Five years ago, almost no accident and health insurance claims at Ping An Insurance Group ran without humans. Today, nearly 60% are automated, with some settled in just 51 seconds.

The leap shows Ping An’s push into artificial intelligence, after a decade of investment worth billions of yuan. Now, senior executives are counting on it to transform the share price, too. They are leveraging AI to double the firm’s price-to-book ratio over the next few years, according to people familiar with the management’s thinking. Provided net assets remain unchanged, that would add about $174 billion to the market value of China’s largest non state-owned insurer.

Investors remain unconvinced. Ping An’s Hong Kong-listed shares still trade 38% below their peak, and their 9.59% drop this year is worse than the wider market slump. But executives at the Shenzhen-based firm, which has 250 million customers and about 20,000 engineers, think the time is ripe for its yearslong bet on AI to finally show up in its share price.

“The AI era successfully opened the window for reshaping services,” Chief Technology Officer Ray Wang said in an interview. “The returns on investment are tangible, highly visible, and unequivocally compelling.”

At the core of the plan is a gateway linking Ping An’s 500 services across banking, insurance and health care. Set to roll out in early April, it’s backed by AI agents that automate underwriting and claims while boosting cross‑selling.

Cost Cuts

Ping An’s AI bet is already showing up in lower costs. Its auto insurance expense ratio dropped by 1.7 percentage points over nine years. That translates into about 5 billion yuan ($724 billion) of underwriting profit growth for the segment in the same period.

In addition, Ping An’s systems have been trained to recognize dozens of Chinese dialects, allowing AI to process insurance claims with minimal human intervention. These bots can even make loan-repayment calls, adjusting their tone depending on whether a customer responds calmly or with aggression.

AI handled 70% of Ping An Bank Co.’s 500 billion yuan of loan recoveries in 2025.

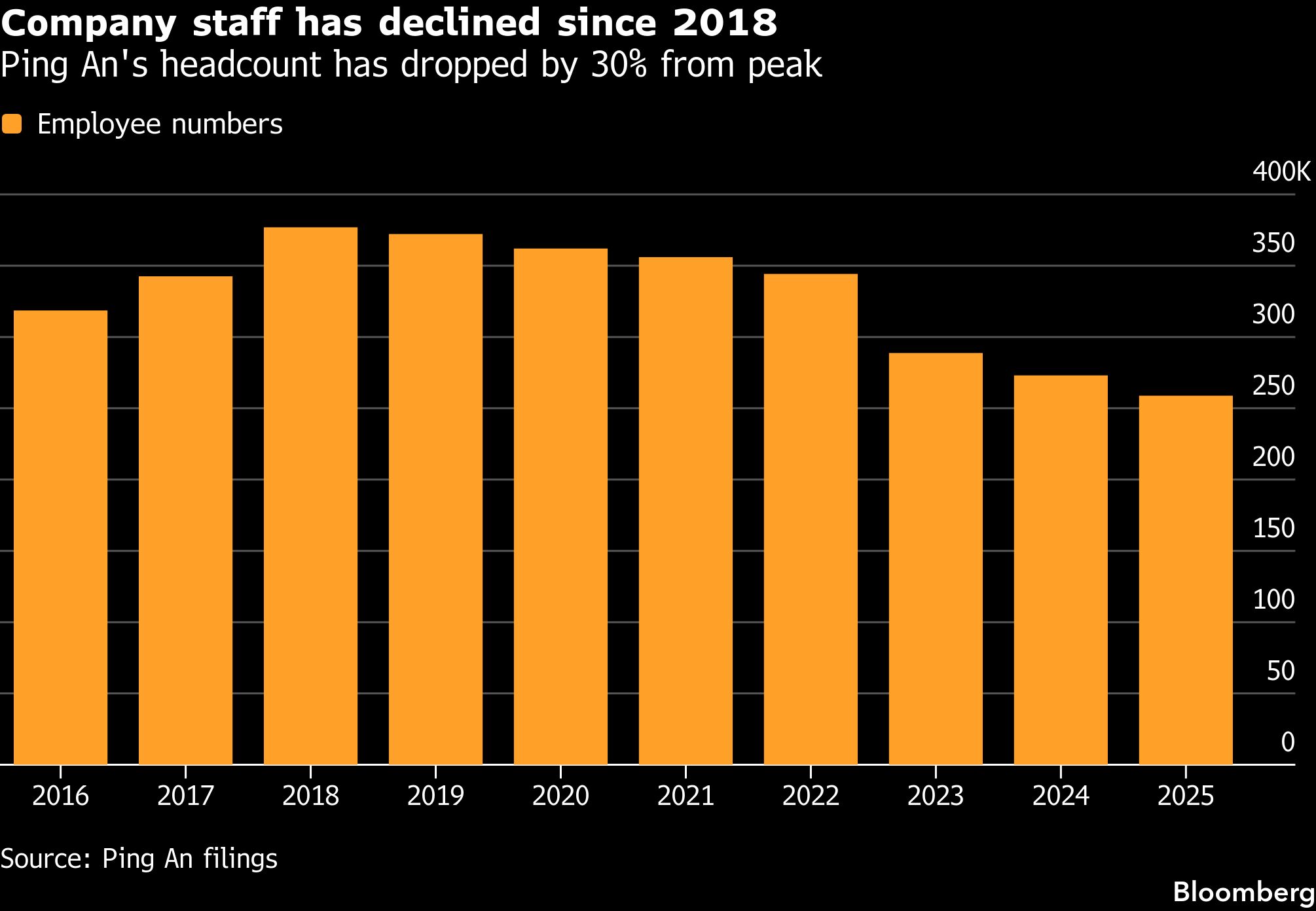

The firm has also more than halved call‑center headcount in the five years through 2025, as the chatbots replace people. Some employees were redeployed to other roles, the company said. Overall, Ping An’s workforce has fallen by more than 118,000, cutting headcount by about 30% from its peak in 2018.

These figures point to some of the worst fears around AI — and a few of the hopes. Discussions around the technology have a tendency to land on total doom or near-panacea as the eventual outcome. A report from the little-known Citrini Research in February fueled a widespread selloff as investors worried about mass layoffs. Bellwethers like Nvidia Corp. and Taiwan Semiconductor Manufacturing Co. have soared as others instead focus on the frenetic investment cycle.

The performance of Ping An — which was betting on AI long before it became the hottest trade in global markets — suggests the reality for many companies will be a little more complicated.

Few investors doubt Ping An has made serious changes to its business with AI. They just want more proof that it justifies a higher valuation.

“I think almost none of the investors are pricing AI into the stock,” said Nicholas Chui, a portfolio manager of Franklin Templeton’s $330 million Templeton China Fund, where Ping An is a top 10 holding. “If people want to buy AI, they’ll buy tech. You really wouldn’t, as your first choice, decide to buy Ping An.”

Historical Baggage

Part of the problem is that Ping An is still held back by historical baggage. Founded in 1988 by the tenacious entrepreneur Peter Ma, the company was the first Chinese financial firm to attract foreign strategic investors, including Morgan Stanley and Goldman Sachs Group Inc. It got a further boost when HSBC Holdings Plc became the largest shareholder.

Ping An’s profile rose as it diversified beyond insurance into banking, asset management, fintech and health care. But rapid growth also brought risks, leading to impairments on its investment in China Fortune Land Development Co. It also triggered payment delays at its trust unit and losses at its asset management arm.

Janus Henderson Group Plc’s Far East Income Fund sold its 2.2 million shares in 2024, due to concerns about the firms property exposure, said Sat Duhra, who runs the 532 million pound ($705 million) fund.

Ping An sells some of its tech know-how to other companies through its subsidiary OneConnect, but it remains a minor revenue contributor.

The company said it invests at least 2% of annual revenue on tech development. That translates into some 111 billion yuan of investments since 2021, based on data compiled by Bloomberg. CTO Wang said Ping An “has no concern” about evaluating return versus investment costs.

“Could this just be a cost-led initiative or can there be revenue drivers,” said Chui, the Templeton fund manager.

Growth Expectations

To convince the market, the company needs stronger growth. Ping An’s revenue is forecast to rise 9.5% in 2026, while a pure artificial intelligence company such as OpenAI has tripled sales.

Ping An said it’s not seeking to develop large language models like OpenAI, but rather build applications using those LLMs.

Michael Guo, co-chief executive officer, said that the one-stop platform will create upside. Retail clients own an average 2.94 Ping An contracts, up from 2.03 in 2015. Retail customer value has “massive room” for growth, Guo said in an interview. “It is quite normal for a single customer to continuously hold five, six, or even seven financial products.”

The firm has also tapped 30 years of proprietary voice and visual data to build services that cater to insurance claims. In one example, when a car accident happens at 3 a.m., an AI agent can respond at once, direct photo and video capture, and let the driver know they’re free to leave. The whole process takes a few simple interactions, Guo said.

Citic Securities Co. analysts led by Tong Chengdun see potential. If client experiences improve with the upcoming AI interface, the company could get clients to purchase higher-margin products, which could lead to “huge room for revaluation,” they said.

Photograph: Signage at the Ping An International Financial Center in Beijing, China, on Saturday, April 22, 2023; photo credit: Bloomberg

Deep Dive: Understanding Data Center Perils

Deep Dive: Understanding Data Center Perils  Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It  Red Sea War Insurance Costs Rise After Houthi Blockade

Red Sea War Insurance Costs Rise After Houthi Blockade  Global Commercial Insurance Rates Keep Falling; Down 8 Quarters in a Row

Global Commercial Insurance Rates Keep Falling; Down 8 Quarters in a Row