enterprises have different preferences between the two. Some customers have concerns about imagery being too invasive and privacy issues. Others are concerned about how employees will view “being tracked” by wearables and how to incentivize employees to wear the devices all day, every day. For some job functions, a wearable, depending on the form factor, can create an additional risk of injury or detract from productivity, whereas cameras do not affect a worker.

While cameras are also attractive for the breadth of risk factors they can detect, wearables offer rich data and insights about ergonomics that are not currently possible via a camera.

Target segments. The Hartford business cases have been more sustainable with material-handling exposures (such as manufacturing, warehouse and distribution) due to the substantial opportunity to reduce preventable losses.

Adoption has been better in self-insured operations compared to guaranteed cost policyholders, given the alignment of incentives to reduce injury claims.

Concerning technological interventions aimed at enhancing worker safety, it is noteworthy that all except the most sizable and sophisticated employers stand to reap advantages from the support extended by their insurers. This is primarily due to the intricate nature of technology and data involved, which encompasses considerations of privacy, analytics, emerging legislation and the multitude of vendors. Building the requisite capabilities at an economically viable scale remains a pivotal factor.

The Hartford has focused on middle and large employers (50-plus employees per location). However, bringing safety solutions to smaller customer segments is becoming more feasible as the prices of technology solutions continue to decrease.

Experiments have reinforced the awareness that free devices do not create value if they don’t improve safety. So, IoT must be the foundation of a systemic change in the risk environment or employee behavior.

Similarly, employers with a dedicated safety or risk manager on staff, who is influential in the company’s culture and financial decisions, are more likely to affect change based on data-driven safety improvement recommendations.

The ideal target client is one who has room for improvement in claim outcomes and a strong desire to improve. Too often, however, that combination proves difficult to find as employers with solid safety cultures tend to already perform well from a claims perspective relative to their peer group and vice versa. This is where the approach needs to contemplate how insurers and their risk engineering teams can create a compelling value proposition to incentivize technology-driven safety improvements.

Approach. Most deployments have focused on introducing behavioral changes to curtail the expected losses. The data collected, once analyzed, provides awareness of current hazards to the risk engineering teams and helps to suggest changes for a safer workplace. It is worth noting that the extraction of actionable insights for safety and risk engineering constitutes a nascent competency, the application of which needs to be learned on a customer-by-customer basis.

A necessary element is the policyholder’s genuine commitment and investment in change management and better job stations. Various entities are testing policyholder incentives, such as premiums and profit-sharing incentives in the market. Further, there are untapped opportunities to enhance the effectiveness of employee-level incentive programs for behavioral improvements; there are no existing best practices beyond normal management routines.

This effort should be considered in the perspective of The Hartford’s broader vision: to help businesses stay in business by maximizing their most important asset—their employees. Safer, happier, more productive workers are good for business.

The ambition is to change the paradigm to compete on the cumulative value of a multitude of capabilities, including both services (risk engineering, tech advice, data insights) and risk transfer. The workers compensation insurer of the future will master the IoT capabilities across its business functions.

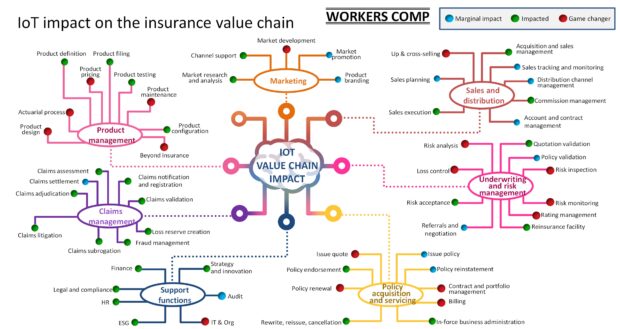

Insurance Value Chain

For workers compensation, IoT capabilities have the most transformative impact on underwriting and risk management activities, such as risk analysis, loss control, risk inspection and risk monitoring. This technology should be universally adopted in the risk engineering and loss control functions for both initial/episodic reviews and long-term ongoing monitoring. IoT-based curated insights can support the organization and the execution of loss control teams’ activity.

Policyholder payroll audits can be revolutionized, or even not performed at all. IoT data will allow insurers to differentiate risk much more granularly than workers compensation code and payroll. Not every worker in the same class code has the same risk; not even every worker in the same job function at the same employer on the same shift has the same risk.

This evolution will unlock the opportunity to innovate the product structure to accommodate this better view of risk and may involve integrating IoT insights, or even replacing payroll, as the driver of exposure. For example, an insurer might consider using metrics such as the number of lifts performed, or hours worked multiplied by the risk level during those hours, as alternative measures of exposure.

Drawing a parallel to the utilization of telematics data in the realm of personal auto insurance, described in another article in this edition (“Nationwide Insurance: Using a Decade of Learnings to Create Next Generation Telematics Solutions ” by Kelly Hernandez and Matteo Carbone), in workers compensation, too, this kind of evolution represents a game-changer for product management activities, rating management, and the entire cycle of policy issuance and servicing activities (issuing a quote, billing, managing contracts and portfolios, renewing policies).

In the claims area, when workplace accidents actually occur, IoT data may not have the same type of game-changing impact on insurer claims management activities that it is having in personal auto. (See related article, “The Transformative Potential of Telematics Innovation: Personal Auto,” for discussion of detection and fraud management). Still, the IoT data will be a valuable supplement to the decision-making process, likely accelerating validation and assessment timelines and bringing down loss adjustment expenses.

Bending the Casualty Curve: Why Casualty Analytics Is Approaching Its Inflection Point

Bending the Casualty Curve: Why Casualty Analytics Is Approaching Its Inflection Point  IIHS Reveals Driver Protection Ratings for 9 Commercial Vehicles

IIHS Reveals Driver Protection Ratings for 9 Commercial Vehicles  ‘We’ll Want Some Proof’: State Farm CEO’s Take on NY Auto Insurance Reforms

‘We’ll Want Some Proof’: State Farm CEO’s Take on NY Auto Insurance Reforms  Most American Workers Are Checked Out, and Like ‘The Office,’ Their Bosses Are the Last to Know

Most American Workers Are Checked Out, and Like ‘The Office,’ Their Bosses Are the Last to Know