Imagine that you receive a quote application from a residential remodeling company working out of a Pennsylvania town near Philadelphia who also does business across the Delaware River, in New Jersey. As you pore over the application, which may include more than 90 queries, you have more questions about the company than you see answers.

What work does this contractor really do? The owner filled in her crew’s primary and secondary capabilities—residential remodeler and finished carpentry. But do they work on anything more substantial, which could increase the risk involved?

In reality, the firm accepts jobs in both New Jersey and Pennsylvania, works with industrial-strength chemicals, and has helped build new strip malls and office buildings in the past decade.

In the end, the result is twofold: You took onto your portfolio additional business owners policy (BOP) risk that’s better suited for a small-commercial package, but you missed an opportunity to recommend additional coverage to the insured. And those results can affect your profitability, especially if it happens frequently.

Fortunately, this is only a hypothetical situation. And it doesn’t have to happen.

Underwriting with speed and accuracy

Among small commercial underwriting sectors, the contracting industry is one of the most complex to assess. In fact, it’s the most diverse business in terms of classifications. Consider a contractor that operates in both the residential and commercial spaces with a focus on carpentry, electricity, and roofing, or a landscaper that’s involved in excavation, snowplowing, and roof cleaning, even if only occasionally.

An area of opportunity: The construction segment represents $25.9 billion in annual premium.*

Misclassifying risk—contractors who only lay kitchen floors and install cabinets, for example, might be confused with those who provide full-service work—could be the result of data that’s not granular enough to uncover insights on a business’ operations and risk characteristics. And bad data could lead to incorrect pricing, lower retention, and a drop in profitability.

P&C insurers need greater data and analytic insights to underwrite with speed and accuracy—and to achieve automated underwriting. Traditional solutions are valuable, but the ability to harness unstructured data introduces additional data points, information granularity, and better currency.

Taking the step to find high-quality data simply makes sense to ensure that you underwrite with accuracy and greater speed and to power your automated underwriting strategy.

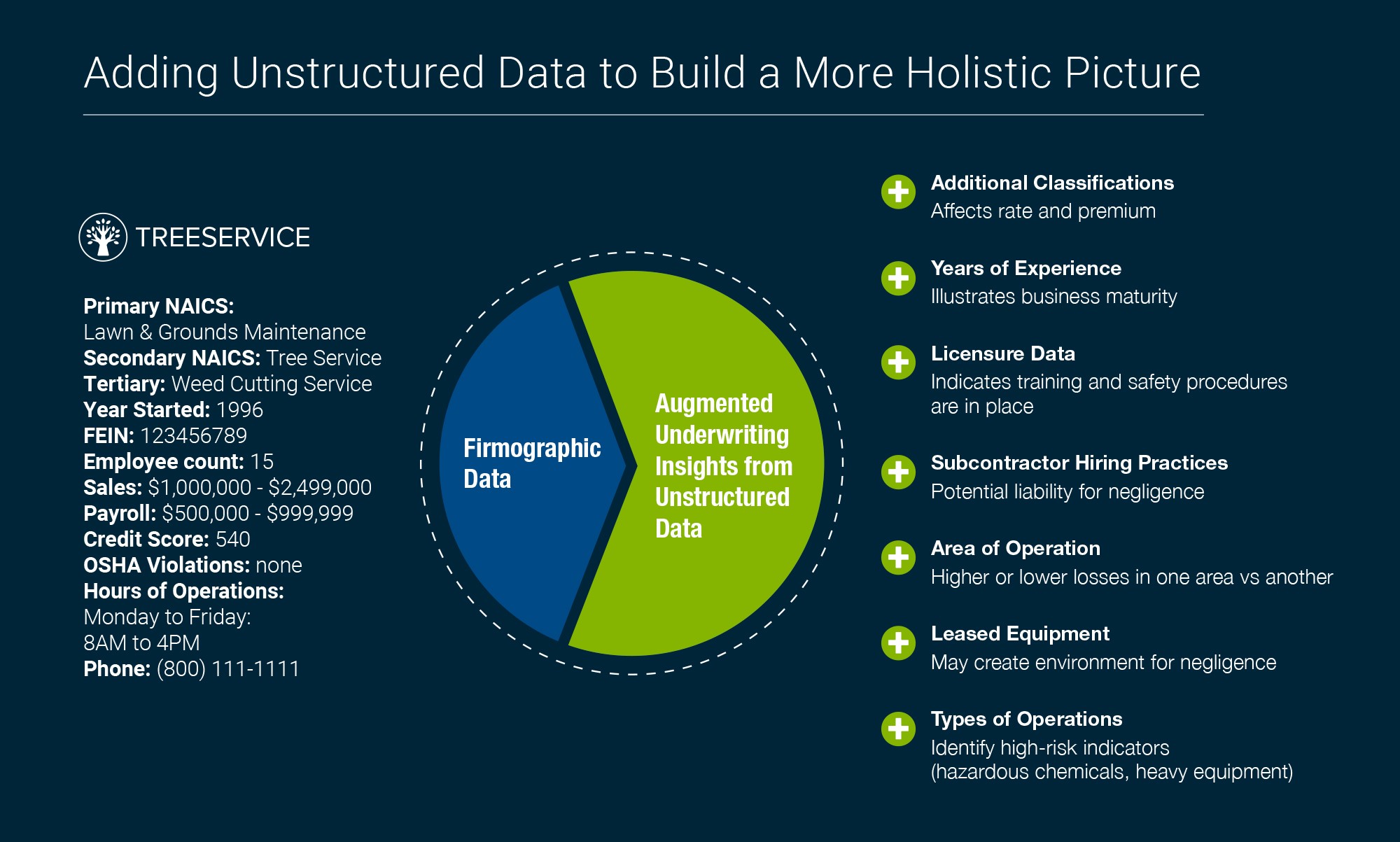

As illustrated in the visual below, new data sources, such as social media, and advances in technology, such as machine learning and artificial intelligence, can help insurers get a better view into the risks they’re underwriting at time of quote.

It’s all a part of the industry’s “race to zero,” which would mean zero questions for applicants to answer. The drive to automate the underwriting process combines rigorously audited data and proven analytics. Together, they dramatically reduce the number of questions for faster application processing, enable more accurate and reliable risk assessments, and help insurers provide a better customer experience. The more comprehensive your data and insights are, the better the chance you’ll have to appropriately price your policies, more suitably cover your insureds, and maintain profitability.

A new era is dawning

Verisk is leading the way with an ecosystem of existing sources of data plus previously untapped sources. The new sources include partnerships with social media sites and marketplaces, and business websites. We’re gleaning business insights from them to help reduce the need for manual underwriting, and we’re able to do so responsibly thanks to our partnerships and relationships with those sources.

31 codes in the standard NAIC classification system compared to nearly 700 unique classes identified by Verisk.

Starting with the contracting industry—a good example of a sector with high volumes, complexity, and frequently shifting risk—our efforts are designed to help insurers gain valuable underwriting insights: a more granular understanding of business classifications, identification of unknown risk exposures, and indicators of how well a business is managed.

The result: Verisk is positioned to help insurers see more clearly—and farther—down the road, with insights to help reduce the number of questions asked and enabling more risks to be automatically underwritten. We’re making it easier for you to write contractor policies with greater confidence, speed, reliability, and accuracy. It’s a win for your customers, too, because it helps you appropriately price the risk and provide policyholders with the right coverage.

For more information on how you can leverage data and analytics to automate your small commercial underwriting, visit Verisk.com/LightSpeedSmallCommercial. You can also download our white paper, Automated Underwriting: Winning the Race to Zero.

_________________________________________________

By: Othman Loudghiri, senior product manager for small commercial underwriting at Verisk. He can be reached at othman.loudghiri@verisk.com.

*ISO MarketStance

NYC Orders Pause of Construction on Damaged Midtown Office Tower

NYC Orders Pause of Construction on Damaged Midtown Office Tower  How We Did It: How a 150-Year-Old Mutual Transformed Culture to Drive AI

How We Did It: How a 150-Year-Old Mutual Transformed Culture to Drive AI  Prosecutors Can Review Tiger Woods’ Med Records in Florida DUI Case: Judge

Prosecutors Can Review Tiger Woods’ Med Records in Florida DUI Case: Judge  Sompo Acquiring Workers Comp Writer Service Insurance Companies

Sompo Acquiring Workers Comp Writer Service Insurance Companies