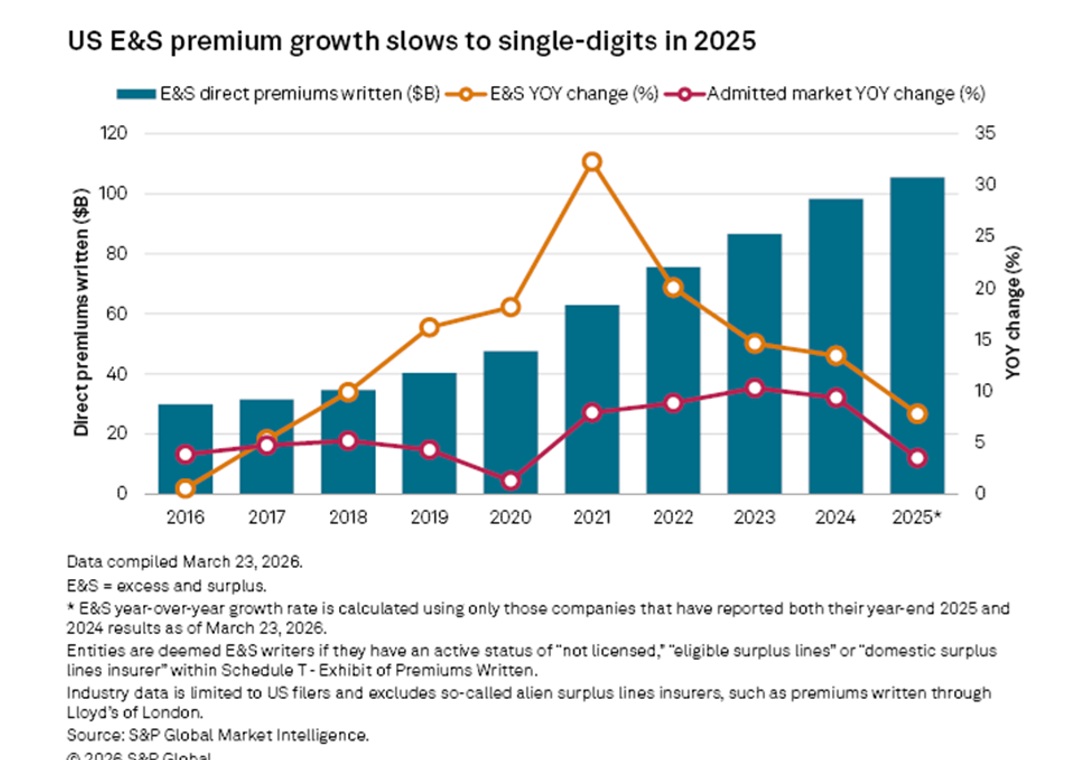

A recent analysis by S&P Global Market Intelligence reveals that the pace of growth in the U.S. excess and surplus lines market slowed to 7.8% in 2025, marking the first single-digit growth rate recorded since 2017.

Previous reports from S&P GMI showed U.S. E&S direct premiums jumping 14.5% in 2023 and 13.4% in 2024, with those double-digit growth rates paling in comparison to a 32.3% percent rate of growth recorded in 2021.

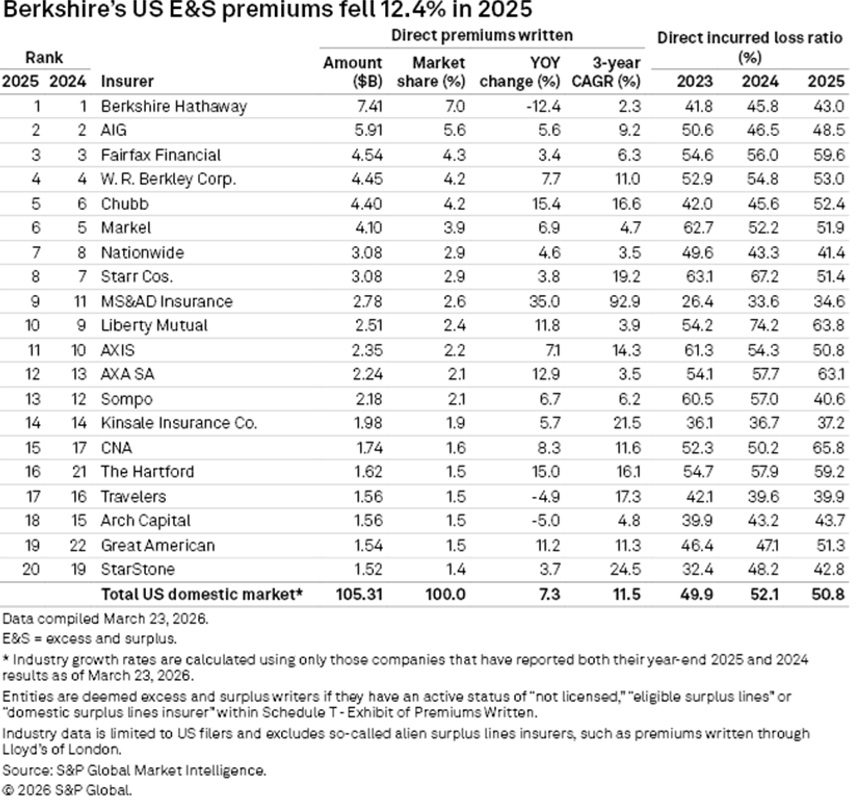

Contributing to the slumping growth rate, S&P GMI reported a drop in premiums for the largest U.S. E&S player—Berkshire Hathaway—last year. Berkshire Hathaway’s recorded 12.4% decline in overall E&S premiums to $7.4 billion was the largest drop among major insurers, with its E&S property business line falling 22.7% to $3.1 billion.

A Carrier Management comparison of the premium data in the latest report with a prior S&P GMI report on the U.S. E&S market published in June last year reveals that only two other insurers among the top 20 E&S players recorded drops in E&S direct premiums last year—Travelers and Arch Capital—each showing declines of roughly 5%.

Still, the U.S. domestic E&S market overall reached a historic milestone last year, by surpassing $100 billion in direct premiums written for the first time, according to S&P GMI which reports an industrywide total of $105.3 billion for 2025.

(Editor’s Note: For the latest report, S&P GMI limited year-over-year industrywide comparisons to entities that have filed 2025 results so as to not artificially understate the overall growth rate. According to the report, at the time of publication, there were about a dozen insurers representing roughly $500 million in direct premiums written in 2024 that had not yet filed their most recent full-year results.)

Individual insurance groups reporting double-digit premium jumps included Chubb, MS&AD Insurance, Liberty Mutual, AXA SA, The Hartford and Great American (based on a Carrier Management comparison of figures in the latest report with a prior report).

Across the industry, S&P GMI attributed the overall slowdown in E&S premium growth to declining commercial property premiums amid intensified market competition. In contrast, on the residential property side, the homeowners segment still had double-digit growth driven by climate-related displacement from admitted markets.

More specifically, commercial property business lines experienced a 2.8% decline to $27.7 billion, marking the first decrease since 2017, while E&S homeowners premiums surged 29.5% to $4.1 billion.

“This divergence reflects cyclical market dynamics, with commercial property facing intensified competition from both admitted and non-admitted insurers, whereas homeowners coverage continues benefiting from carrier retreats in catastrophe-prone states including California, Colorado, Florida and Texas, demonstrating sustained displacement from traditional admitted markets,” S&P GMI said.

Offering evidence of the degree of competition among commercial property writers, S&P GMI reported that large account commercial property renewal rate declines were in the 25% to 35% range during the fourth quarter last year, representing an acceleration in competition from earlier periods. “This pricing pressure prompted some small commercial businesses to migrate back to the admitted market, though the shift remained limited.”

For the E&S homeowners segment, S&P GMI calculated a three-year compound annual growth rate of 34%, and said that 2025 marked the third consecutive year of growth exceeding 20%. The figures reveal the homeowners line as “a critical growth engine” for the E&S industry, S&P GMI analysts said in a media statement about the latest E&S report.

Focusing on the largest player, S&P GMI reported that Berkshire Hathaway’s most dramatic reduction in E&S premium occurred in commercial multiperil non-liability, which plummeted 70.3% year-over-year to $192.6 million from $648.2 million. Premiums also declined for occurrence and claims made liability business written by the E&S insurance operations of the conglomerate, while Berkshire’s E&S commercial auto direct premiums saw double-digit growth, according to figures in the report.

Analyzing the distribution of industrywide premiums across the E&S market by line, S&P GMI reported that property lines account for 30.2% of the market. Liability and casualty coverages still dominate, capturing a 54.9% market share. Commercial auto represented 5.6% of total 2025 E&S direct premiums tallied by S&P GMI so far.

Driver Death Rates High for Small Cars, Big Engines: IIHS

Driver Death Rates High for Small Cars, Big Engines: IIHS  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns

Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz