Two firms tracking mergers and acquisitions in the insurance industry reported changes in property/casualty insurance deals last year, with one describing “increased momentum” and another “stabilization.”

Both, however, indicated that selectivity and strategic approaches characterized 2025 deals—a dynamic they believe is likely to continue in 2026.

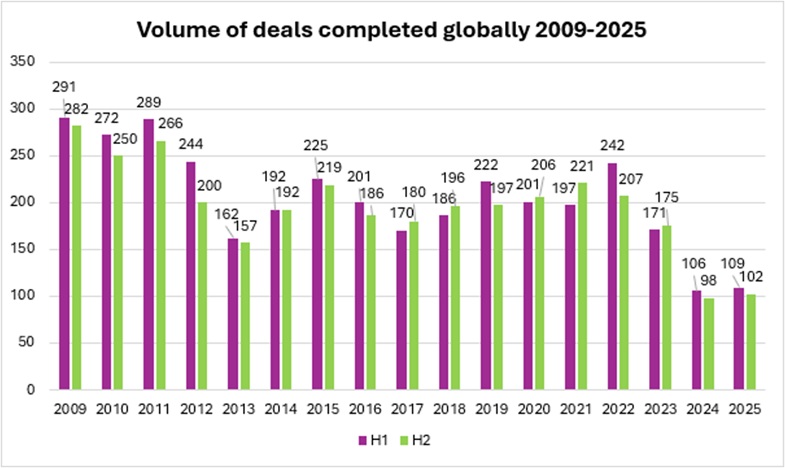

• Falling interest rates and a “more strategic approach” to acquisitions drove a stabilization of M&A activity during 2025, according to Clyde & Co’s annual “Insurance Growth Update,” which tallied 211 carrier and broker deals globally in 2025, up from just over 200 in 2024.

The 2024 figure marked a steep decline—more than 40%—from 346 deals in 2023, and 2025 activity levels remained much lower than those recorded for the 10 prior years, report statistics based on London Stock Exchange Group data reveal.

• Focusing solely on activity in the U.S. and Bermuda, Deloitte’s “2026 Insurance M&A Outlook: Eye on the Ball,” counted a lot more 2025 deals—455—including 411 broker deals, 26 P/C carrier deals and 11 in the life and annuity insurance segment. But only the life segment saw growth in deal volume, according to Deloitte, while the broker and P/C carrier segments had double-digit percentage drops in 2025 deal counts compared to 2024.

Still, despite a 19% drop in P/C carrier deal volume, the aggregate dollar value of P/C carrier deals rose 64%, “reflecting a pronounced shift toward larger, more strategic acquisitions,” the Deloitte report says, adding that five transactions exceeded $500 million each, compared with just one such transaction in 2024.

Despite differences in their tallies, the writers of both reports noted that strategic considerations marked P/C insurance carrier deals last year, and predict similar drivers in the year ahead. Deloitte, however, flagged a changing P/C insurance market as a fact that could fuel defensive combinations instead.

“One wildcard for 2026 is whether softer P/C market conditions and rising operational demands collide more quickly than expected,” the Deloitte insurance leaders wrote. “If margin pressure coincides with higher expectations around governance, data, and capital management, some insurers may increasingly view consolidation as a practical response.”

“In that environment, M&A could be driven as much by the need for resilience and scale as by growth ambitions,” the report says, adding that those who move early may reap the benefits of more choice and greater flexibility.

The Clyde & Co report highlighted opportunities to diversify and add new capabilities or to deepen expertise in specialty market segments as some of the strategic considerations that prompted 2025 deals.

“We saw this begin in 2024 with Zurich Insurance Group’s acquisition of AIG’s travel business, which represented a move to cement its global position in business travel insurance,” the firm said in a media statement.

“This trend in strategic moves to strengthen specializations ramped up in 2025 and will continue to shape dealmaking in 2026.”

One wildcard mentioned by Clyde & Co (although not specifically labeled as such) is geopolitical instability. Flagged as “a risk to the trajectory of dealmaking,” Clyde & Co said that not only could geopolitical instability disrupt sector confidence but also that the prospect of rising interest rates could increase the cost of capital and dampen deal appetite.

Region by Region

Behind a global stabilization in 2025, Clyde & Co like Deloitte reported a double-digit decline in deals in the Americas. By the Clyde & Co count, deals in the Americas dropped to 77 deals in 2025 from 92 in 2024 and 162 in 2023.

The United States continues to be a strong influence on global deal activity, with many multinational transactions driven by U.S.-headquartered firms, according to the international law firm, which said that 52 of the 77 Americas deals took place in the United States in 2025, with eight valued over $1 billion.

“U.S.-based managing general agents (MGAs) and carriers are increasingly looking outward for expansion,” Clyde & Co said.

While the Americas still has the highest level of deals compared to other regions, the APAC region had the strongest dealmaking surge in 2025, with 59 transactions last year compared to 39 in 2024. The APAC region also had the most mega-deals valued at over $5 billion—four of them—according to the report, which noted that two of those took place in Japan.

Clyde & Co reported a flat level of deals in Europe—57 in 2025, compared to 56 in 2024—and highlighted renewed interest in accessing the Lloyd’s platform, with some companies now considering re-entering Lloyd’s after previously drawing back from the market.

“Japanese insurers have been active acquirers and, following domestic portfolio adjustments, have significant capital available for overseas expansion,” Clyde & Co said, adding that the international law firm expects strategic, cross-border acquisitions by Japanese insurers to continue in 2026.

‘Strategic Collaboration.’ The Readiness Is All

The lawyers at Clyde & Co and insurance team leaders at Deloitte delivered their separate reports this month after Zurich and Beazley announced that they had agreed to a $10 billion-plus deal.

But the two reports were inked before Tokio Marine Holdings Group announced that Berkshire Hathaway’s National Indemnity Company would make a $1.8 billion investment in the Japan-based global insurer, and also that the two companies would embark on a “strategic collaboration in M&A and global investment opportunities.”

Describing the M&A collaboration, the Tokio Marine statement says, “The two companies will collaborate on global strategic investment opportunities, including M&A, executing joint investments to drive sustained business expansion…Through the Strategic Partnership, by combining our proven M&A execution capabilities with NICO’s peerless capital strength, we believe we are able to broaden our strategic options and access to high-quality growth opportunities,” the statement said.

Tokio Marine made note of the fact that it has “steadily expanded [its] global footprint through disciplined acquisition principles” in recent years. Last year, a Tokio Marine executive discussed the possibility of spending $10 billion on acquisitions, according to a Bloomberg report.

Whether the new collaboration with Berkshire will have any impact on the P/C insurance deal environment remains unclear. But Clyde & Co sees dealmaking continuing in 2026 for other reasons.

“We’re seeing a steady return to strategic dealmaking across the sector, driven less by any single transaction and more by market fundamentals,” Clyde & Co Partner Eva-Maria Barbosa said in an emailed statement to Carrier Management.

“Well‑capitalized carriers are reassessing portfolios, targeting specialist capabilities, and looking for ways to sharpen their competitive edge.”

Deloitte did not express a view on the impact of the Tokio Marine announcement before this article posted. In the report, however, Deloitte industry leaders wrote that “optionality favors the prepared.”

“As insurers look ahead to 2026, preparation may matter as much as appetite. Clarifying strategic priorities, understanding capital flexibility, and identifying opportunities early can help firms move with intent,” the report says, also pointing to the importance of “operational readiness”—everything from integration planning to governance alignment.

“This way, organizations can act decisively when opportunities arise, rather than reacting once competitive pressure builds,” the report says.

Strategies Behind the Numbers

Clyde & Co notes that recent deal activity “has been driven by portfolio optimization and geographic refocusing, as carriers have shifted their focus from a ‘growth at all costs’ mindset to evaluating strategic fits.”

“This has highlighted a clear divergence in the market, with steady and selective carrier activity sitting alongside strong, continued momentum among intermediaries, brokers and MGA platforms,” the global law firm said in a media statement.

Barbosa described the contrast as a “tale of two cities.” While 2025 activity has been “selective and steady” on the carrier side, in the intermediary space, “particularly with MGAs and brokers, we’re seeing continued momentum and a real depth of interest in the sector.”

“Insurers have sharpened their focus on specialty lines resulting in a clear emergence of strategic opportunities across energy transition-related risks, cyber and AI exposures, and contingency business tied to large multinational events,” she said.

“We expect this to continue into 2026 resulting in steady deal flow and targets thoughtful M&A.”

Like Clyde & Co, Deloitte sees more deliberate, targeted deals on the horizon.

“After a period of uneven and often cautious deal activity, insurance mergers and acquisitions signaled renewed momentum in 2025. While large, headline transactions remained the exception rather than the rule, deal discussions picked up across several segments, particularly in the back half of the year,” the Deloitte report begins.

The 2026 insurance M&A outlook “feels more balanced than exuberant,” the report says.

“Insurers have sharpened their focus on specialty lines resulting in a clear emergence of strategic opportunities across energy transition-related risks, cyber and AI exposures, and contingency business tied to large multinational events.”

Eva-Maria Barbosa, Clyde & Co

While many insurers enter the year with “stronger balance sheets and more room to maneuver,” they also have “a more measured view of risk, growth and integration,” Deloitte insurance leaders believe.

“Instead of a broad-based resurgence in dealmaking, M&A activity may consist of targeted moves, evolving deal structures, and a sharper focus on capital efficiency and long-term value,” the report says.

Overall, the report authors say they expect “selective insurance M&A strategies” in 2026 to be shaped by a focus on profitable growth. Referring to carriers’ portfolio rebalancing activities and capital discipline over the last several years, “some organizations could have more room to redeploy capital,” the report says, noting, however, that a softening P/C market makes organic growth harder to come by. “In that environment, M&A may regain appeal as a way to reposition portfolios, fill specific capability gaps, or sharpen strategic focus,” the authors conclude, adding that targeted, asset-light transactions are more likely than transformational deals.

The report describes two opposing deal drivers—some insurers still looking to shed businesses that consume too much capital vs. better-capitalized ones that can pursue renewal rights acquisitions, block acquisitions, specialty platforms, or carve-outs.

Related article: Everest Sells Another Retail Commercial Insurance Op: Canada Biz Going to Wawanesa

Among other expectations specific to P/C insurance, Deloitte said:

- Private capital is expected to stay active but focused on specialty P/C insurance, excess and surplus lines, and MGAs.

- Insurance brokerage M&A will emphasize operational integration, simplification, and targeted tuck-in acquisitions aimed at deepening industry or regional capabilities as organic growth opportunities moderate.

- Technology M&A will no longer focus on broad digital transformation but instead on AI and analytics capabilities designed to enhance the quality of underwriting, pricing, and claims management.

“The insurance M&A environment appears to be gradually reopening, shaped less by urgency and more by choice,” the Deloitte report concludes.

New Research Finds That Despite Improved Productivity, AI ROI Fails to Outpace Spend

New Research Finds That Despite Improved Productivity, AI ROI Fails to Outpace Spend  Deja Vu as Berkley Calls Out MGUs During Quarterly Call

Deja Vu as Berkley Calls Out MGUs During Quarterly Call  Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak  Mapfre to Acquire Safety Insurance in $1.5B in Cash Deal

Mapfre to Acquire Safety Insurance in $1.5B in Cash Deal