A combination of historic high inflation and a growing frequency of natural catastrophes is creating the hardest market in a generation for property insurance, the American Property and Casualty Insurance Association says in a new white paper.

“The growth of population, housing and businesses in hazard-prone areas are exacerbating the effects of climate change, leading to more frequent and severe catastrophe losses,” stated Karen Collins, the APCIA’s vice president, property and environmental, in a press release. “The higher costs of capital and reduced reinsurance capacity are further exerting upward pressure on insurance rates and may result in stricter underwriting in catastrophe-exposed markets.”

APCIA noted that the U.S. inflation rate hit a 41-year high of 8 percent in 2022, peaking at 9.2 percent last June. Insurance claims have risen even faster, contributing to underwriting losses that pushed the estimated combined loss ratio for property casualty up to 104 according to a preliminary estimate by A.M. Best, the report says. That was the first underwriting loss since 2017.

Both claims frequency and claims severity play a role in those losses. The report says 2022 was the eighth year in a row that the U.S. suffered 10 or more catastrophes with losses exceeding $1 billion. Natural disaster losses from 2020 to 2022 exceeded $275 billion, the highest-ever three-year total for U.S. insurers.

In the meantime, the cost of materials needed for repairs and replacement has increased. The APCIA said the producer price index for residential construction goods jumped 33.9 percent from January 2020 through December 2022. The Consumer Price Index for home furnishings grew 18.7 percent during that period.

U.S. spending on residential construction has been generally rising since 2010. Construction spending remains “resilient,” the report said, in part because of spending made necessary by natural catastrophes.

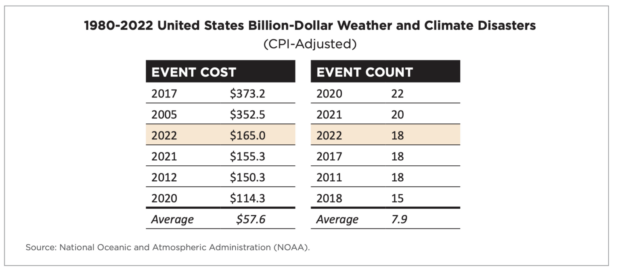

According to the National Oceanographic and Atmospheric Administration, 2022 was unique for landing in the top three years for both frequency of events and overall disaster costs. There were 18 U.S. weather/climate disaster events with losses exceeding $1 billion each, a number that was surpassed only twice before, in 2020 and 2021. Total losses reached $167 billion, a number that was also surpassed only twice before, in 2005 and 2017. (Losses are adjusted for inflation.)

Reinsurers have pulled back, resulting in higher prices. Guy Carpenter estimates that property-catastrophe reinsurance prices rose 30.1 percent this year following a 14.8 percent increase in 2022.

Collins said homeowners and business owners own choices are helping drive the hardening market.

“The growth of population, housing and businesses in hazard-prone areas are exacerbating the effects of climate change, leading to more frequent and severe catastrophe losses,” she said. “The higher costs of capital and reduced reinsurance capacity are further exerting upward pressure on insurance rates and may result in stricter underwriting in catastrophe-exposed markets.”

Collins said insurers are encouraging property owners to harden homes and businesses by upgrading with disaster-resistant materials. Combustable materials such as bark and wood piles should be kept five feet away from homes. Safety devices that use smart technology are also recommended to reduct losses.

Building codes can also play a role in reducing losses. Researchers for the National Institute of Building Sciences say that for every $1 spent on natural hazard mitigation in new code construction can save $11 in disaster repair and recovery costs. In 2020, the Federal Emergency Management Agency released a report that says building in compliance with modern building codes leads to major reductions in property losses from floods, hurricane winds and earthquakes.

The report says the amount of damage caused by Hurricane Ian last year is a case in point. Compared to Hurricane Charley, which followed a similar path across the Florida peninsula in 2004, Ian caused considerably less wind damage and there were fewer partial and total roof failures.

“Commercial and residential properties with mitigation measures such as flood vents, updated roofs and hurricane shutters inherent to their construction were able to withstand the storm’s wrath and limit damage,” the report says.

Top photo courtesy of APCIA.

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums  Zurich CEO: El Niño May Mean Fewer Hurricanes, Insurance Losses in North America

Zurich CEO: El Niño May Mean Fewer Hurricanes, Insurance Losses in North America