The prospect of property/casualty insurers and reinsurers adding information from geospatial imagery to their toolkits for underwriting, product development and claims handling isn’t an entirely new idea. But it’s one that is getting a lot more attention in 2021.

Executive Summary

CM Guest Editor and CB Insights Analyst Mike Fitzgerald hosted a Roundtable bringing together participants in the world of geospatial information systems, seeking to understand reasons behind the increased interest in applying imagery data to existing and emerging insurance problems. In Roundtable highlights here, representatives of a commercial insurer, a global reinsurer, a flood mapping specialist and an MGA creating specialty parametric insurance products describe a confluence of technology developments that are making satellite imagery more accessible to insurers of all sizes, and broader environmental concerns that are fueling demand, as well as some remaining obstacles to broad-based acceptance by insurance underwriters.Watch the entire Virtual Roundtable—”Seeing Through the Clouds: Satellites in Insurance,” on the Carrier Management channel of InsuranceJournal.TV

(Editor’s Note: At the time this article was first published in late 2021, Fitzgerald was a principal insurance analyst for CB Insights. In 2022, he joined SAS as an advisory insurance consultant.)

Industry giants including AXA XL and Swiss Re have been using geospatial information systems (GIS) for property risk modeling and pricing, post-catastrophe loss adjusting, parametric insurance product innovations, and climate sustainability models for a number of years. But now the rest of the industry is starting to get on board, including insurers serving small business customers and homeowners, a panel of participants in the GIS space told Carrier Management recently. (See related article for GIS definition.)

“Why now?” asked Mike Fitzgerald, principal insurance analyst for CB Insights, kicking off a Carrier Management Roundtable event on geospatial information systems titled “Seeing Through the Clouds: Satellites in Insurance,” in mid-October.

Bessie Schwarz, the co-founder and chief executive officer of Cloud to Street, a team of scientists that harness the power of satellites for flood mapping, agreed that “this love affair [has] only really now started to take off and go deeper into the market”—some 10 years after the start of what she referred to as a “massive revolution” in micro-satellites. Offering her take on why this moment in time is different, Schwarz said the development of technologies outside of space tech has made data insights from satellite imagery more accessible. And beyond that, an appreciation of risk is a key factor driving demand for insurance products leveraging information from satellite imagery—and from insurers and consumers.

“Our users on the ground, even the sophisticated ones within the insurance industry, don’t actually care about the millions of pixels we’re crunching all the time or the cool new algorithm that we just published on it…They just want the answer to their question, which is often just a CSV table of their assets and which ones are flooded today and not.”

Bessie Schwarz, Cloud to Street

“None of this would be possible without two other technical revolutions,” she said, referring first to cloud computing. “That’s finally enabled planetary scale computing at relatively low cost,” she said. The other is artificial intelligence, or more specifically the computer vision subset of AI technology. “Computer vision has completely, in many ways, leapfrogged what we’re able to do in terms of deriving insights from the satellite imagery themselves,” she said. “We just don’t even in many ways understand how machine learning can see through clouds in certain places to see the flood underneath. But we’ve published papers on it. It’s quite effective.”

In addition to those papers, scientific analysis from Cloud to Street was published in Nature magazine as the publication’s August 2021 cover story (“Satellite imaging reveals increased proportion of population exposed to floods“). Another co-founder, Dr. Beth Tellman, who is also chief science officer of Cloud to Street, was the lead researcher for the paper, which was published along with the largest open database of flood maps in the world. Combining the flood maps created from satellite images, instead of typical ground measurements, with population data, the researchers found that 58-86 million people moved into areas with satellite-observed inundation between 2000 and 2015, representing an increase of 20-24 percent in the proportion of the global population exposed to floods—10 times higher than previous estimates. (Related article, “High and Rising”)

Such findings open up opportunities for insurers and brokers to enter new markets with flood insurance products using parametric triggers, Schwarz told Roundtable listeners, referring to Cloud to Street partnerships with the P/C insurance and reinsurance community—most notably, as a Willis Research Network partner. “We’re beginning our work with those partners in the U.S. in early 2022,” she said, stressing that beyond the breakthroughs in science, the demand for new insurance products is driving an interest in satellite technology. “I really think the massive amount of catastrophes and the amount of uncertainty that really everyone is feeling—whether you’re a corporate with supply chain risk all around the world, in China where the massive floods happened this summer, or you’re a homeowner who’s looking at sea-level rising in a more serious way—[has] everyone looking at ways where they can take their risk more seriously and where they can diversify their risk.”

“That’s going to drive demand in ways that will converge all the things we’re talking about”—satellite technology, cloud computing capabilities and AI—”in really fascinating ways,” Schwarz predicted.

“There is a sense of urgency in organizations like ours to both update our models with current event data, with footprints, with damage assessment—and also to build very fast capabilities to respond to these events.”

“There is a sense of urgency in organizations like ours to both update our models with current event data, with footprints, with damage assessment—and also to build very fast capabilities to respond to these events.”

Pranav Pasricha, Swiss Re

Pranav Pasricha, global head of P&C Solutions for Swiss Re, spoke to the increased demand from insurers and reinsurers as climate-related events continue to impact the industry. “It’s super critical that we keep evolving our catastrophe risk models that we have for all of these perils…Historic events in the last 12 months—the floods in India, European floods, [Hurricane] Ida, you name it. We all know what we’re dealing with. And so, there is a sense of urgency in organizations like ours to both update our models with current event data, with footprints, with damage assessment, and also to build very fast capabilities to respond to these events, to be able to help our carrier partners respond to Ida. Where do I send my adjusters? For which clients can I just write a check to and get clients and consumers back on their feet? For us, this is a priority,” he said.

“As a major global reinsurer, being the backstop to a large part of the global insurance industry, we feel it’s our responsibility to drive innovation and progress in the industry. There’s a lot of change going on in the industry, and we are there to help our insurance partners be future-proof, to improve their underwriting results and then to navigate these changes,” Pasricha said. (Related article, “Why Swiss Re Cares About GIS”)

Providing a commercial insurance company perspective, Giacomo Favaron, senior specialist, Insurance Pricing for AXA XL, said the decreasing cost of satellite launches is something that can’t be overlooked in answering Fitzgerald’s “Why now?” question. “On the engineering side, we have seen a huge technical progress, because satellite manufacturing saw a big decrease in production costs. Satellites are getting smaller, lighter and therefore generating a lower payload cost per launch.”

“Also, the advent of reusable rockets has slashed overall cost per launch. And that’s why we see now the coming of constellations of satellites put in orbit, made of cheap satellites, maybe with a short lifespan, that can give you that almost near-perfect global coverage with very brief resolution time that wasn’t possible just few years ago,” he said. According to Favaron, before the advent of reusable rockets, the average cost per kilo per launch was $9,000 or $10,000 compared to just $1,400 or $1,500 per kilo today. (Editor’s Note: A kilogram is roughly 2.2 lbs.)

“The majority of the market seems to focus on the post-event analysis rather than the data harvesting and data enrichment of what could be available. There’s probably a focus on around what the human eye can see, rather than what actually a sensor can give you back.”

“The majority of the market seems to focus on the post-event analysis rather than the data harvesting and data enrichment of what could be available. There’s probably a focus on around what the human eye can see, rather than what actually a sensor can give you back.”

Giacomo Favaron, AXA XL

“There are definitely more and more companies jumping on this new trend, and we’re going to see the increase of these massive constellations in the very near future,” he said, adding that as more players compete in the market for satellite launches, those costs will fall even more.

Fitzgerald said there also has been a business model innovation for satellite launch services, referring to SpaceX’s Rideshare program. “We’re used to hearing what rideshare is on the Earth [with] Lyft and Uber. But they changed their approach to pricing to where you can have multiple of these micro-satellites on the same launch and share the fixed costs of getting up there,” he said.

Still, even as launch costs decline and cloud capacity increases, insurers face the need to understand ever-growing quantities of higher-precision data, which don’t quite mesh with historical data used for underwriting and pricing. For some, that adds layers of complexity and cost that are best borne by groups of insurers or consortiums, Roundtable participants said.

“Even if we think about what is currently available, we are just scratching the surface of how we are using satellite data,” Favaron said. “The majority of the market seems to focus on the post-event analysis, for example, rather than the data harvesting and data enrichment of what could be available. There’s probably a focus on around what the human eye can see, rather than what actually [a satellite] sensor can give you back,” he said.

Recalling the early 2000s, when state-of-the-art satellite instrumentation supplied panchromatic data (from the visible RGB spectrum), Favaron reported that today’s satellite constellations supply information from 21 spectral bands at different resolutions. “You have temperature radiometers, technical pressure radars, microwave radiometers…”

“The majority of the [geospatial information] products I’ve seen around [are] still imagery-type products. Maybe they come [paired] with some artificial intelligence model behind for recognizing objects on the ground, [or] recognizing if a place might be under water or not…But the real treasure, in my opinion, is in all those other instruments that are able to capture what the human eye cannot see because we only see a very tiny range of the lights,” he said.

“You need to be able to give it to them on a plate. It might be as basic as giving them an Excel file and saying, ‘We’ve got this data, you should be pricing it like this.'”

“You need to be able to give it to them on a plate. It might be as basic as giving them an Excel file and saying, ‘We’ve got this data, you should be pricing it like this.'”

James Rendell, BirdsEyeView

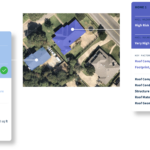

Referring to microwave sensors, in particular, he said, “We could, in theory, already with some of the products around, map buildings and know their heights, know almost exactly their shape.” And all of those can have direct impact on insurer pricing models.

With the advent of cloud storage and cloud computing, “we are really starting to exploit all these data sources,” Favaron said. But technological progress on the space tech side isn’t stopping. The resolution of these instruments continues to improve. At the same time, the amount of data grows. “This is why, in my opinion, you see more products that are akin to post-event type of analysis, because the study area[s] are still confined and are more manageable to process. For all these activities, there’s a cost associated as well.”

Favaron said he hopes to see more widespread use of satellite data at the country and continent level in the next few years, in conjunction with other data sources, such as urban planning or building ownership datasets—in order “to enrich these datasets to give us a near-true representation of what’s on the ground.”

“We are in an age where we can see or predict natural events. But still, [insurers] need to know on the ground who owns what, when that building was built, will it withstand a particular natural event,” he said, noting products filling in those blanks are emerging now.

Favaron sees the promise of satellite data insights reaching beyond the property insurance world. He notes that satellite information “can be used as proxy for human or animal activities”—informing environmental underwriters, for example, what type of pollutants are generated from a production plant. That might give a liability insurer an idea of the type of manufacturing taking place at the plant or how much storage they have, he said. AXA XL underwriters in lines beyond property have reached out after seeing applications and pricing tools created by Favaron’s group for the property lines, he reported.

Why Not Now?

“I don’t think the technical side is the main thing that needs to move forward,” said Schwarz, also suggesting that insurer innovation on product development, underwriting and pricing is the wave of the future that’s starting to take shape now. “I say this as a scientific-first company and a team of scientists primarily,” she said.

In the insurance world, Schwarz envisions the development of more robust business interruption insurance products from satellite data. “I feel pretty strongly that the widespread disruption from climate change that’s coming over the next years…is just going to disrupt economies really on all scales, to orders of magnitude potentially beyond what we’ve just seen in the last two years,” she said, referring to business interruption losses related to pandemic shutdowns.

“Suddenly, with high-quality, satellite-based analytics, you can see risks to distribution from a port to your gold mine in Ghana or your agricultural facilities across Nigeria that a significant portion of operations, and then supply chains, are relying on,” she said.

Offering an insurance product innovator’s perspective to the Roundtable panel, James Rendell, chief executive officer of London-based MGA BirdsEyeView Technologies Ltd., responded to questions from Fitzgerald about other factors holding the industry back from moving forward with parametric products that his firm and others are designing from space data.

BirdsEyeView takes the developments occurring in the Earth observation sector and deploys those into the insurance market by structuring new parametric insurance solutions for climate change risks, specifically targeting customers in the [small] and mid-market sectors, Rendell explained. (See related textbox, “What BirdsEyeView Offers”)

“We’re looking at Earth observation datasets the whole time, and there are some fantastic things you can do” with them, he said, noting that small satellites “can see a car on the road or an individual.” While that is valuable for claims and damage assessments and post-event recovery, “you can’t escape from the fact that you still need to do the [upfront] risk modeling. That’s fundamental to insurance.” Since that fantastic high-resolution live data never existed before, “that creates problems for the underwriter because it’s not baked into the pricing and risk modeling.”

In other words, in Rendell’s view, what insurers are uncomfortable with is a mismatch in the historical data going into risk and pricing models—basically, the blend of coarse resolution data for part of the historical experience period used in the models and very high-resolution data now available to use for settlement.

He gave the example of multi-spectral imagery captured by the Sentinel-2 satellite that had the ability to measure chlorophyll in plants (a metric that can be used to develop a vegetation index, assessing whether or not an area being observed contains live green vegetation). “But it’s only been capturing data since 2015. So, for risk modeling, you’ve maybe had a much coarser resolution from Landsat from 2000 to 2015,” he said.

With satellites monitoring rainfall amounts, a weather risk product for farmers, for example, pays out a predetermined amount triggered by certain amount of rain.

Event and contingency covers for global sporting events, mine closures and construction project stoppages, as well as for the hospital and retail sectors (responding to unseasonal rainfall or snow that reduces customer traffic), are similarly structured.

“All underwriters ever ask you—the first thing that they ever ask me is how much historical data have you got and how consistent it is,” Rendell reported. While parametric insurance developers can present correlations between the historical data and the live data to respond to the questions, “it just leads to twitchy feet and being uncomfortable,” he said. “That’s where the risk modeling needs to catch up.”

For parametric insurance development, “you’re extrapolating the probability of X event happening again in the future. And a lot of the underwriters we spoke to, even if we found high-resolution satellite data, if there wasn’t enough historical data available of the same dataset, they were unwilling to underwrite,” he said. For example, for a parametric rainfall-based product, they get worried that the new dataset is more sensitive than the historical dataset, he said. He added, however, that BirdsEyeView is now working with Lloyd’s syndicates that are more willing “as long as we prove to them from a data science perspective that it aligns with their pricing.”

Schwarz and Rendell agree that insurers are looking for satellite information providers to do some of the work of organizing data and to overlay insights on their exposure base information in ready-to-use formats.

“Our users on the ground, even the sophisticated ones within the insurance industry, don’t actually care about the millions of pixels we’re crunching all the time or the cool new algorithm that we just published on it,” Schwarz said. “They don’t even want the map. They don’t even really want the analytic or the insight. They want just the answer to their question, which is often just a CSV table [comma separated values file] of their assets and which ones are flooded today and not.”

Molding the information for insurers that don’t have resources to make sense of the data is a more important task for vendors operating in the geospatial space—from analytics companies to satellite operators—than adding information from a new spectral band, Rendell said. “The key to cracking this is [to remember] that not every underwriter or insurance company is like Swiss Re, which has a Research Institute and every bright young person coming out of a Swiss university.”

Related Videos

Related Videos

- Seeing Through Clouds: Satellites In Insurance (Full Roundtable, 52 minutes)

- Why Now Is the Time for Geospatial Technology in Insurance (Roundtable Excerpt, 7 minutes)

- Beyond the Human Eye (Roundtable Excerpt, 3 minutes)

- Planetary Scale vs. an Excel Spreadsheet: What Carriers Want From GIS Providers (Roundtable Excerpt, 9:30 minutes)

- On the Horizon: From Flood to Business Interruption (Roundtable Excerpt, 5 minutes)

- Keys to Insurer Success in GIS: Talent, Innovation Mindsets and More (Roundtable Excerpt, 8 minutes)

“You need to be able to give it to them on a plate,” he continued. “It might be as basic as giving them an Excel file and saying, ‘We’ve got this data; you should be pricing it like this,’ [or] ‘You use Sequel Rulebook], and we can integrate it into that.'” (Editor’s Note: Sequel Rulebook is a combination rules engine, underwriting desktop and analytics tool. Verisk acquired Rulebook, a provider of business intelligence and software solutions for the London Insurance Market, in 2018.)

Favaron said that insurers run the risk of being overwhelmed by improvements in satellite technology and applications. “In the next few years, we’ll be bombarded by new products coming into the market and all these satellite providers coming to us and saying my product is better than this other company because of this and that.”

“It is very important for the insurance industry to have the right capacity and know-how within the company, but not just within the company—[also] by working together with the academic world.”

“I see, probably in the future, the opportunity for a consortium of different types of industries—not just insurance—to [pull] together the economical backing that we need to harvest that data and to process that data together with the academic world and some other players. And I think countries, governments should also be behind these,” he said, noting that such initiatives already are taking shape.

Mythos Myths: Good Guys Hold More Cybersecurity Cards, Insurer CEO Says

Mythos Myths: Good Guys Hold More Cybersecurity Cards, Insurer CEO Says  The Skills People Still Perform Better Than AI

The Skills People Still Perform Better Than AI  California UPS Mechanic Admits to Workers Comp Fraud

California UPS Mechanic Admits to Workers Comp Fraud  More Than 1M People Alerted Before Northern California Quake

More Than 1M People Alerted Before Northern California Quake