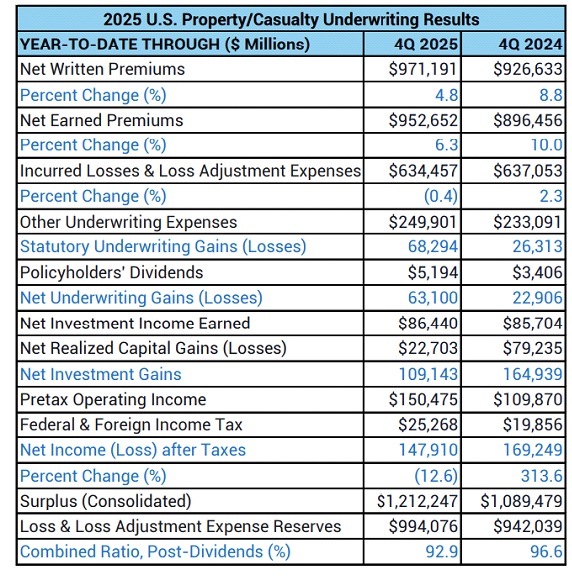

In a joint report of U.S. property/casualty insurance industry financial results yesterday, Verisk and the American Property Casualty Insurance Association revealed the same eye-popping level of underwriting profit improvement that AM Best did earlier in the week: 176%.

While the dollar figures tallied by Verisk and APCIA don’t exactly match those presented by rating agency AM Best, both reports agree that industrywide pretax underwriting profit soared past $60 billion—almost three-times the $20 billion-plus level recorded in 2024.

The surge translated to 3.7 points of improvement in the combined ratio, which landed at 92.9 for 2025, according to both reports.

Related article: P/C Industry Soared in 2025. Will It Fly as High in 2026?

Much of the downward movement in the combined ratio was attributable to lower loss and loss adjustment expense ratios, which came in roughly 4.5 points better in 2025, with the dollar value of losses falling slightly while earned premiums jumped more than 6%.

“Industry results continued to stabilize in 2025. Incurred losses were largely flat, reflecting the unusual lack of hurricanes making landfall in the United States,” said Robert Gordon, senior vice president, policy, research and international at APCIA.

Other underwriting expense dollars, however, climbed more than 7%, according to both reports, moving the industrywide expense ratio up by about 0.6 points.

Providing some underlying detail on the loss ratio component of the combined ratio, the AM Best report showed that less catastrophe losses and more favorable loss reserve development in 2025 explained more than half of the loss ratio improvement. Catastrophe losses accounted for 7.6 points of loss ratio in 2025, as compared with 8.8 points in 2024—a 1.2-point improvement. Prior-year development shaved 2.1 points off the 2025 loss ratio by AM Best’s calculations, compared to 0.7 points in 2024—a 1.4-point improvement.

“The industry delivered one of its strongest underwriting results in years in 2025, supported by a near-record low combined ratio, but that outcome was driven more by unusually low catastrophe losses rather than a fundamental shift in industry risk,” said Saurabh Khemka, president of Verisk Underwriting Solutions, in a media statement about the Verisk/APCIA report. “A near 90 percent decline in hurricane-related claims in 2025 materially reduced catastrophe losses, an improvement that reflects limited U.S. landfall rather than a change in underlying exposure,” Khemka said.

“The industry delivered one of its strongest underwriting results in years in 2025, supported by a near-record low combined ratio, but that outcome was driven more by unusually low catastrophe losses rather than a fundamental shift in industry risk.”

Saurabh Khemka, Verisk Underwriting Solutions,

Khemka, like David Blades, associate director of Industry Research and Analytics for AM Best, highlighted the positive impacts of personal auto underwriting improvements, fueled by strong rate action and tighter underwriting discipline, also noting that workers compensation continued to deliver consistently favorable results last year.

“At the same time, overall premium growth decelerated and commercial liability continued to weigh on overall performance.”

“Taken together, these dynamics make 2025 a reset after several years of volatility, not a new normal,” Khemka said, stressing that ongoing catastrophe variability, moderating rate momentum and elevated legal system costs are factors pressuring industry results in 2026.

“That reality is already playing out this year, as recent tornado and hail events serve as an early reminder of the volatility that continues to define catastrophe risk,” Khemka said.

Verisk and APCIA also pointed out that escalating material and labor costs continue to drive higher repair and replacement expenses, particularly for roofs, and that frequent and intense hail and severe convective storms are expanding property loss exposure beyond traditional geographies.

Verisk and APCIA also pointed out that escalating material and labor costs continue to drive higher repair and replacement expenses, particularly for roofs, and that frequent and intense hail and severe convective storms are expanding property loss exposure beyond traditional geographies.

“As a result, recent profitability should be viewed against a backdrop of persistent and evolving risk as the industry moves through 2026 and beyond,” the joint statement said.

Blades had a seemingly more optimistic assessment.

“The latest [2025] results are a manifestation of sustained disciplined underwriting and persistent pursuit of greater premium adequacy, and adherence to enterprise risk management principles,” he wrote in an article for Carrier Management summarizing AM Best’s initial tally of last year’s results.

“Even if the property/casualty industry takes a small step backward, most carriers operating within the segment are wielding fundamental positives that AM Best believes will continue throughout 2026 and create another year of positive underwriting results,” wrote Blades. In particular, he referred to the “judicious use of pricing tools”—notably the increasing use of predictive analytics and telematic in industry pricing models for personal auto and small commercial.

Insurers “have accelerated investments in data, analytics and artificial intelligence (AI) to enhance underwriting precision, improve risk selection and streamline distribution,” he wrote, noting that technology is quickly becoming a critical competitive differentiator for carriers.

As for price competition, AM Best does expect rate momentum in private passenger auto, homeowners and commercial property “to moderate with the potential for profit margins to shrink” in 2026. But he believes there are still underwriting profits ahead for those lines.

Deep or Shallow? Previewing the 2026 Soft Market

Separately, David Paul, principal of ALIRT Insurance Research, expressed a similar view. In a full-year 2025 macro review of the U.S. P/C industry published by ALIRT late last week, Paul noted waning price momentum in commercial lines. Like Blades, Paul suggested that industry fundamentals may have changed for the better in these lines in recent years—a possible signal of continued profit for 2026.

“Almost all industry analysts predict that this result is as good as it gets, at least in the current pricing cycle,” he wrote. He illustrated what analysts are reacting to with a chart showing a history of weighted average rate changes (from CIAB, CLIPS and Marsh) by quarter dating back to fourth-quarter 2016. The numbers on his chart climb from -2% in fourth-quarter 2016 to positive low double-digits in late 2019 through 2020, ultimately drifting back down to 1.5% and 1.3% in the last two quarters of 2025.

With the overall annual industry rate increases now nearly “flat,” there is a real prospect of rate changes going negative in the near term, ushering in a “true soft market,” Paul observed.

“But this does not mean that profitability will unravel all at once—or even at all,” wrote Paul in concluding remarks of his report, which he shared with Carrier Management. “Just as rates rose over an extended period of time, but never with the outsized spikes of prior hard markets, so we may enter an equally extended though shallower softer market cycle,” he predicted. “Much will turn on whether the industry—after an historically long positive pricing cycle—has undergone a secular change in the way it conducts business.”

Paul thinks there is reason to believe this secular change has occurred. Like Blades, he points to carrier investments in data and technology.

“AI insights and agentic tools are being introduced across almost all insurance company silos and one can imagine more targeted (and hence profitable) underwriting/risk selection along with more productive (and hence less costly) claims practices, not to mention overall lower operating costs through improved automation,” he wrote.

“This does not mean that profitability will unravel all at once—or even at all…Much will turn on whether the industry—after an historically long positive pricing cycle—has undergone a secular change in the way it conducts business.”

David Paul, ALIRT Insurance Research

Paul also pointed to fragmentation of the commercial market into specialty niches as a structural change that could lessen the amplitude of pricing cycles. He reasoned that underwriters with “more targeted expertise” might hesitate to trade profitability for top-line growth over the long term.

Right now, Paul believes the P/C industry is in “excellent shape” financially. He bases his assessment on measures of financial and operational strength developed by the research firm known as ALIRT scores—scores which also incorporate assessments of holding financial flexibility and credit ratings of major rating agencies. Commercial lines composite ALIRT scores, he noted, exceeded their multi-decadal average over the past three-and-a-half years.

Like Verisk and APCIA, Paul also reminds subscribers reading his report of the pressures that continue to demand discipline in pricing and terms.

“While it traditionally takes time for aggressive underwriting to adversely impact operating earnings and surplus, the industry remains exposed to the more immediate “known unknowns” of large natural (or man-made) catastrophe losses, economic downturns, inflation, capital market deterioration, and/or the vagaries of a newly disciplined global reinsurance market. Any combination of these factors can impact industry financial results in the more immediate term,” he wrote.

Blades and Paul both said their firms will be tracking individual insurers, the industry and external factors closely over the coming year.

“There are some fundamental positives to build on that we think are going to continue for P/C market,” Blades said in a video interview about AM Best’s recent report posted on the AM Best website. “We’ll keep an eye on all those, and what’s changing throughout the year.”

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent

Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent  Tesla’s Cratering Cybertruck Sales Evoke Ford Edsel Comparisons

Tesla’s Cratering Cybertruck Sales Evoke Ford Edsel Comparisons  Deja Vu as Berkley Calls Out MGUs During Quarterly Call

Deja Vu as Berkley Calls Out MGUs During Quarterly Call