As the popularity of large tract home neighborhoods continue to grow due to the quest for “affordable luxury,” underwriters are challenged with how to distinguish between the two home types when assessing structure risk and accurately pricing homeowner policies. Because they appear similar due to the sheer size of both homes, traditional methods of pricing Coverage A could run the risk of over insuring large tract homes. While some may think it’s better to be over insured then underinsured, carriers who do not have a methodology in place for discerning between the two run the risk of losing customers who may find a more affordable policy elsewhere.

The secret to more accurately pricing large tract homes is twofold.

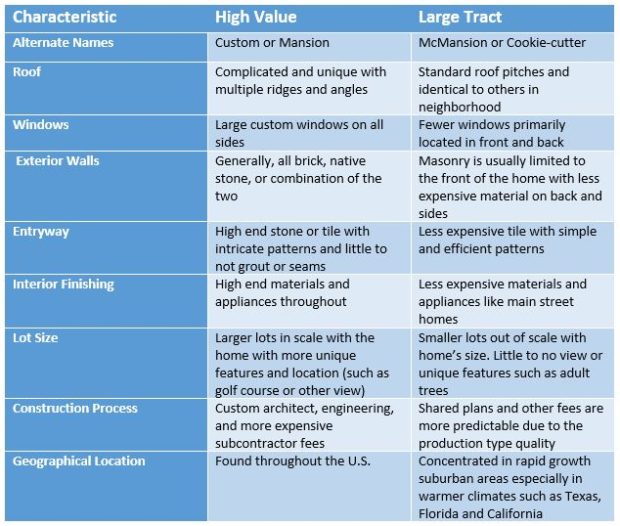

First, it’s important to understand what makes them different. The table below gives specific examples of ways in which these home styles vary.

Caption: This picture identifies some characteristics common of large tract homes.

Second, to avoid the challenge of consistently differentiating between the two across an enterprise, it’s important to leverage a tool that automates this decisioning within the underwriting workflow. A tool that is built to identify large tract neighborhoods with Zip+ 4 granularity from just an address, and that also has the appropriate property characteristics of a large tract home within its knowledge tables, lessens the subjective decisioning of a tool wherein the user needs to manually reduce quality based on homeowner- or agent-submitted information.

For more information, visit the RCT Express® webpage.

Report Reveals Mixed Collision Trends as Fleets Work to Implement Safety Programs

Report Reveals Mixed Collision Trends as Fleets Work to Implement Safety Programs  Leave it to Me: Overconfident CEOs Less Likely to Delegate M&A Work

Leave it to Me: Overconfident CEOs Less Likely to Delegate M&A Work  Farmers Insurance Plans Historic, Rapid Expansion of Agency Force

Farmers Insurance Plans Historic, Rapid Expansion of Agency Force