In the realms of cause and effect, nothing quite stacks up to innovation for its ability to create positive change in any organization.

When insurers first heard that AM Best would be assessing innovation, some were skeptical. Insurers are all different. Unique products would call for different levels of innovation. How could innovation truly be measured in a way that makes sense and also doesn’t penalize those areas of the industry that don’t need dramatic innovation? Is there anything to truly be gained in the process, or is this just another way to assess the value of an organization? Is there any correlation between innovation and profitability? Is there any relationship between innovation and overall business strength? Operationally and strategically, where are insurers on the roads of innovation?

I asked two industry experts to join me in a webinar entitled, Insurance Transformation — Operationally and Strategically — Where are We?

Our goal was to look at innovation from at least two angles. First, we wanted to look at the practice of innovation and how it might play a role in furthering the goals of the organization. Instead of sticking with theory, we asked an AM Best expert to give us his innovation perspective using real AM Best findings from insurers who had reported on their innovation status. Second, we wanted to look at the strategy of innovation. How much of a priority do insurers need to give to innovation if they hope to improve their long-term profile for growth?

We split this interview into two sections. Today’s blog covers both the current status and theory of innovation efforts. The second will cover the practice of innovation from the perspective of different lines of business.

Our three experts on the September webinar panel were:

Edin Imsirovic, Associate Director, AM Best

Seth Rachlin, Executive VP, Global Insurance Industry Leader, Capgemini

And myself, Denise Garth, Chief Strategy Officer, Majesco

To kick us off, I asked Edin Imsirovic to walk us through the AM Best Innovation assessment. He answered many of our questions below.

What is the Innovation Score and how did it come to be a part of the “official criteria” of an AM Best rating?

Edin Imsirovic

Discussing company-specific innovation is really nothing new. We have always talked about companies’ innovative strategies and have analyzed their focus on innovation. It’s always been a part of our rating process. So why did AM Best try to separately assess innovation with a separate assessment?

The biggest reason is the accelerated nature of change. During times of rapid change, being innovative is especially important because business models may evolve or change more rapidly. Before we launched the innovation criteria, we did an industry survey and found that only 1% of the industry does not see innovation as critical. So, given the industry’s view of the importance of innovation in times of accelerated change, we decided to be proactive in addressing these trends by highlighting this particular aspect of insurance and making the analysis of innovation more explicit. It took us about two years of working with the industry and various academic institutions to develop the innovation score.

How does the Innovation Assessment operate within the Business Profile?

Edin Imsirovic

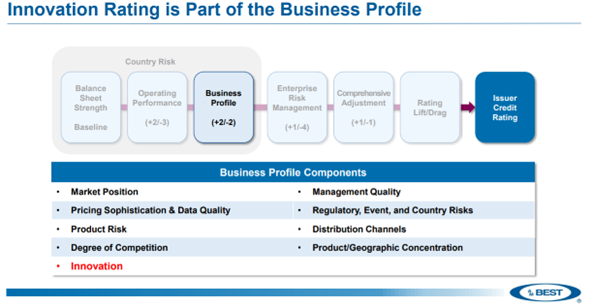

AM Best still has the same building block approach to the rating process. We start our analysis with policy strength, and then we look at forward-looking factors like operating performance, business profile, and enterprise risk management. Historically, the business profile has different components; things like market position, management, quality, and so on. (See Fig.1)

Figure 1: Innovation Rating

Innovation is now the ninth component. Our belief is that innovation or lack of innovation can either enhance or erode the financial strength of the insurer.

We take an input and output approach to measuring innovation, both of which are weighted equally. For input, we rate leadership, culture, and resources that are dedicated to innovation, as well as processes and structures related to innovation. When we look at the output, we look at the level of transformation related to innovation, tied to quantifiable results.

Has AM Best seen a correlation between innovation scores and AM Best ratings?

Edin Imsirovic

Yes. It became apparent that the most innovative players like those in the leader or prominent categories were able to differentiate themselves by credibly quantifying the results right at the output of their innovation efforts. The leaders distinguish themselves by being the innovative first movers within the insurance space. They were typically the timeliest in responding to market pressures by offering new products or solutions for emerging needs. Leaders typically had very high transformational scores.

As you would expect, the higher rated the company is, the higher the innovation scores.

Which lines of business seem to be the most innovative?

Edin Imsirovic

Every line of business has innovative players, but as we were conducting innovation assessments throughout our universe, we noticed certain themes related to innovation. For example, those with either the greatest competition or those with the most structural or technological change also tended to be the more innovative players. The most innovative lines of business we identified were reinsurance, health, and personal auto lines.

Personal lines, in general, are especially exposed to changing consumer tastes and preferences and higher consumer expectations. Consumers are drawn toward seamless and personalized user experiences. Insurers are increasingly facing expectations that are set by other industries rather than by direct competitors.

We also are seeing increasingly how insurance companies are turning to innovation to address quality, which is a prominent concern of health insurance. Health insurance is concerned with both the quality of customer service and the delivery of quality health care.

Let’s look at a high-level summary regarding business results. Is there any correlation between innovation scores and growth rates?

Edin Imsirovic

You can see a very interesting and clear delineation between innovation categories related to premium growth. Innovators grew their premium over a five-year period at approximately 12%. Moderates grew at 9%. Companies with minimal innovation grew at 8%.

We also noticed that innovation and supply and growth are linked. Digital advancements have enabled more innovative insurance to gain market share. The divergence in premium growth was particularly acute during COVID.

Insurers that already had digital infrastructures were generally able to continue more or less normal operations. For example, the average net premium rate and growth in 2020, which was the peak COVID year, was about 7% for innovators. Premium growth for moderate innovation was about 4%. Those with minimal innovation assessments were below 2%.

Those classified as leaders in innovation also tended to have lower expense ratios. They have made optimizing operating efficiency through innovation a crucial part of their strategy.

The Economy’s impact on innovation.

Should the industry pull back or move forward? What should business priorities be, in light of today’s macroeconomic factors?

Denise Garth

We have a number of macroeconomic challenges that all businesses, including insurance, are beginning to face. They will have an impact and an influence on innovation plans and budgets and priorities moving into 2023 and beyond. I would categorize them into eight areas.

- Optimize & Innovate Business — continue to optimize while creating innovation around either the existing or future business.

- Risk Resilience — focus on risk prevention and risk mitigation to avoid claims and improve customer experience.

- Customer Expectations — look at the expectations that are driving the business.

- Personalized Niche Products — match smarter customer spending by insuring and underwriting based on lifestyle/behavior/business need.

- Market Reach & Growth — allow customers to buy insurance differently, through additional channels and embedded options.

- Ecosystem and APIs — foster partnerships and distribution arrangements that depend on APIs which allow insurers to connect.

- Long-term Data Strategy — expand data sources for underwriting and claims, plus the application of AI and machine learning.

- Interconnected Tech Foundation — customize the technology set that can be brought together to meet your business strategy.

When Majesco looked at weighing growth and innovation, like AM Best scores, we found that Leaders by far outpaced Followers and Laggards in terms of five strategic areas. Are they replacing core insurance systems with next-gen cloud core, creating new products, launching new business models, expanding distribution channels, and reallocating resources from running the business as is to fit the new realities of business? We found the gap between Leaders and Followers was about 30% and the gap between Leaders and Laggards was about 70%. And the pace of change isn’t going to stop. The faster it continues, the wider the gap can become. Interestingly, these gaps line up with AM Best’s first full innovation assessment for P&C.

Given the macroeconomic shifts, do you see a change in investment priorities? What kinds of refocusing or shifts are you seeing?

Seth Rachlin

It is my perception that insurance companies typically don’t react quickly to changing macroeconomic conditions, but they do ultimately react. My fear is that the recession, if it is going to happen or has already begun, will ultimately hit technology budgets. I’m worried that there will be a retrenchment of what’s been a fairly buoyant tech spending environment within insurance and that it will ultimately slow down advancements that are already moving not as fast as they should.

From a priority perspective, the things you outlined are spot on. I don’t think we’ll see a shifting of priorities. There may be some heightening of efforts to take cost out because tough economic times usually bring with them a focus on cost. My fear is that the recession slows us all down from where we need to be.

Is Talent also an issue regarding innovation and focus?

Denise Garth

The U.S. Bureau of Labor Statistics has indicated that the insurance industry is halfway through a massive 15-year shift where 50% of the workforce is going to retire by 2028. That is only five years away. I was recently in a conversation with an insurer who stated that they are expecting 40% of their workforce to be eligible for retirement within the next three years. This wasn’t built into their plan! It gives us another perspective on priorities and the importance of next-gen technology replacing legacy, but also in how technology might optimize the business processes and redefine certain roles to provide a better customer experience.

Seth Rachlin

It’s possible that these retirement cliffs that we are talking about are impeding change, because it creates a level of risk aversion among executives within insurance. An executive might be looking at retirement, thinking, “I know how slowly the industry moves. I’m pretty comfortable not having to feel this [innovation] fire under me because I’ll make it another five or 10 years before things really have to change.”

And, I think that’s absolutely the wrong way of thinking. The industry has been at this a long time. We are not making the progress that we need to make. The fact that AM Best was only able to identify a few leaders, so far, is indicative of that lack of progress.

I was struck with a comparison between this and something that Jamie Dimon, the CEO of JPMorgan Chase, said at the end of last year when they released their investor statement. He said JPMorgan Chase is going to invest $12 billion a year in technology — 10% of their total revenue. This represented a 26% increase from the prior year.

When investors pushed him and asked, “How are you going to measure the return?” he said, “We’re in this game for the long haul, and we’re in this game to preserve the business and the position that we have. I’m not going to get hung up on measuring ROI quarterly.”

I’ve been around insurance tech a long time and I have never seen anything like a 26% budget increase. I wish that there were more people in the insurance industry who had that level of courage. I think that level of courage is what we need.

Denise Garth

This points to an opportunity for next-gen cloud technology investment — a potential advantage that mutual insurers might have over publicly traded insurers. Both are sitting on a lot of capital, because they must from a regulatory standpoint, but there is still a lot of money that’s available for investment. Instead of investing in the market, maybe these companies should invest in their own businesses.

In our next segment, we’ll discuss mutual insurers and their deployment of capital. We will look at how innovation is practically working itself out among all different lines of business, such as health, life, P&C, and among the different supporting players within MGAs and reinsurance. We will also connect the dots between the technology designed to help insurers prevent and protect and the innovations that are necessary within core systems.

For a preview, be sure to watch Insurance Transformation — Operationally and Strategically — Where are We?

By Denise Garth

AI Pushes Underwriting Beyond Risk Selection to Prevention

AI Pushes Underwriting Beyond Risk Selection to Prevention  Your Greatest Competitive Advantage Isn’t Technology—It’s Leaders

Your Greatest Competitive Advantage Isn’t Technology—It’s Leaders  Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent

Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent  Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak