Executives of InsurTech Lemonade say they’re slowing down growth in 2023, as the company waits for regulators to approve rate hikes needed to keep up with inflation.

“So long as these mismatched pockets persist, our growth will be more muted, as we skirt mispriced enclaves,” company leaders said in the annual report to shareholders published last night, referring to places where regulatory rate approvals are lagging.

While growth metrics continued to soar last year, the company is still betting that “peak losses” were reached in 2022 and that loss ratio improvement will continue.

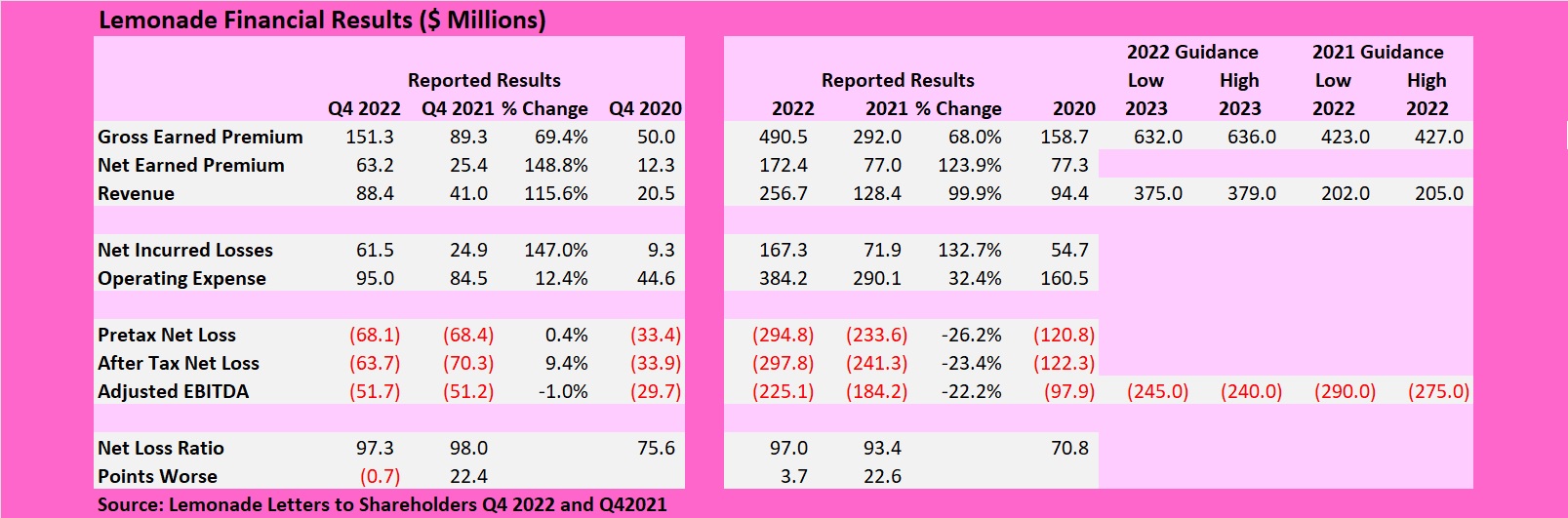

On the growth front, gross earned premiums jumped 68 percent to just under $500 million, while net earned premiums rose 124 percent, and revenues (net premiums plus ceding commissions and investment income) doubled.

For the most part, Lemonade measures the success of its efforts to lower insurance losses and expenses by tracking an “adjusted EBITDA” measure, which came in at $225 million in the red for the year—better than guidance offered by the company in early 2021, which put the expected EBITDA loss figure as high as $290 million. According to notes to Lemonade’s financial statements, “adjusted EBITDA losses” are net earnings (or losses) before interest, taxes, depreciation and amortization adjusted for a few other items—the most significant of which is stock-based compensation expense.

Removing the stock-based compensation expense and other adjustments, the unadjusted bottom-line net loss figure (after taxes) was $297.8 million in 2022.

Commenting on the fourth-quarter 2022 result, the Lemonade shareholder report said the “adjusted EBITDA” loss was almost identical to the same measure for the final quarter of 2021, “yet our business was two-thirds larger this year than last—highlighting the rapid and demonstrable improvements to our underlying business during the course of 2022.”

Although the narrative of the shareholder letter indicates that executives believe that “peak losses” are behind them, the guidance included for 2023 indicates a higher “adjusted EBITDA” loss of at least $240 million for the full year.

The more usual key performance metrics reported by property/casualty insurance carriers—gross and net loss ratios—stabilized in 2022. The gross loss ratio for the full year, 90, was the same as the gross loss ratio reported for 2021, while the net loss ratio deteriorated roughly 4 points to 97.0.

Referring to the rate changes filed in 2022, the report said: “It was a year of soaring inflation, in response to which we filed eight times more rate changes with regulators across the country, as compared to 2021. Most of these rate changes have yet to be approved, implemented, and earned in, so we expect continued loss ratio improvement as they do.”

Later, the report referred to an apparent slowdown of inflationary trends, and to the fact that the problematic states that delayed rate hike approvals—the “mismatched holdouts”—are shrinking. Still, the report added, “inflation in pet services and home and car repairs have trended disproportionately high, and some regulators have been slow or resistant in approving commensurate rate adjustments. Our determination to exclude such areas from our growth plans means that for now we expect overall annual [in-force premium] growth of approximately 11-12 percent, though we’ll look to catch up to our multi-year target of 20-25 percent as our rates come online.”

As of Dec. 31, 2022, in-force premium stood at $625.1 million, and executives expect the figure to grow to $695 million or $700 million in 2023.

For the final quarter of 2022, revenue grew 116 percent to $88.4 million, which Lemonade attributed primarily to a 69 percent jump in gross premium, but also to a reduction in the proportion of earned premium ceded to reinsurers, to 58 percent in fourth-quarter 2022 from roughly 72 percent in fourth-quarter 2021. Absent the shift in cession rate, revenue would have grown roughly in line with gross earned premium, the shareholder report said.

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz