Seven insurance company impairments were identified in the U.S. property/casualty industry in 2020, with five of the seven involving auto insurers, according to an A.M. Best special report.

Last year’s number was an improvement over 2019 when 13 impairments were identified, according to the report “2020 U.S. Property/Casualty Impairments Update.”

A.M. Best detailed the 2020 impaired insurers as:

- Two standard private passenger auto writers, consisting of a Texas reciprocal exchange and a New York insurer,

- Two non-standard private passenger auto insurers with business written in multiple states, primarily Florida and Texas,

- A risk retention group (RRG) that provided commercial auto liability and general liability insurance to independent owner operators and small trucking companies in seven states, primarily California (where the liquidator has filed a federal lawsuit against the president and several outside advisors alleging the defendants falsified bank documents to conceal the financial condition of the entity)

- A workers’ compensation insurer with business written primarily in New York and New Jersey and

- A title insurer that underwrote policies primarily for owners and mortgagees of residential properties in New York.

All the 2020 impairments were placed into insolvent liquidation.

A.M. Best defined impairments as situations in which a company has been placed, via court order, into conservation, rehabilitation or insolvent liquidation. Supervisory actions undertaken by state insurance department regulators without court order are not considered impairments, unless delays or limitations were placed on policyholder payments.

Impairment Trends During 2000-2020

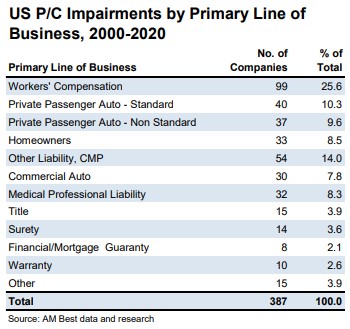

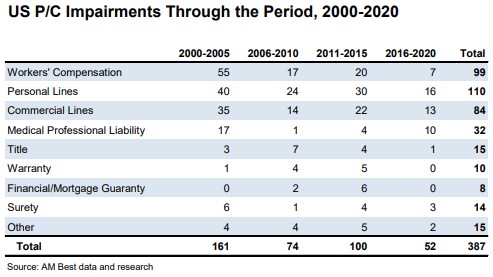

The report went on to track impairment trends for the period 2000-2020. AM Best identified 395 impaired property/casualty insurers during those years, with the leading line of business being workers’ compensation, which accounted for 26% of the impairments during the period. “The most notable shifts over the 20-year period have been the reduction in workers’ compensation insurer impairments, the reemergence of difficulties for insurers in the medical professional liability segment, and the general reduction in impairments overall,” said the report.

During the 20-years, personal lines insurers accounted for 28%, split between private passenger auto (20%) and homeowners (9%). Private passenger auto can be further broken down as standard (10%) and non-standard auto insurers (10%). Commercial lines insurers accounted for 22%, split between other liability/commercial multi-peril (14%) and commercial auto (8%). The remaining 24% was split among specialty lines.

“Specific causes have been identified for some of the impairments, with most falling into the category of general business failure arising out of some combination of poor strategic direction, weak operations, internal controls weaknesses or underpricing and under-reserving of the business,” said the report. “The most relevant aspect of these impairments may be the products these companies offered and the products’ potential risks.”

Diving into the causes of 97 of the impaired insurers, A.M. Best found that the leading reason for a company failure was fraud or alleged fraud – affecting 25 companies during the 20 year period. Problems with affiliates were the cause of 22 impairments, while catastrophe losses were blamed on 21 impairments. Sixteen companies became impaired after experiencing rapid growth, and investment losses were a significant factor in 11 impairments, said A.M. Best.

And finally, one insurer became impaired because of reinsurance failure and another was placed into liquidation after marketing warranty insurance products without a license.

“The most notable shifts over the 20-year period have been the reduction in workers’ compensation insurer impairments, the reemergence of difficulties for insurers in the medical professional liability segment, and the general reduction in impairments overall,” said the report.

During the 20-year period, A.M. Best noted that the impairments consisted of 321 insolvent liquidations and 74 rehabilitations, of which 37 were closed during the period and 37 remained open. In addition, there were 54 conservatorships, all of which led directly to either rehabilitation or liquidation.

Source: A.M. Best

*This story ran previously in our sister publication Insurance Journal.

Liberty Mutual Introduces Its Newest Brand Character: Liberty Biberty

Liberty Mutual Introduces Its Newest Brand Character: Liberty Biberty  A Matter of Trust

A Matter of Trust  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz