Rising inflation in Europe, which jumped to 8.9 percent in July 2022—the highest in 25 years—will hurt the profitability of property/casualty insurers in 2022-2024, according to London-based data and analytics company GlobalData.

Premium growth is expected to be slower as rising inflation will affect the ability of policyholders to pay higher premiums, said a research note issued by GlobalData. At the same time, the average cost per claim is expected to increase, which will reduce the profit margin of general insurers.

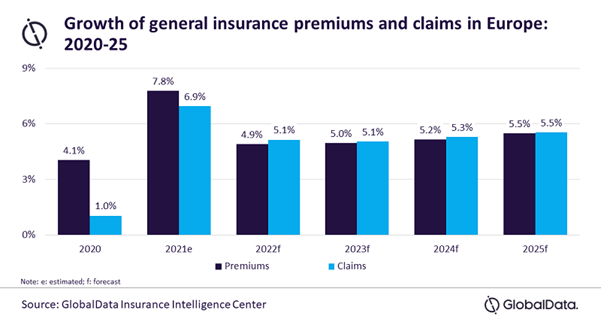

General (or P/C) insurance claim payouts in Europe are expected to grow by 5.1 percent in 2022, whereas premiums will grow at a lower rate of 4.9 percent, further indicating a negative impact on the profitability of insurers, GlobalData continued.

Property insurance is vulnerable to inflation as rebuilding and repair costs are directly linked to the cost of materials and labor, according to the research note.

“Inflation in European countries has increased sharply since the beginning of 2021. This was initially due to the prolonged economic impact of COVID-19 but has been further exacerbated by the Russia-Ukraine conflict and the resulting supply chain disruptions in 2022,” commented Swarup Kumar Sahoo, senior insurance analyst at GlobalData, in a statement. “Following this, the price for the average claim has increased, impacting most general insurance lines, especially property, motor and specialty insurance.”

“Factors such as rising raw materials prices, disruptions in supply and labor shortages are expected to shoot-up the average cost of claims for both commercial and household property insurance. As a result, property insurance claims are expected to grow by 6.4 percent in 2022 while premiums would grow by 5.6 percent,” the note continued.

Pointing to a specific line, GlobalData said motor insurance claims growth is expected to increase from 1.6 percent in 2021 to 4.0 percent in 2022, against a decline in premium growth from 6.4 percent in 2021 to 4.3 percent in 2022.

Motor insurance claims are expected to rise in 2022 due to higher replacement costs, third-party payouts, litigation costs and wages, GlobalData said, noting that the rising cost of claims will affect insurers’ claims reserves used for paying unsettled claims from previous years.

“The burden of rising inflation and cost of claims will prompt insurers to review their risks. This will lead to an increase in premium for both new policies and renewals,” the research note continued.

“Rising inflation and the cost-of-living crisis will not only lead to higher insurance rates and tougher conditions for the market but will also push policyholders toward underinsurance and keep general insurers’ profitability under pressure,” said Sahoo.

“Striking a balance between profitability, premium growth, as well as customer retention, is expected to be a key focus area for European general insurers over the next few years.”

Source: GlobalData

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak  Mapfre to Acquire Safety Insurance in $1.5B in Cash Deal

Mapfre to Acquire Safety Insurance in $1.5B in Cash Deal  This Year’s SCS Loss Totals Will Fall Below Average: KCC Analysis

This Year’s SCS Loss Totals Will Fall Below Average: KCC Analysis  Waymo Driverless Cars Crash Less Than Human Drivers: IIHS Study

Waymo Driverless Cars Crash Less Than Human Drivers: IIHS Study