Even the most experienced insurance companies could not have prepared for COVID-19, leaving portfolios riddled with uncertainty for an indeterminate time.

Perhaps no line of business has felt the impact quite like workers compensation, with estimates of 30 million small business claims tied to related losses. In California, for example, 11.2 percent of workers comp claims in 2020 have been pandemic-related, according to the California Workers’ Compensation Institute.

Although the full effects of the pandemic are still unraveling, workers comp insurers clearly face a few significant impacts:

- Some state-specific legislation may require carriers to presume compensability for COVID-related illnesses assumed to have resulted in the course of employment.

- Due to business interruption, payrolls may decline significantly from prior years—putting premium at risk.

- Plummeting interest rates may significantly decrease investment yields.

The combination of these factors puts further pressure on insurers to achieve underwriting profitability to make up for lost premium and investment income. As such, insurers must get creative in their use of data analytics, not only to get a handle on exactly how this pandemic is impacting their portfolios but also to focus on areas for growth.

Using geospatial analytics is an example of how some workers comp insurers are getting creative in their use of data analytics to understand risk. More commonly utilized for property risk selection and evaluation, geospatial platforms enable insurers to visualize risk and achieve a ground-level view of this pandemic’s impact on their portfolios. For example, by using up-to-date COVID-19 data, unemployment data from the Bureau of Labor Statistics (BLS), alongside their own portfolio data, insurers can use a geospatial analytics platform to visualize exposure and dig deeper into potential claims and premium at risk. Additionally, other forms of data such as census population, industry wages and even risk scores derived from predictive models can be layered into a geospatial analytics platform to provide deeper insights. Armed with this information, insurers can better understand potential COVID-related claims, premium at risk and new business growth opportunities.

Here are three ways to use data and analytics to understand the business impacts of COVID:

- Anticipating Potential COVID-19 Claims

As COVID-19 infections continue to fluctuate and even rise in many states, insurers can use a geospatial analytics platform to map COVID-19 hot spots and visualize the largest potential increase in pandemic-related workers comp claims by layering up-to-date COVID-19 data with their payroll data. To create an accurate and relevant depiction of high-risk areas, insurers can combine the highest active COVID-19 cases as a percentage of the population of a region with the amount of insured payroll.

To go one level deeper, these insights can be filtered through the North American Industry Classification System (NAICS) to visualize high-risk industries and determine the businesses that are most likely to be affected by pandemic-related claims. This granularity is important because state-enacted COVID-19 compensability legislation may increase claim severity for certain industries, such as frontline healthcare workers where illness is assumed to have resulted in the course of employment.

Armed with this data, insurers can take several important proactive measures that would otherwise be unavailable to them:

- Discuss mitigation activities with insureds, collaborating to limit employee COVID-19 exposure during work hours.

- Take a closer look at the state-specific COVID-19 claims regulations.

- Plan for potential losses well in advance of claims filing.

Any effort guiding policyholders during this time is crucial for both the business and customer satisfaction.

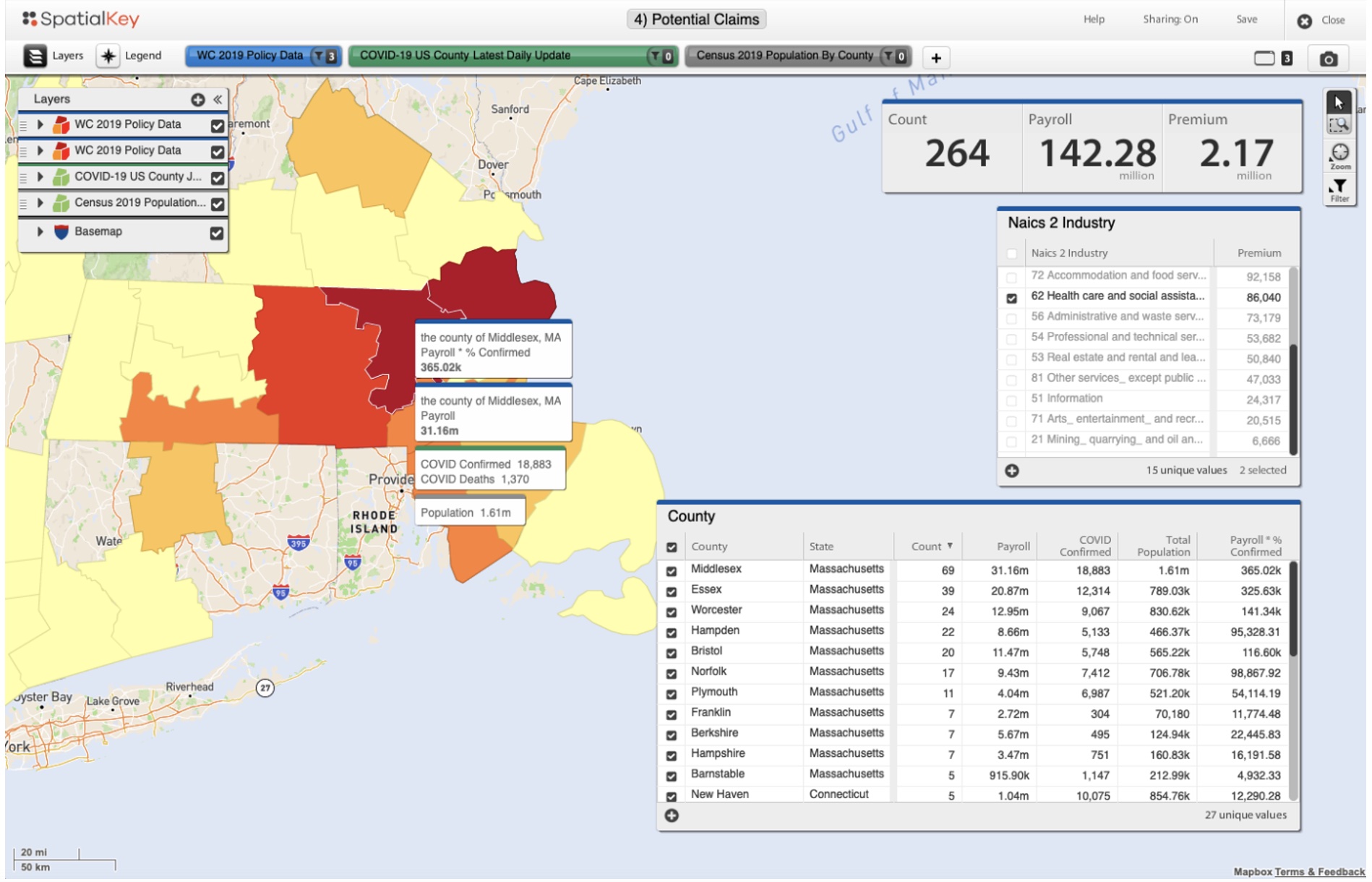

Figure 1: The above screenshot shows counties in which insurers may experience higher COVID claims based on filters applied on high-risk industries such as healthcare. It also considers the percentage of confirmed cases (i.e., the number confirmed as a percent of the population). In this example, if an insurer’s payroll were to be impacted at the same rate that COVID is impacting the population in Middlesex, Mass., they could expect to see $365,000 in payroll impact for healthcare workers.

- Anticipating Premium at Risk

Beyond claims, insurers are also looking to data and analytics to help them anticipate potential premium at risk due to high unemployment rates. When lockdowns first began in March 2020, U.S. unemployment reached 14.7 percent, the worst since 1940. Although it’s showing signs of improvement, now down to 6.3 percent as of January 2021, there are plenty of layoffs that continue across the country. With so many businesses laying off or furloughing workers, there can be higher volumes of insured premium loss. Insurers often identify exposure reduction during an audit that occurs several months after the end of the policy term. As such, this could leave insurers blindsided by loss in premium well into 2021.

Using geospatial analytics, insurers can measure and visualize exposure by layering the BLS unemployment data against insured payroll to determine portfolio businesses most at risk for policy termination, delayed premium payment or premium reductions as policies come up for review. NAICS data can also be used to target and isolate specific industries that are more susceptible to layoffs, such as restaurants and airlines. For example, if an insurer has 15 restaurant policies in Atlantic City, N.J., where unemployment rates are high, it can determine that these are among the highest risks in its portfolios. These types of powerful insights enable insurers to prepare for and react to potential premium loss.

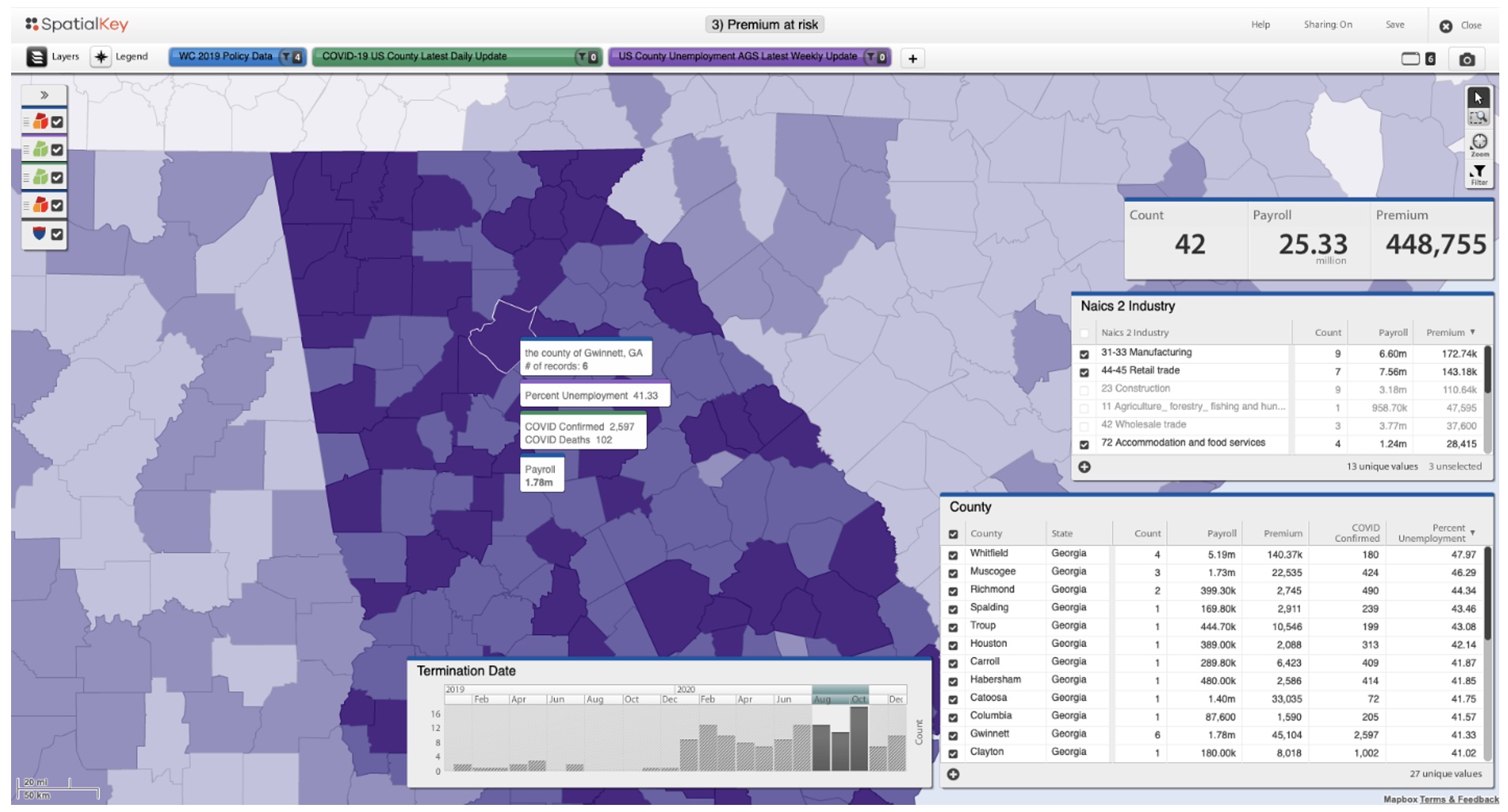

Figure 2: The above screenshot shows areas with the highest percentage of unemployment (dark purple). Coupling this information with an insurer’s employee count per county provides a way to focus on the areas that matter the most. The insurer portfolio data shown here has six policies in Gwinnett, Ga., that may be impacted by shelter-in-place orders. The unemployment rate is over 41 percent in this county. Given the extremely high unemployment rate and that these six policies may have a higher chance of layoffs, the insurer may want to reach out to check on the reality of potential payroll reductions.

- Identifying New Business Opportunities During COVID-19

With workers comp insurers facing potential premium loss, they cannot afford to pump the brakes on identifying new business opportunities. The COVID-19 data overlayed with an insurer’s portfolio data provides an excellent starting point to identify problematic growth areas for insurers in real time, especially in places where they might typically have large market penetration and expertise in writing business. Insurers need to make several challenging decisions with massive potential ramifications, such as whether to alter their typical premium structure in higher-than-average COVID-19 infection areas or go after business in entirely new adjacent areas less affected by the pandemic.

Data analytics can help insurers confidently make these risk selection determinations. The insights can be even more effective by leveraging predictive models for underwriting, where they can begin to identify new growth areas within their risk appetite. Other variables, such as industry type, can also be layered to make more granular decisions when it comes to securing new business during the pandemic.

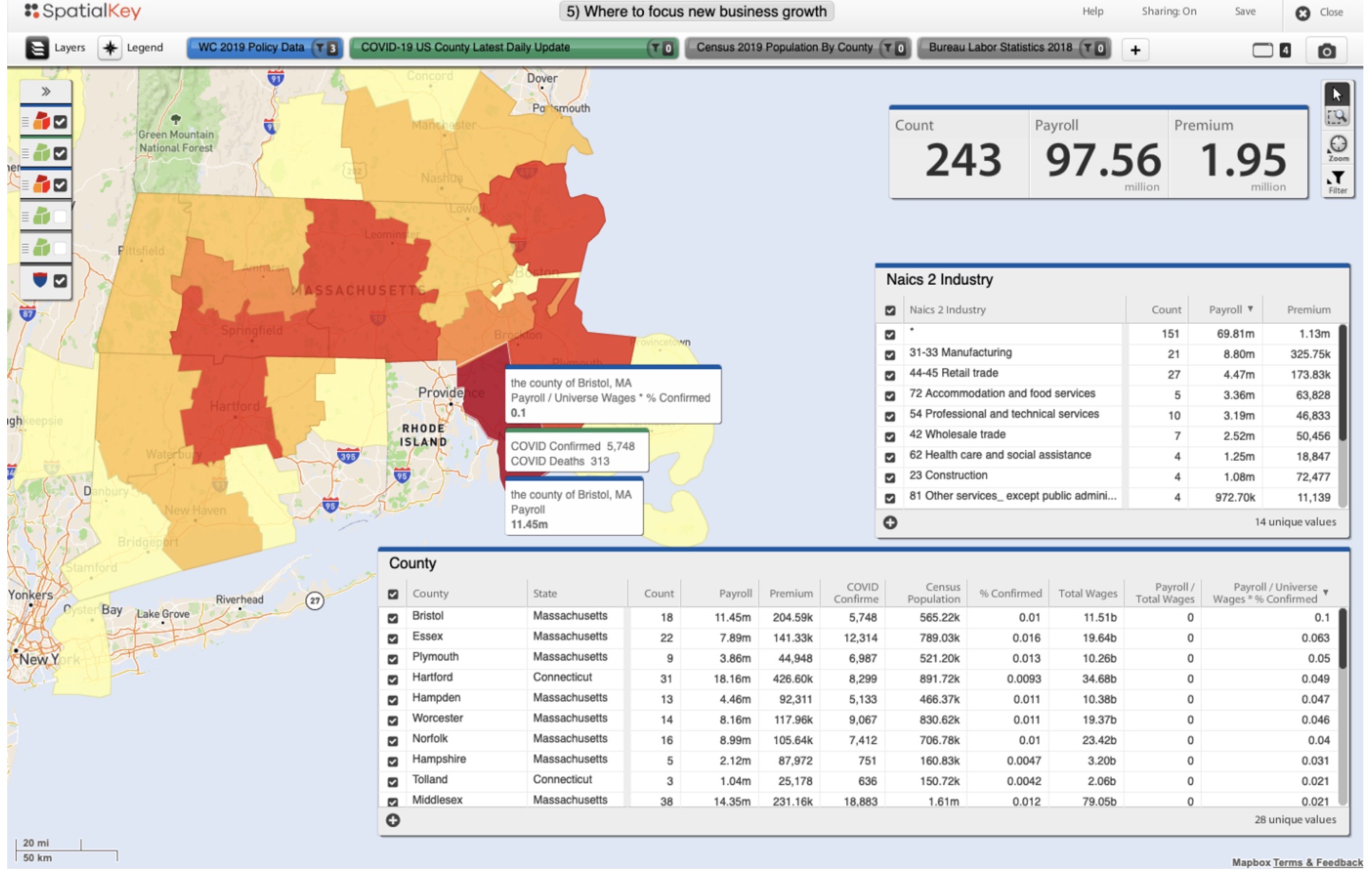

Figure 3: In the above screenshot, attention is drawn to areas where an insurer may want to avoid marketing and growth activities while COVID-19 is still a concern. The areas in red represent areas where there is a high number of COVID confirmed cases and where an insurer has higher market penetration.

Figure 3: In the above screenshot, attention is drawn to areas where an insurer may want to avoid marketing and growth activities while COVID-19 is still a concern. The areas in red represent areas where there is a high number of COVID confirmed cases and where an insurer has higher market penetration.

These are just a few of the ways that third-party data can be used within a geospatial analytics platform to help workers comp insurers understand and visualize the impact of the pandemic on their portfolios. Through the insights gained by layering intelligence in this way, insurers can proactively take steps to mitigate and manage risk, serve insureds, and identify potential opportunities to grow—even amidst a challenging and unprecedented workers comp market.

Will AI Be the End of Insurance Agents?

Will AI Be the End of Insurance Agents?  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs