Customers who switch auto insurance carriers due to poor service often end up sorry they did because they end up paying more with their new insurer, according to the latest J.D. Power 2014 U.S. Insurance Shopping Study.

While a poor experience with their insurer is the leading reason customers shop for, and ultimately switch to a new auto insurance company, declining new price satisfaction is the primary reason customers are less satisfied when they do switch insurers, the survey says.

“The insurance industry spends billions of dollars each year on advertising, and over the last seven years many of those ads have tried to entice customers with big savings,” said Jeremy Bowler, senior director of the insurance practice at J.D. Power. “While switching to a new insurer usually results in savings, the ads make promises of savings that a growing number of new customers don’t believe they’ve received.”

According to the study, 30 percent of auto customers shopped for a new insurance provider in 2013, among whom 36 percent ultimately switched insurers. Customers who experience a premium increase shop at a rate of 13 percent—less than half the rate of shopping among those who have a poor experience (28 percent).

Rate increases do not drive customers to shop as much as poor service does, as customers are tolerant of a certain level of rate increases, according to the survey. However, rate hikes of more than $200 can triple the rate of customers who switch insurers.

Price is still important in the selection process—eight in 10 customers continue to select the lowest-priced insurer—and price is also an increasingly important driver of new-buyer purchase experience satisfaction once customers have selected a new insurer.

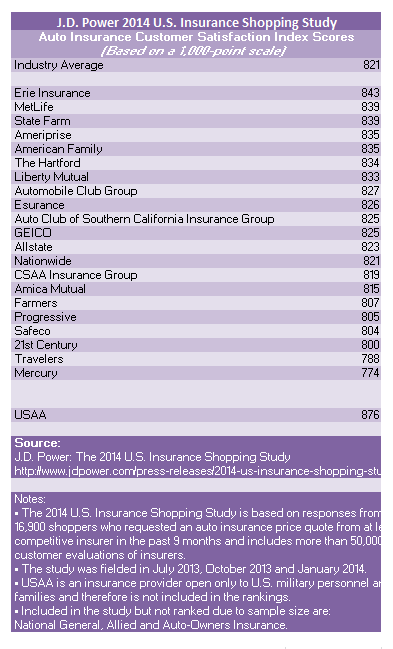

Overall new-buyer satisfaction with the auto insurance purchase experience averages 821 (on a 1,000-point scale), down from 828 in 2013. The decline in satisfaction is driven by a 17-point drop in the price factor, which has the greatest impact on satisfaction.

On average, customers saved $300 when switching insurers in the past 12 months. The longer customers had been with their previous insurer, the greater the savings when they switched carriers, likely because they had been experiencing rate increases, according to the researchers.

Customers who were with their prior insurer for 11 years or longer before switching save an average of $426 per year on their premiums, compared with $291 among those who had been with their previous insurer less than two years before switching.

Moreover, satisfaction among customers who had been with their insurer 11 years or longer prior to switching is higher than among those who were with their insurer fewer than two years (855 vs. 820, respectively).

Insurers that achieve high satisfaction scores by providing an outstanding onboarding experience also retain a higher percentage of those customers and have fewer new customers shopping. Among customers who are highly satisfied in their first year with their insurer (overall satisfaction scores of 850 or higher), 81 percent remain with that insurer and only 41 percent shop other insurers. Among customers with lower satisfaction in the first year (809 or lower), only 61 percent remain with that insurer and 61 percent shop.

The study, now in its eighth year, examines insurance shopping and purchase behavior and overall satisfaction among customers who recently purchased insurance across three factors (in order of importance): price, distribution channel and policy offerings.

Study Rankings

Erie Insurance ranks highest among auto insurers in providing a satisfying purchase experience for the second consecutive year, with a score of 843. Erie Insurance performs particularly well in all three factors. MetLife and State Farm rank second in a tie at 839, while American Family and Ameriprise rank fourth in a tie at 835.

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz  Global Wildfire Surge Hits U.S, Propelled by Rising Temperatures

Global Wildfire Surge Hits U.S, Propelled by Rising Temperatures  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t