(Part 2 of 2)

Most insurance outsourcing contracts favor the provider, according to our firm’s analysis of the language in typical contracts in place today.

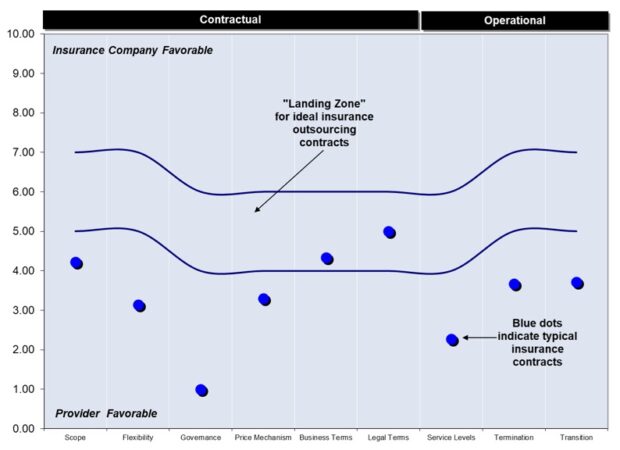

In our previous article, we graphically presented the results of our review of over 500 outsourcing contracts and how insurance outsourcing contracts tend to be significantly lagging in seven of nine key areas.

Scope: Provider responsibilities for the basic insurance processes are usually reasonably well documented, but contracts rarely document what happens when things go wrong, including communication, incident management and escalation rules.

Also, when the provider is responsible for the insurance platform, most contracts fail to document carrier information technology requirements for data feeds, testing, cyclical peaks, quality assurance, release management and demand management.

We rarely see well-designed provider requirements that would keep the platform current with such things as hardware and software refresh policies, automation requirements, RPA, and middleware support.

Post-COVID-19 digital transformations with AI, InsurTechs and the cloud have to be adequately addressed to give the insurance company control over provider-led automations and applications to ensure proper requirements for monitoring, testing, training and cybersecurity protocols exist.

Flexibility: Insurance contract terms tend to be longer than necessary, often seven to 10 years vs. a new market standard of three to five years. This is a problem when the contract contains cost-of-living inflationary adjustments that exceed market standards, lack reasonable productivity requirements or incentives, lack provisions for onboarding new work from new products and future acquisitions, or reduce costs when there is a decrease in volume from runoff or selling of old blocks.

The contract needs to allow the technology ecosystem to evolve over the life of the contract as innovation generates new products, new technologies, more InsurTechs and more advances in direct-to-consumer mobile apps, AI, drones, etc.

Governance: The governance provisions typically lack defined roles and responsibilities of the governance team or steering committee members and fail to include meeting schedules and agendas to manage the strategic and operational aspects of the contract.

Innovation provisions are rarely found in insurance contracts, so providers are not contractually obligated to introduce innovation. This gap in innovation and lack of controls for operational, financial, legal, regulatory and technology changes is especially troubling given the massive technology transformation that most insurance companies are going through in our post-COVID-19 world.

Pricing mechanisms: Old insurance contracts with FTE-based pricing are out of market with today’s best-in-class contracts, which have variable pricing tied to policy counts (all in price per policy) or have a fixed base price that changes incrementally over time as volume increases or decreases.

Insurance outsourcing providers often bring subrogation, underwriting and other tools that focus on increasing sales, reducing risks or increasing indemnity savings with some guaranteed performance improvements and savings and some gain-share for performance over and above the guaranteed amounts. These savings are often larger than the total of the provider’s outsourcing costs and are part of today’s new insurance outsourcing provider marketplace.

Another provision missing or underused in insurance contracts are errors and gain/loss provisions in which the provider takes responsibility for its errors that result in losses, late fees or regulatory fines above some reasonable baseline. Getting this right can save millions of dollars and prevent lawsuits.

Service levels: While timing-related service levels tend to be included, we rarely see quality or customer-satisfaction service levels, and at-risk amounts and allocation pool percentages too often are much lower than market standards. When we do see quality service levels, there is not enough detail to ensure that the quality score is a correct reflection that the work has been done accurately. A typical contract uses service-level percentages that are lower than what today’s world class providers are achieving with AI, RPA and other automation—and much higher than insurance trade association benchmarks. Other areas frequently lacking are root cause analysis, continuous improvement, and the ability to add, remove and change service levels over time as the business changes.

Termination: Often, termination fees are much higher than our best practice’s market standard and lack documented requirements related to termination assistance from the provider and maintaining of service levels during the termination period (which is typically much shorter than what is needed for a conversion and transition to a new provider).

Transition: Often we see a single, flat fee for transition and conversion, or at best a prorata fee each month during the transition/conversion period. Instead, there should be a detailed transition plan with clearly identified roles and responsibilities, and transition is only paid for when the provider has achieved significant milestones.

Our review of two other aspects of insurance outsourcing contracts—legal terms and business terms—finds them in line with market standards for most carriers.

However, today’s digital initiatives bring new complexities. As providers’ help insurance companies digitize their data and perform data analytics, there need to be contract requirements that protect policyholder data and limit the provider’s ability to use non-scrubbed and normalized data in provider datasets used for their own clients.

Disaster recovery and business continuity planning (BCP) requirements also need to be updated to address heightened cybersecurity needs with regular BCP tests, audit rights on testing and requirements to implement actions based on test findings. COVID-19 has shown that not being prepared for business continuity can result in not being able to stay in business.

Limitation of liability clauses provide a “cap” on provider liability; however, these clauses should also be updated to include a second level of the cap, a “super cap” (or increase the super cap if it existed) to cover the potential for breaches as insurance companies have been one of the primary targets of ransomware attacks. Also, pandemic-related language related to work-from-home, supplier site definitions and force majeure needs to be reviewed and likely rewritten to add allowances and requirements for work-from-home and exclude COVID-19 as a force majeure event. Key personnel requirements should also be tightened with succession planning to reduce the risk of loss of knowledge and skills when there is attrition.

Older contracts are rarely in line with contemporary, post-COVID-19 market terms and conditions. Insurance companies that renew them without a detailed contract benchmarking review as they enter renegotiations put themselves at significant risk.

The Need to Benchmark Your Insurance Outsourcing Contracts

Insurance companies with existing outsourcing contracts are likely overpaying, are not getting the level of service they could be getting and are taking on more risk than required. Much has changed about the insurance outsourcing market over the last decade and especially since COVID-19, including the mix of insurance providers and old contracting methodology with the smaller, FTE-based deals being replaced by new, larger, digitally oriented transformation deals with guaranteed savings that adjust as volume changes.

A benchmark of your existing contract before you renew or recompete with new providers can deliver current market terms, significantly better pricing and a service offering that takes advantage of the advances in digital technology.

Benchmarks can be extremely valuable if performed in a sophisticated manner, incorporating data on insurance outsourcing terms and conditions as well as the cost of today’s digital technology. Simply benchmarking the FTE price or price of the technology will miss potentially massive (frequently eight-figure) costs associated with missing or deliberately obscure contractual and compliance terms.

More Insurance M&A Deals on the Horizon?

More Insurance M&A Deals on the Horizon?  How Insurance Can Turn Maintenance Into Measurable Competitive Advantage

How Insurance Can Turn Maintenance Into Measurable Competitive Advantage  Senator’s Probe Reveals Lack of Transparency in Remote Assistance Use in Self-Driving Cars

Senator’s Probe Reveals Lack of Transparency in Remote Assistance Use in Self-Driving Cars  Insurers Using Advanced Analytics and AI See Strong Returns: Report

Insurers Using Advanced Analytics and AI See Strong Returns: Report