Insurers affected by Hurricane Ian’s damaging path across Florida at the end of September 2022 faced operational, regulatory and statutory requirements for accurate projections of the ultimate financial cost of the damage. Accustomed to using catastrophe risk models to project their ultimate losses, the uncertainty bounds on their loss estimates were considerably higher for this event. While hurricane loss models are capable of estimating damages and insured losses to buildings and assets to some known degree of certainty, there are other sources of loss which are less certain.

These uncertainty factors are referred to as post-loss amplification factors. These include a demand surge factor, i.e., a short-term run-up in prices driven by the extraordinary costs of importing outside workers and materials, and cost-inflation factors arising from regulatory aspects like the assignment of benefits law (AOB) in Florida. These post-loss amplification factors have plagued the Florida insurance market for many years and have been gradually getting worse, culminating in a seemingly never-ending upward spiral of claims costs for Hurricane Irma in 2019.

Recent levels of historically high inflation fueled by supply shortages of materials and high energy costs have contributed to significant increases in the cost of everyday goods and services, with consumer price inflation peaking at just under 10% earlier this year. Labor shortages also continue to be an issue, with the National Federation of Independent Businesses reporting hiring to be as hard as ever.[1]

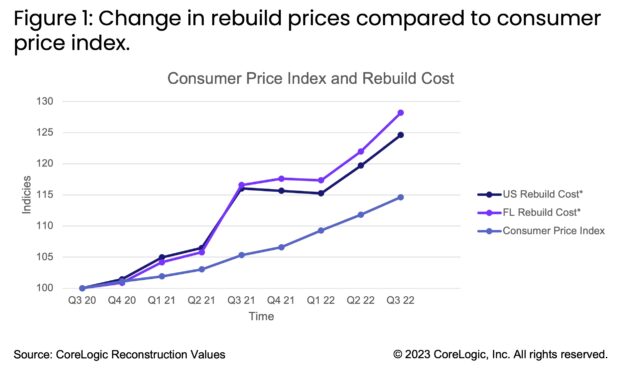

The costs of construction materials and labor used for rebuilding have been rising faster than general inflation, with levels just under 15% at the beginning of 2022. We can see in the graph below that these costs have seen an even steeper rise in Florida.

Figure 1: Change in rebuild prices compared to consumer price index.[2]

CoreLogic loss estimates have been calculated using the latest values for rebuild costs. The problem is that insurers or agents may be looking at schedules or values from twelve months or more ago which could be undervalued with little or no future inflation built into the schedule. Costs to insurers are incurred once the repair is complete. As of November 22, 2022, almost 50% of the insurance claims were still open and 25% were still open as of January 20, 2023.[3] The costliest claims take the longest time to repair with inflation driving ultimate costs higher. This lag is even longer for reinsurers.

In 2017, Florida had a significant change to the building code for existing buildings which required an entire roof section to be replaced where 25% or more of a roofing section is damaged and where there were errors with the permitting, installation, or inspection.

Assignment of benefits is an established practice in Florida that enables a property owner the ability to hire a contractor to repair their property and to assign the benefits of their insurance policy to the contractor in lieu of a direct payment. Devised to deliver agility and speed to homeowners seeking repairs to their property, the addition of attorney settlement fees to the claim have increased costs to insurers for settlements and, ultimately, has increased costs to homeowners.[4] In May of 2022, Florida’s legislature implemented reforms to the AOB laws and the effectiveness of these reforms is untested.

The revised 2017 regulations on AOBs such as reduced claims windows, price of cancellation, and contingent fees will have a significant impact on lowering costs only if insurers can stop dubious actors from contacting their clients and proactively starting to handle settled claims early. Further reforms enacted by emergency legislative session have now (going forward at least) banned the ability of policyholders to assign the benefits of their policy to 3rd parties and restricted the ability to recover legal fees. However, the legislation is not retroactive, so claims from Hurricane Ian could still be subject to AOB-inflated losses.

Hurricane Ian and Housing: By the Numbers

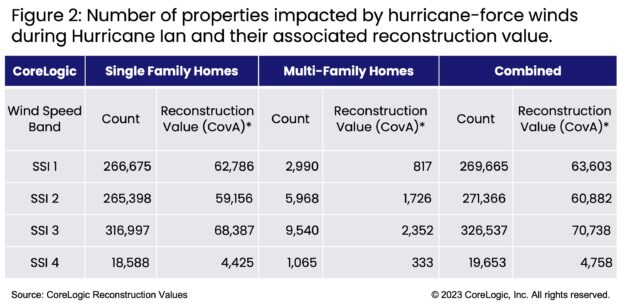

CoreLogic estimates that almost 900,000 homes were subject to hurricane force winds, and 600,000 of those were subject to severe Cat 2 or Cat 3 wind speeds. Per the Florida Office of Insurance Regulation, approximately 475,000 residential claims were on file as of January 20th, 2023, up from 440,000 claims on file as in November 2022.

The continued stabilization of these claim numbers may be evidence of the improvements made to home-strengthening building code regulations in the years since Hurricane Andrew (1991). This high-volume of claims will be a test of not only the adequacy of the recent AOB reforms in reducing overall repair/insurance costs for homeowners to repair/insure their homes but also a test for insurers and reinsurers in managing the uncertainty of determining the ultimate cost of Hurricane Ian.

To learn more about the impacts of Hurricane Ian 6 months after landfall, see a recent CoreLogic webinar exploring the findings of a damage survey in Southwest Florida including a detailed breakdown of the modeled losses and what made this hurricane event so unique.

By: Paul Brown, Saumi Shokraee

©2023 CoreLogic, Inc. The CoreLogic® statements and information in this article may not be reproduced or used in any form without express written permission. While all the CoreLogic statements and information are believed to be accurate, CoreLogic makes no representation or warranty as to the completeness or accuracy of the statements and information and assumes no responsibility whatsoever for the information and statements or any reliance thereon.

[1] https://www.nfib.com/content/press-release/economy/nfib-jobs-report-nearly-half-of-small-business-owners-still-cant-fill-job-openings/

[2] U.S. Bureau of Labor Statistics, Consumer Price Index

[3] https://www.floir.com/home/ian

[4] https://floir.com/consumers/assignment-of-benefits-resources

Preparing for an AI Native Future

Preparing for an AI Native Future  How Americans Are Using AI at Work: Gallup Poll

How Americans Are Using AI at Work: Gallup Poll  Experts Say It’s Difficult to Tie AI to Layoffs

Experts Say It’s Difficult to Tie AI to Layoffs