Liberty Mutual’s underwriting results across its businesses came in ahead of targets the company set three years ago when the business was unprofitable, the chief executive reported yesterday, also giving a sense of future strategies.

“In 2026, a key focus is shifting from fixing to building—taking what’s working and scaling it, leaning into our target segments and distribution, and growing only where returns meet our thresholds,” Tim Sweeney said on an investor conference call for Liberty Mutual Holding Company.

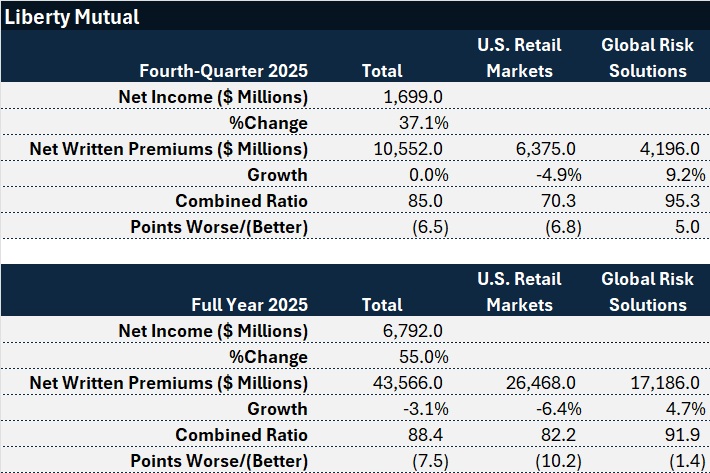

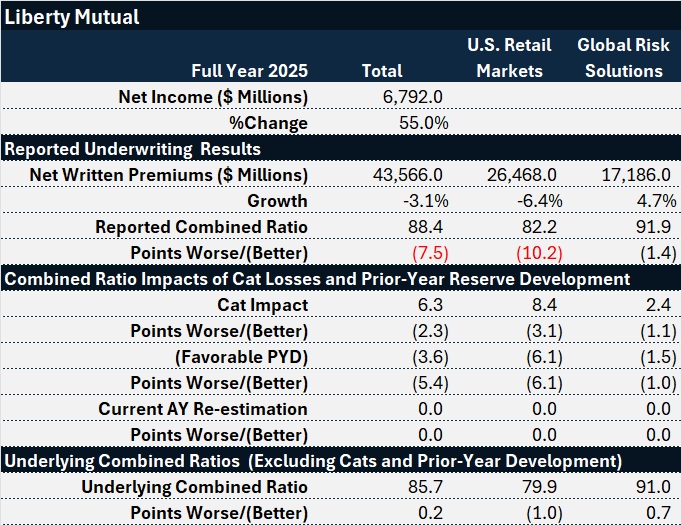

For the full year, Liberty reported a 55% jump in net income to $6.8 billion, with its combined ratio landing at 88.4—7.5 points lower than 2024’s 95.9 combined ratio. Notably, Sweeney highlighted the fact that both the insurer’s two main businesses—the U.S. Retail Markets operation, consisting of U.S. personal lines and small commercial businesses, and Global Risk Solutions segment, writing commercial and specialty insurance, reinsurance and surety solutions to midsize and large businesses worldwide, saw their combined ratios fall below targeted levels of 95 and 92, respectively.

“We made these commitments with a clear recognition that the profitability we were generating at the time was not acceptable, neither for our business nor for the policyholders who depend upon us to keep our promises,” Sweeney said, reflecting on the company’s situation three years ago.

For the full-year 2025, the U.S. Retail Markets combined ratio fell comfortably below the prescribed target, coming in at 82.2—10 points below the reported combined ratio for 2024. Global Risk Solutions ended 2025 right on target, falling 1.4 points to 91.9.

The reported improvements were largely attributable to favorable prior-year loss development, which executives said occurred mainly in the personal auto liability line. Lower levels of catastrophe losses also drove the better reported results in 2025, moving underlying loss ratios down while expense ratios climbed.

Excluding the impact of catastrophes and prior-year development, Chief Financial Officer Julie Haase reported that underlying pre-tax operating income actually decreased by $711 million to $8.7 billion. “This decrease was primarily driven by higher expenses, including increased commissions and advertising in U.S. Retail Markets to stimulate growth, higher employee-related costs, and a shift in external partnership agreements in Global Risk Solutions.”

Across the businesses, Liberty Mutual’s overall underlying loss ratio—excluding the impact of cat losses and prior-year development—fell 2.7 points in 2025, while the expense ratio rose 2.9 points. The underlying 2025 combined ratio of 85.7 was just about even with the comparable 2024 result (85.5).

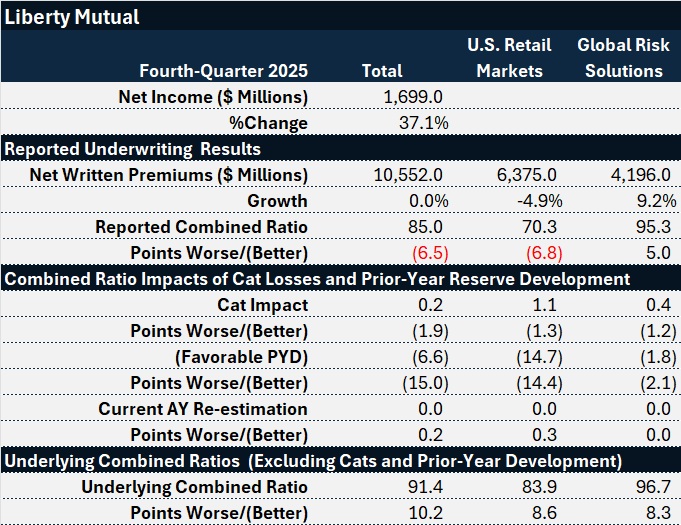

The charts below show the impacts of catastrophe losses and prior-year development changes on the combined ratios by segment for the full year and the fourth quarter.

Focusing on the full year and the larger U.S. Retail Markets division, Liberty didn’t record any prior-year incurred loss movement in 2024 but inked 6.1 points of favorable prior-year development in calendar year 2025. That accounted for a big chunk of the 10 points of improvement in the reported full-year U.S. Retail Markets combined ratio, with a lower level of catastrophe losses accounting for 3 more points of improvement.

The underlying combined ratio, at 79.9, was just one point better than the 2024 underlying combined ratio for the U.S. Retail Markets segment.

Dissecting that into the loss and expense ratio components, the underlying loss ratio improved 4.5 points while the expense ratio rose 3.5 points.

Turning to the top line, Hamid Mirza, president of U.S. Retail Markets business, described the factors impacting a 6.4% decline in 2025, including underwriting actions taken to “build the right portfolio by line,” the transformation of the exclusive agency channel into the digital independent agency (Comparion), closing new business for some inactive segments, and “purposeful action” to reduce average written premium.

“By year-end 2025, we returned to sequential growth in policies in force for personal lines, driven by a substantial increase in new business as we reached record levels of advertising spend and re-engaged our agency partners,” Mirza reported. “Proven and sustainable profit has positioned us to continue momentum and pivot even further into profitable growth heading into 2026,” he said.

The investor conference also marked the first one for Matthew Moore, President of Underwriting for Global Risk Solutions, who will assume the role of President of Global Risk Solutions, replacing Neeti Bhalla Johnson, who is leaving the company.

Moore reviewed market conditions for various specialty lines and other external pressures facing the business but also highlighted the business turnaround he saw as an underwriting leader. “Our combined ratio has improved over 10 points since 2021, a direct result of the disciplined choices we made across underwriting, portfolio management and expense control,” he said.

Also noting a slight uptick in the underlying combined ratio (to 91.0 in 2025 from 90.3 in 2024), he cited “modest pressure from higher employee-related costs, investment in strategic priorities, loss trends that outpaced pricing in certain lines and an increase in small weather-related event frequency. “Those headwinds were largely offset by targeted growth, lower large loss activity, and stronger net investment income, leaving underlying profitability resilient,” he said.

Beyond the advertising and commission expenses that Mirza and Haase mentioned, Sweeney spoke repeatedly about Liberty Mutual’s investments in technology—and AI, in particular—without providing a specific dollar-amount or expense ratio impact.

“We’re not treating AI as a standalone initiative. We’re embedding it into our platforms, data and analytics, and scaling it across the business as a force multiplier for underwriting discipline and long-term performance,” he said, also referring to internal tools (including one he referred to as Liberty GPT), which give employees “access to information, stronger analytical support” and create “more streamlined workflows built into how we underwrite risk, manage claims, and serve customers.”

“Our rollout is deliberate, broad enablement that lifts everyday productivity and decision support alongside targeted scale deployments where we invest behind the highest value use cases, enhancing underwriting insight and workflow speed; accelerating claims, triage and cycle times; improving service responsiveness and consistency.

“As we scale [AI tools], we do so with strong oversight, model validation, and responsible use standards, ensuring these tools augment professional expertise and judgment, not replace it, and that decisions affecting pricing, coverage or claims outcomes remain grounded in underwriting judgment and established governance,” he stated.

“When we do that well, it improves outcomes for customers, supports expense efficiency over time, and reinforces the underwriting culture and long-term focus that differentiate Liberty Mutual,” he said.

Sweeney referred to AI investment again when he was asked what the company intended to do with record levels of capital. After he and Haase spoke about a preference to put capital to use for organic growth before pursuing M&A, Sweeney observed: “Everyone’s talking about gen AI and how it’s going to impact all of our businesses. We view ourselves as having a lot of degrees of freedom to invest what we need to invest in there—to make sure that we’re a winner in that space.”

Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?

Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Home Trend Report: Severity Reaches All-Time High, Frequency Declines

Home Trend Report: Severity Reaches All-Time High, Frequency Declines  Liberty Mutual Introduces Its Newest Brand Character: Liberty Biberty

Liberty Mutual Introduces Its Newest Brand Character: Liberty Biberty