Jumps in rates and written premiums did little to move the needle on underwriting profits for U.S. personal auto insurers, Fitch Ratings reported based on a recent review of midyear results of nine big market players.

Profitability challenges in the auto line prompted a Fitch downgrade of the lead subsidiary of one of the insurers, Kemper, yesterday, and a changed outlook for another, Horace Mann. Separately, S&P Global Ratings downgraded yet another—Allstate—earlier this week.

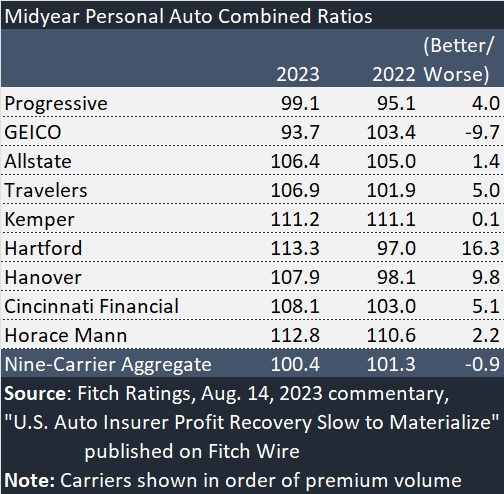

In their analysis of public company GAAP filings titled, “U.S. Auto Insurer Profit Recovery Slow to Materialize,” published earlier this week, Fitch analysts calculated a 10 percent aggregate increase in premiums for the nine-company cohort for the first six months of 2023. But the aggregate combined ratio for the group improved less than a point, dropping to 100.4 for first-half 2023, compared to 101.3 for the same period last year.

The aggregate combined ratio now hovers right above breakeven, with just two of the nine publicly traded personal auto insurers—Progressive and GEICO—reporting sub-100 combined ratios, a chart in the Fitch report reveals

Fitch cited continued unfavorable claims severity and higher catastrophe losses as factors driving the overall underwriting loss for the group.

“Future profit improvement will continue to be hindered by unusually high loss severity,” the Fitch writeup predicted.

The combined ratio figures compiled by Fitch reveal that GEICO was the only one of the nine carriers to actually report a lower combined ratio in first-half 2023 compared to first-half 2022. While GEICO reported a 9.7-point drop in its combined ratio and premiums growing less than 1.0 percent (0.9 percent per Fitch’s calculation), other carriers saw combined ratios grow in the range of 0.1 points (Kemper) to 16.3 points (The Hartford).

Excluding GEICO, the overall first-half 2023 combined ratio for the group is about 103, up about 3 points from last year’s first half ex-GEICO result. (Carrier Management estimates based on premiums and underwriting profit information in the Fitch commentary.)

GEICO vs. The Rest

Commenting on GEICO’s results in the Management’s Discussion and Analysis section Berkshire Hathaway’s second-quarter 2023 report published earlier this month, the conglomerate cited higher average premiums per auto policy, takedowns in prior accident year’s claims estimates and cuts in advertising costs to explain the reversal from last year’s underwriting losses to underwriting profits for the quarter and six month periods.

Although rate increases generated 16.3 percent higher average premiums per policy over the last 12 months, GEICO’s overall premiums were basically flat. A decrease of 2.7 million policies in force over the same period—a 14.4 percent drop in policy counts—explains why premiums did not increase.

Berkshire said the cuts in advertising contributed to the decline in the number of policies.

GEICO’s first-half loss ratio improved 7.5 points, with the prior-year reserve takedown ($888 million) accounting for roughly 3.6 points of the change (by CM’s calculations). The expense ratio improved 2.2 points.

As for other carriers, loss severity continues to be an issue, Berkshire noted. “Average claims severities in the first six months of 2023 were higher for property damage (21-23 percent range), collision (7-9 percent range) and bodily injury (6-9 percent range) coverages,” Berkshire’s stated in the MD&A.

Meanwhile, claim frequency changes varied by coverage, with property damage and collision frequencies down 7-8 percent, while frequencies rose slightly for bodily injury and personal injury coverages.

While GEICO’s premium volume hardly budged, among the remaining carriers analyzed by Fitch, Progressive had an outlier premium jump of more than 20 percent for the first half.

Premium growth averaged 10.2 percent for the nine carriers overall, but only four of the nine—Progressive, Allstate, Travelers and Cincinnati Financial—actually recorded increases of 10 percent or more. Together, first-half 2023 premiums for the eight carriers other than Progressive only grew by about 4 percent.

That’s a problem when loss costs are climbing faster. The Fitch report displays CPI data from the Bureau of Labor Statistics indicating that Motor Vehicle Insurance costs leapt by more than 10 percent annualized for each month since September 2022, including a 17 percent jump in June 2023.

Progressive, in its second-quarter earnings report, revealed that, unlike GEICO, its policies in force are climbing by double-digits, while unfavorable prior-year loss reserve development and catastrophe losses fueled worsening underwriting results through the first six months. On Wednesday of this week, Progressive reported July 2023 results, revealing that the year-to-date combined ratio is now down to 97.6, through seven months, from 99.1 through six months, with premium growth staying at the 20-plus percent level.

In contrast to Progressive and GEICO’s sub-100 combined ratios for the year so far, Kemper, Horace Mann and The Hartford posted first-half combined ratios above 110, with The Hartford’s result deteriorated more than 16 points.

“Persistent severity loss increases in auto have had a meaningful influence on overall industry results. We continue to respond with significant pricing actions,” said Hartford Chief Executive Officer Christopher Swift during a conference call, according to a report from our sister publication, Insurance Journal.

“During the quarter, we achieved renewal written price increases of 13.8 percent and expect acceleration to above 20 percent by the fourth quarter. As loss cost trends emerge, we will aggressively push for appropriate rate actions,” Swift added.

Rating Agency Actions: Horace Mann and Kemper

Fitch took rating actions on the carrier’s with the second- and third-worst first-half auto combined ratios—Horace Mann and Kemper—yesterday.

For Horace Mann, Fitch Ratings has affirmed the ratings of the property/casualty operating subsidiaries at “A” (Strong), but revised the rating outlooks to negative from stable.

“The negative rating outlook for the P/C subsidiaries reflects continued weakness in the personal auto and property lines of business which Fitch believes will persist over its ratings horizon,” Fitch said in a statement. “In 1H23, the auto segment combined ratio deteriorated relative to the prior-year period as a result of persistently high claims severity, while the property business reported above-average catastrophe losses, leading to a total P/C combined ratio of 118.4, compared with 115.3 for full-year 2022.”

Fitch also affirmed the ratings for Horace Mann Life Insurance Company at “A,” and its holding company ratings, citing “strong capitalization; moderate business profile driven by the company’s niche position in the K-12 educator market; and the growing organizational focus on the relatively stable earnings in the life, retirement and supplemental segments which somewhat offset the volatile results in the P/C segment.”

For Kemper, Fitch announced that is downgrading the insurer financial strength ratings of the lead P/C operating subsidiary, Trinity Universal Insurance Company to “A-” (Strong) from “A.”

Fitch has also downgraded the ratings for Kemper’s holding company, while affirming the ratings of Kemper’s life insurance subsidiaries with a stable outlook.

Explaining the downgrades, Fitch cited “continued underwriting weakness” through the first half of 2023 and deterioration in Kemper’s capitalization level.

“Kemper Corporation’s underwriting results remained above rating sensitivities through 1H23, largely as the result of a continuation of heightened loss trends in both the Kemper Auto (nonstandard personal and commercial auto) and Personal Insurance (preferred auto and homeowners) segments, higher catastrophe losses and adverse prior-year reserve development. The Kemper Auto and Kemper Personal Insurance segments reported GAAP combined ratios remained elevated at 109 and 115, respectively, for 1H23,” the Fitch announcement said.

Fitch noted that Kemper’s actions to address underwriting performance with targeted rate increases as well as non-rate actions over the last several quarters should limit further deterioration in underwriting results and help the company’s efforts to return to underwriting profitability over time. The rating agency also reported Kemper’s decision to place its personal insurance business into a planned runoff, noting that this “could have a modest near-term impact on the company’s scale and performance volatility related to property exposure.”

S&P Downgrades Allstate

Earlier this week, another one of the nine big publicly traded auto insurers—Allstate—found itself on the down side of a rating actions. For Allstate, the actions came from S&P Global Ratings. In addition to lowering the holding company long–term issuer credit rating, S&P lowered the financial strength ratings on the core operating subsidiaries to “A+” from “AA-” with a stable outlook.

“The downgrade reflects Allstate’s continued weak underwriting performance given elevated catastrophe losses, persistently high loss costs for the personal auto business, and the increased exposure—measured by premiums—consuming higher levels of capital.”

Highlighting the impact of catastrophes, S&P said that Allstate’s Property-Liability year-to-date catastrophe losses of $4.4 billion, were greater than the $3.1 billion loss in all of 2022. Cats pushed the Allstate six-month combined ratio in the homeowners line to 132.3, S&P’s announcement said.

“The auto business, while improving on an underlying basis in the quarter, still weakened year to date on a calendar year basis to 106.4 from 105 as elevated catastrophe losses and minimal adverse development outpaced a meaningful expense improvement.”

Allstate told investors that auto premium growth is beginning to outpace underlying loss costs during a second-quarter earnings call, and S&P expects the auto combined ratio to improve in the second half as “compounding rate increases start to meaningfully earn through the book.”

Still, however, S&P said it expects the companywide combined ratio to fall in the range of 108-110 range for the full year, assuming a normalized level of catastrophe losses in the second half. The S&P announcement went on to comment on the potential drivers of improvement—continued rate increases, a reduced expense ratio driven by advertising cost cuts and other expense control initiatives, as well as the reduction of “loss-making” policies in force and an effective reinsurance buying strategy. Potential drivers in the other direction include “catastrophe risks in its homeowners business line in the third and fourth quarters of 2023 mainly from wind and fire disasters that could further erode earnings, and ultimately, capitalization,” S&P said.

Separately, on Thursday, Allstate announced estimated catastrophe losses for the month of July of $313 million or $247 million, after-tax, from 18 events. Allstate also reported that it implemented auto rate increases of 8.2 percent across 12 locations during the month of July, resulting in total brand premium impact of 0.9 percent.

“Since the beginning of the year, rate increases for Allstate brand auto insurance have resulted in a premium impact of 8.4 percent, which are expected to raise annualized written premiums by approximately $2.19 billion and rate increases for Allstate brand homeowners insurance have resulted in a premium impact of 7.8 percent, which are expected to raise annualized written premiums by approximately $804 million,” Allstate Chief Financial Officer Jess Merten said in a media statement.

Deep Dive: Understanding Data Center Perils

Deep Dive: Understanding Data Center Perils  Four Insurers Join Ward’s Annual Top 50 P/C Ranking for 2026

Four Insurers Join Ward’s Annual Top 50 P/C Ranking for 2026  Soft P/C Market May Be Shallower Than Previous Cycles: Swiss Re

Soft P/C Market May Be Shallower Than Previous Cycles: Swiss Re  Wellness, Exercise Programs Key to Keeping Workers Healthy

Wellness, Exercise Programs Key to Keeping Workers Healthy