Property/casualty insurers have widely adopted the principles of relational database management into their policy administration systems, but the potential benefits of that approach for data analysis are often limited by a siloed approach to system design.

Statistical reporting applications are all too often developed as an afterthought, and there is very little flexibility in management reporting.

While carriers have embraced relational database management within insurance functions, the full benefits of that approach aren’t apparent until it is implemented as uniformly as possible across an entire enterprise. To accomplish this, executives are advised to understand the basics of relational database management and to develop in-house competence regarding the capture, reporting and—most importantly—the connectivity of data across all insurance functions. (Related article: Data Connectivity in a Carrier: Solving a Common Problem)

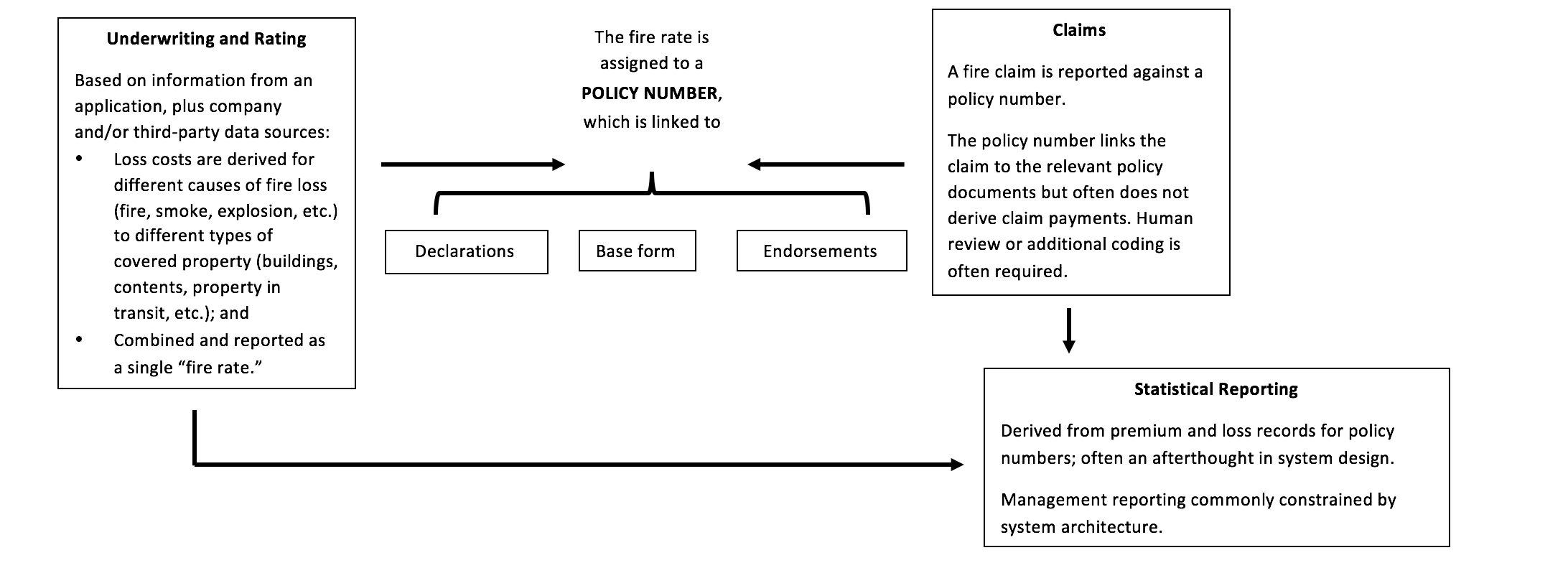

To illustrate, let’s consider a simple example of a fire premium and a fire loss. (Click image to expand).

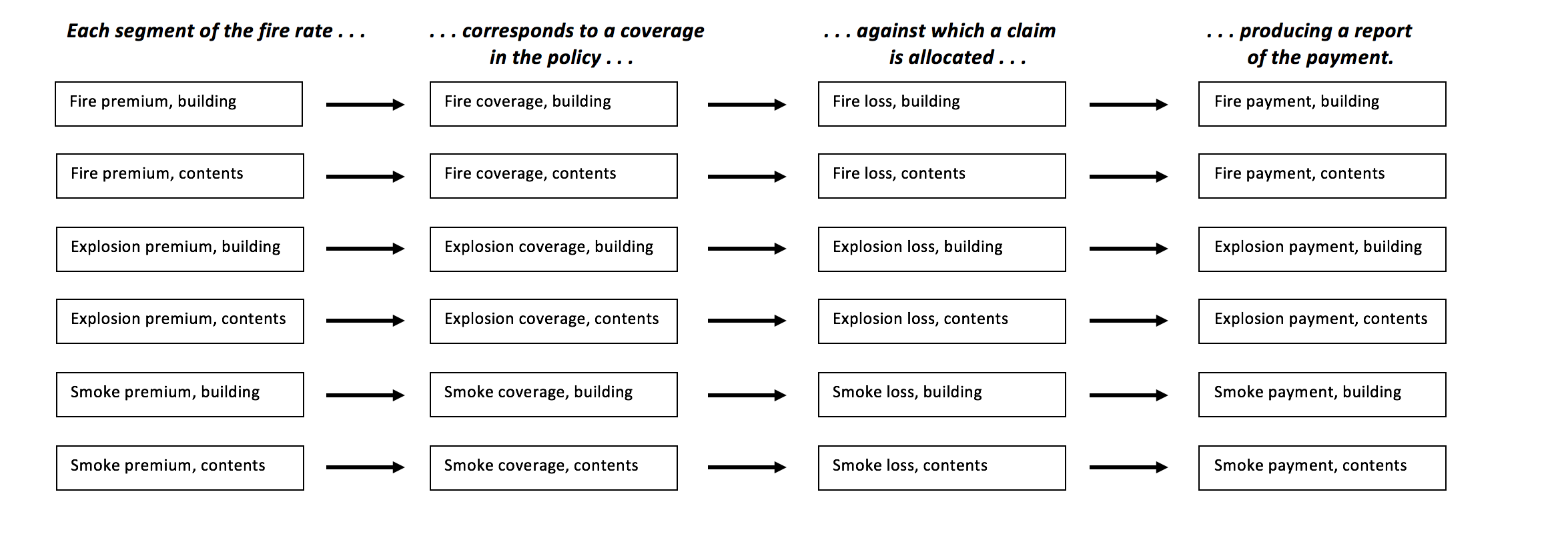

This is how it might work if data elements were designed to be linked across your enterprise. Although this representation may appear to suggest more work, a well-designed system will create these records automatically, giving managers far more flexibility in querying their data for strategic analysis. (Click image to expand)

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz  AXA XL to Acquire S-RM

AXA XL to Acquire S-RM