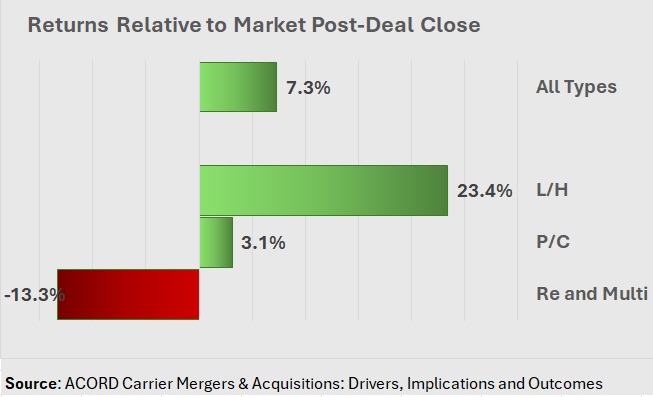

A recently released analysis of insurance carrier and reinsurer mergers and acquisitions finds that 75% of recent deals featuring reinsurers and multiline insurers as buyers destroyed value for shareholders.

The report, “Carrier Mergers & Acquisitions: Drivers, Implications & Outcomes,” published by the insurance industry standards-setting body ACORD, notes that publicly traded reinsurer and multiline (writing both property/casualty and life/health insurance) buyers in M&A deals stand apart from P/C and L/H carriers, who are largely value creators. In contrast to the reinsurer/multiline segment, 60% of P/C-only carriers created value through M&A deals they closed between July 2023 and December 2025, and 70% of L/H carriers did so as well.

ACORD used total shareholder return (TSR) indexed against the MSCI World Index as a measure of deal performance. (According to a report footnote, TSR was calculated using dividend-adjusted share price performance from the transaction closing date through Dec. 31, 2025, and indexed against the MSCI World Index to isolate deal-specific outcomes from broader equity market movements.)

Related article: Nearly Half of 100 Largest P/C Insurers Destroy Value: ACORD

As a group, reinsurers and multiline carriers produced 13.3% lower returns than the market between close date and year-end 2025, while post-deal returns for P/C insurers were 3.1% above the overall equity market.

L/H insurers saw the biggest return boost from deals with returns 23.4% higher than the market, on average, after deals closed.

The report does not identify carriers and reinsurers involved in deals analyzed but notes that the value part of the study involved 34 companies across all three sectors overall. Between July 2023 and December 2025, ACORD counted roughly 500 carrier deals across 84 countries. Of those, 34 met three more criteria for the value study—they involved non-affiliated companies, a publicly traded insurer as a buyer and deal values were disclosed.

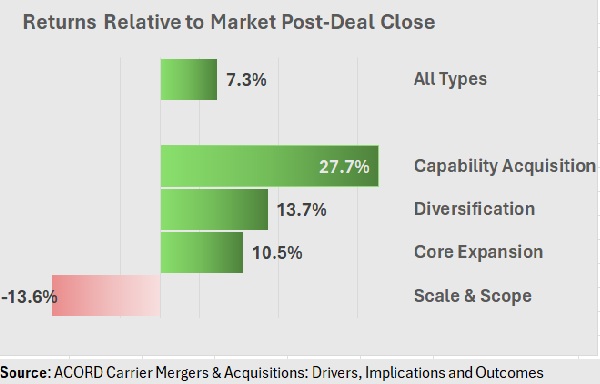

Scale-Seeker Deals Destroy Value

For the 34 carrier deals analyzed, the report also reveals differences in shareholder value for four different deal drivers, finding that deals done with the goal of achieving scale were also notable value destroyers, on average.

Key findings by deal driver are summarized below:

- Scale & Scope—amortizing fixed costs and improving resource access by increasing absolute size or expanding scope across strategic and tactical dimensions—was the only motivation associated with a negative indexed total shareholder return, averaging -13.6%. This deal driver ranked as the third-most cited buyer rationale for recent deals, sinking from first place in the prior decade.

- Diversification—expanding by acquiring new revenue and earning sources—has pivoted from the least-used, lowest-return rationale to a leading source of activity, with materially stronger outcomes. It has become the most prevalent motivation at 41% of deals, associated with the second-strongest returns (+13.7%), reflecting a notable shift in both adoption and performance.

- Capability Acquisitions—aimed at optimizing the risk, cost and time associated with developing new or enhanced internal capabilities—only accounted for 6% of recent deals. But the few capability-led deals produced the strongest returns (+27.7%).

“The underperformance of Scale & Scope as a buyer motivation highlights the difficulties of achieving scale-related benefits through M&A,” said Dave Sterner, Senior Vice President of Research & Development at ACORD, in a media statement. “Increasing scale only amplifies what already exists, including inherent limitations and challenges; it rarely transforms,” he said.

“Beyond a certain size, bureaucratic drag, slower decision-making and reduced innovation velocity combine to depress organic growth and weaken execution discipline,” the ACORD M&A report says, explaining the challenges of “Scale & Scope” deals.

“Scale benefits are often overestimated, while cost synergies are smaller than projected. Integration risks are also systemically underpriced, and diseconomies of scale are overlooked,” Sterner added.

He also reported, however, that for value-destroying deals, the primary driver of destruction was “execution, not deal logic.”

“Without disciplined value-capture management, synergies identified in diligence often dissipate during integration.”

Deal Sizes Soar

The report begins with an overview of insurance M&A over the past decade, encompassing both carrier and broker deals, revealing that while carrier deals accounted for on 21% of 13,000 transactions reviewed, in terms of dollars, those carrier deals represented 77% of the total deal values recorded. The average P/C deal size was $375 million over the 10-year time frame (2015-2025), and reinsurance and multiline deals averaged $623 million.

Since peaking in 2016 at 321 carrier transactions, the number of carrier deals (across all three segments, including L/H) fell to 163 in 2025, based on ACORD’s tally. Factors explaining the drop include “a challenging deal environment marked by higher costs of capital driven by rising interest rates, persistent inflationary pressures, geopolitical uncertainty, and increasing regulatory scrutiny and complexity,” ACORD said in a media statement.

Noting a shift toward fewer, larger transactions, ACORD noted that from 2015-2024, average carrier disclosed deal sizes were approximately $455 million, (including L/H insurer deals). In 2025, the average carrier disclosed deal size vaulted to $1.1 billion, ACORD said.

“As insurance M&A continues to evolve toward fewer, larger, and more complex deals, disciplined execution will remain the defining differentiator between transactions that close and those that deliver lasting results,” Sterner said. “Organizations that protect core operations, translate deal intent into focused value initiatives, establish clear decision rights, and sequence integration deliberately are far better positioned to sustain value creation.”

The report includes an extensive list of potential impediments to value creation (including problems with culture and change management, systems integration, talent retention and integration fatigue, among others), and a separate list of enablers of value creation (concrete executable synergy and growth initiatives, clear integration governance and value realization tracking, and others).

Summarizing the first list, ACORD said barriers to value creation in the deals studied for the report were mainly characterized by lack of focus or thoughtful assessment of the deals. One page of the report reviews the role of data standards on post-merger integration—reducing M&A execution risk “by providing a common industry-specific language across products, policies, claims, billing, finance and reinsurance.”

“ACORD Standards remain highly valuable even in smaller deals, where integration costs do not scale linearly and a one-time data ‘translation’ can represent a disproportionate share of total transaction value.”

For the first time, ACORD has made the study findings publicly available for both ACORD members and non-members. For more information or to download the report, please visit www.acord.org/research.

Featured image: AI-generated (ChatGPT)

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Deepest Drilling Study Ever Provides Insight into Deadly Japan 2011 Tsunami

Deepest Drilling Study Ever Provides Insight into Deadly Japan 2011 Tsunami  Beyond the Weather News Bulletins: How Insurers Can Improve NatCat Responses

Beyond the Weather News Bulletins: How Insurers Can Improve NatCat Responses  Default Speed Limit in Iowa Changes from 55 to 60MPH

Default Speed Limit in Iowa Changes from 55 to 60MPH