In the first part of this four-part article, we revealed that Root—currently the fastest growing carrier of three VC-backed InsurTechs we’ve been tracking—also posted the worst loss ratio result of the trio in third-quarter 2018.

Executive Summary

With permission of the authors, Carrier Management is republishing this analysis of the statutory financials of InsurTech insurers Lemonade, Metromile and Root, originally published on LinkedIn. Originally published as a single article, we present it as a four-part series. This is Part 2.For the complete original article, visit the LinkedIn pages of Matteo Carbone or Adrian Jones.

Root’s 128 gross loss and loss adjustment expense ratio for third-quarter 2018 also marked the auto insurer’s worst quarter of the year.

What’s the problem for the InsurTech that we referred to as a “grasshopper” in Part 1?

At the November 30 plenary session of the U.S. IoT Insurance Observatory (founded by one of the co-authors), Denese Ross of DRC Consulting shared an in-depth 50-page review of Root’s filings, which total over 130,000 pages. Our opinions, based on her factual, non-opinion analysis, is that Root is experimenting aggressively, correcting some rookie mistakes, and is still underpricing some business.

The following is our interpretation:

• Raising rates, but is it enough? Root has begun correcting its early underpricing by raising rates substantially in several states, but not as much as the actuaries indicate is needed. The company has filed rate increases in seven of its 20 states since late summer, ranging from +5.5 percent to +34 percent. The highest is in Texas, where the filing is pending, and where Root now writes one-third of its premium (whereas Ohio was the largest state last year).

The indication in Texas was +200 percent. An indication is the change to the overall rate “indicated” by an actuarial analysis to achieve a specified pricing target based on analysis and adjustments to historic trends.

For many reasons, the rate level chosen could be less than the indication, but a big gap between rate taken and indication suggests management may still be oriented towards growth even if it is at a loss. Indeed, Root recently put up a blog post claiming to be up to 52 percent cheaper across states. Further, Root also added or changed discounts, which are not part of the headline rate.

In other states, per-policy rate caps limit the actual amount of rate taken on renewal business, possibly to avoid churning existing customers, since the acquisition cost of a renewal customer acquired via a direct channel is quite small.

These ratemaking decisions illustrate the fine line a company like Root has to walk when balancing growth, profitability, retention, and acquisition cost. Similarly, investors should be wary of individual numbers presented in isolation. It can be good to churn underpriced customers.

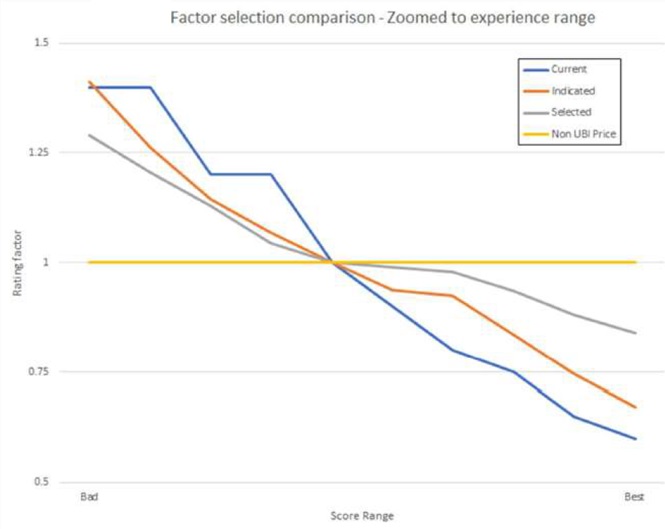

• Technology that isn’t as predictive as expected. Root collects telematic data via a smartphone and scores a driver once they have tracked 500 miles, using features such as hard braking, acceleration, turning, time of day, mileage, consistency, and distractions. The company started with a third party’s telematics model that apparently gave excessive discounts to drivers in better tiers. See the steep blue curve below, which is from a Root filing.

Root then developed its own model and is giving more modest discounts to better drivers (gray line).

Telematics contributes information and allows more granular clustering, but the law of large numbers and class rating variables (e.g. demographics) still matter more than perhaps anyone would like. Good drivers get hit by uninsured bad drivers. Bad drivers can drive well for 500 miles when they’re being watched. Good drivers’ cars get stuck in hail storms and hurricanes.

Nonetheless, Root is the first insurer around the world to acquire large numbers of customers through a TBYB (Try-Before-You-Buy) app, something many incumbents have tried in the past few years.

• Me-too is harder than it looks. Root has filed several modifications to its rates to correct mistakes, such as correcting household structure data, moving from ISO vehicle symbols to factors assigned directly by VIN, and correcting for “double-discounting” and “double-surcharging”.

• Claims difficulties. Most startups lack a high-quality claims infrastructure, which is one of the hardest aspects of an insurer to build, but it appears that Root is now taking more claims activity in-house instead of using a third-party claims administrator (TPA). To date, Root’s customer claims experience hasn’t been as easy as they say. Their 15 Better Business Bureau complaintsare mostly claims-related, and only one-third of Clearsurance userswere satisfied with the claims experience. On the same website, Progressive and GEICO are around 80 percent, and Metromile is at 70 percent claims satisfaction. As one Clearsurance review of Root reads: “I was in an accident back in July and it’s now November and my simple simple claim has not been paid on or closed out. It was originally with an adjuster at Crawford & Co. but without my knowledge that changed hands to some other adjuster actually within Root. The original adjuster back in September said that she would get back to me within the week….Months later and I’m still here with an open claim.”

It will take time for these corrections Root has made to show through in results. And particularly on pricing, they may be too little. Thus, the unanswered question remains: Is Root’s growth simply the result of selling something far too cheaply, or are they quietly experimenting their way to becoming the next Progressive?

Our thoughts are summarized in Part 3 of this article.

Related Articles

In Part 1, the authors present overall loss ratio, expense ratio and combined ratio results from statutory filings of the three insurers. “Between An Ant and A Grasshopper, Lemonade’s Results ‘Most Improved’ for Q32018”

In Part 3, they answer the question, “Can an InsurTech Startup Compete With Progressive and GEICO?“

In Part 4, they revisit a comparison of results for VC-backed startups and startups backed by traditional incumbent carriers. “Startups vs. Incumbents Revisited: Q32018“

Design the Team Before You Design the Solution: Commercial Trucking Case Study

Design the Team Before You Design the Solution: Commercial Trucking Case Study  Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Driver Death Rates High for Small Cars, Big Engines: IIHS

Driver Death Rates High for Small Cars, Big Engines: IIHS