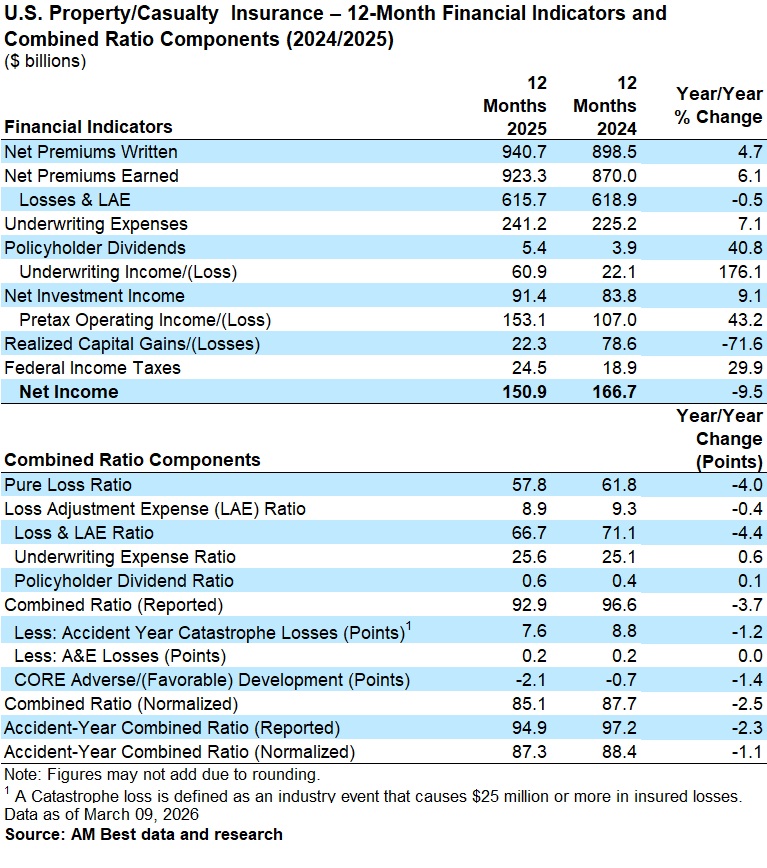

Building off momentum from the previous year, the U.S. property/casualty (P/C) industry recorded a $61 billion underwriting gain in 2025—nearly triple the $22 billion recorded in 2024.

With nearly all P/C companies’ 2025 annual statutory statements received, representing an estimated 96% of total industry net premiums written, AM Best can for the first time get a good look at how the industry performed for the full year in 2025.

The sharp jump in underwriting income even eclipsed AM Best’s earlier initial projections, based on third-quarter data. Still, what the numbers show ultimately do not come as a surprise given the positive swings in results AM Best started to see toward the end of 2023 and in 2024. The two largest personal lines of business—homeowners and private passenger auto, which make up nearly half of the P/C market—exhibited a tremendous improvement in underwriting profitability the last two years; for example, personal auto posted a $14 billion net underwriting profit in 2024 following a $17 billion loss in 2023 and a $33 billion loss in 2022. Though not as dramatic as personal auto, the homeowners line has also shown significant strides toward profitability.

While underwriting profit figures by line are not yet available for 2025, the two lines were likely strong contributors to the $61 billion total across all lines. The latest results are a manifestation of sustained disciplined underwriting and persistent pursuit of greater premium adequacy, and adherence to enterprise risk management principles in response to the difficult years that kicked off this five-year period.

There’s no doubt that the benign Atlantic hurricane season aided 2025 results as well, even as the year started with the California wildfires and other insured losses driven by secondary perils. The industry’s combined ratio for the year fell by nearly four percentage points to 92.6, with catastrophe losses accounting for 7.6 points, as compared with 8.8 points in 2024.

From the standpoint of rates and pricing, there has been a concerted push toward achieving premium adequacy in recent years, and companies have been more steadfast in sticking to their risk appetites while judiciously using the pricing tools available to them. This led to a 6% increase in net premiums earned for the year.

Key trends also include a softening reinsurance market after several years of significant cost increases and higher retentions. Loss‑free layers are likely to see modest price declines.

Predictive analytics and telematics are increasingly part of industry pricing models, particularly in the small commercial and personal auto markets, and insurers have accelerated investments in data, analytics and artificial intelligence (AI) to enhance underwriting precision, improve risk selection and streamline distribution. Technology is quickly becoming a critical competitive differentiator in pricing, claims and fraud detection.

Conversely, a lessening benefit from favorable prior-year loss reserve development has caused some profit margin constriction for the workers compensation line, which has long been the most profitable and consistent P/C line of business. However, the overall positive industry trends were enough to offset this headwind and others related to rising claims severity and macroeconomic volatility.

On the investment side, a nearly 10% rise in investment income in 2025 reflected favorable equity market conditions. It also highlighted how companies have been able to take the proceeds from maturing investments and reinvest them in higher-yielding instruments. The enhanced investment earnings combined with the higher underwriting profits created pre-tax operating earnings of $153.1 billion, 43% higher over the previous year.

From a policyholder’s surplus standpoint, the better investment environment helped to generate realized capital gains, which along with the improved underwriting margins, helped to boost overall industry surplus by 11.4% from the end of 2024 to $1.2 trillion at the start of 2025.

Whether property/casualty insurers can keep this momentum in 2026 bears watching. AM Best expects rate momentum, particularly for the commercial property, private passenger auto and homeowners lines of coverage, to moderate with the potential for profit margins to shrink, albeit remaining positive.

With some established reserve cushions dissipating, combined ratios could rise in other lines of business too, such as medical professional liability, which remained unprofitable in recent years. Even in the industry’s most profitable line, workers compensation, the consistent downward trend of workers compensation rates across many jurisdictions and risk classes has contributed to the tighter profit margins for that line as well—and eroding reserve prior-year reserve redundancies could compress margins further.

Already in 2026, P/C insurers were dealt a one-two punch of winter storms Fern and Hernando. At the same time, social inflation and third-party litigation funding are primary contributors to the rising claim severity that is negatively impacting insurers underwriting commercial auto liability and general liability, including umbrella and excess liability coverages. Nuclear verdicts, which have subsequently led to higher average liability settlements, continue to exhaust primary layers and pressure umbrella and excess carriers.

Despite an expected reprieve with the Supreme Court’s ruling on tariffs, global macroeconomic factors, particularly with the Middle East conflict intensifying, could impact results. Companies with tighter control over supply chains are better positioned to manage these pressures.

Even if the property/casualty industry takes a small step backward, most carriers operating within the segment are wielding fundamental positives that AM Best believes will continue throughout 2026 and create another year of positive underwriting results.

Farmers Making It Easier for Consumers to Understand Insurance

Farmers Making It Easier for Consumers to Understand Insurance  Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent

Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent  Deep Dive: Understanding Data Center Perils

Deep Dive: Understanding Data Center Perils  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age