If the National Association of Insurance Commissioners doesn’t act this year to correct systemic racial bias in insurance ratemaking and other processes, Congress may pass anti-discrimination laws that apply to insurance, a consumer advocate said earlier this month.

Birny Birnbaum, the director for the Center for Economic Justice, a consumer advocacy organization, made the prediction toward the end of a session of the Casualty Actuarial Society’s Ratemaking, Product and Modeling seminar in mid-March when asked if he sees regulatory and legislative fixes on the near-term horizon.

“A lot is going to depend on what the NAIC does this year. They have a committee on race in insurance,…and if the NAIC takes some concrete actions, then I think there’s potential for state-based regulation to move in a very positive manner in the next couple of years.”

But absent such action “this year” from the NAIC, “I think the likelihood is the action will come from the Feds—that we’ll see we’re more likely to see federal antidiscrimination and civil rights legislation coming from Congress that applies to state-based insurance regulation,” said Birnbaum, a former associate commissioner for policy and research at the Texas insurance department who served for many years as the designated consumer representative of the NAIC.

Birnbaum, who focused his presentation prior to the Q&A on a method of disparate impact analysis that would improve cost-based pricing—one that would involve actually using race-based information—also stressed that pricing isn’t the only place where actuaries and regulators need to dedicate efforts to remove racial bias. Marketing and anti-fraud investigation practices during claims settlement may, in fact, be more ripe for scrutiny, he said.

Co-panelist Roosevelt Mosley, a principal and consulting actuary with Pinnacle Actuarial Resources, began his own remarks noting that none of these problems is easy to solve. “These issues are historic. These issues have been around for years, [and] you aren’t going to fix 200 years of systemic racism overnight,” he said.

Mosley, who regularly participates in discussions with state insurance regulators, suggested that forums like the CAS session titled “Disparate Impact: The Impact of the Social Justice Movement on Insurance Rating” improve the odds of removing insurance pricing bias. “It’s going to take a little longer than probably what most people would define as the near future. But if we really do get to the point where we did have these conversations, where we’re sitting down at a table, all the different interested parties, and really talking through the hard issues and talking through what the solutions look like, we’ve got a better chance at getting somewhere faster.”

Based on his own experience participating in meetings for NAIC and the National Council of Insurance Legislators and speaking in state forums about state-specific insurance bills, Mosley reported, “for reasons that you could probably guess, those don’t tend to be the most productive conversations…Often, discussions end up devolving into things that don’t get to a really solid solution.”

If the debate continues in a fashion where “people are yelling at each other, then are we going to get somewhere? We’ll probably get somewhere. It may not be somewhere where everyone likes,” he said.

Where Actuaries Stand Today

The way forward “is for insurance companies, and the actuarial profession, to get out in front right now,” Birnbaum agreed.

Both speakers began their presentations defining terms like disparate impact and disparate outcomes, as well as polling the actuaries about their perceived roles in taking bias out of insurance pricing. Specifically, Mosley asked more than 100 ratemaking actuaries attending whether they had started to examine issues of racial bias in insurance pricing in their current jobs. While 60 percent said they had either started or considered examining the issues, roughly 40 percent said they had not yet even considered it.

Birnbaum asked the actuaries about the company environments in which they do their work, with choices like “my company has a policy to examine the algorithms for racial bias” and “my company has been receptive to suggestions for examining algorithms for racial bias.” Although half the respondents selected one of those two descriptions, more than one-third selected a choice worded, “My company doesn’t use, collect or consider racial characteristics, so there is no need to test our practices for racial impact.”

“That’s a little troublesome on its face,” said Birnbaum, reviewing that last result. “Sometimes that particular line is used by insurer trade associations to argue that insurance can’t possibly discriminate on the basis of race because they don’t consider race. That represents a fundamental misunderstanding of how structural racism operates,” he said.

In fact, Birnbaum would go on to argue that “efforts to address discrimination on the basis of race require explicit consideration of race”—or said more technically, they need to control for protected characteristics like race in pricing algorithms. Building to that conclusion, the consumer advocate first reviewed ways in which systemic racism can manifest in insurance, distinguishing between disproportionate outcomes tied to historic discrimination and disproportionate outcomes resulting from risk classifications that serve as proxies for race. Insurance actuaries should focus their skills on remedying the latter, he said.

Explaining the former, Birnbaum offered the example of disparate life and health insurance outcomes rooted in the prevalence of certain health conditions and shorter life expectancy in communities of color. “It’s the role of state or federal legislatures to address this,” he stated.

“Insurance should not be the tool to address societal inequities when doing so distorts the cost-based framework of insurance,” he said emphatically, noting the role of Congress in deciding that Americans should have access to health insurance regardless of pre-existing conditions, expected claim outcomes or ability to afford coverage. “So, Congress established permissible risk classifications, and Congress provided funds to assist those unable to afford insurance. Congress did not ask insurers to subsidize insurance for some consumers,” he said.

On the other hand, proxy discrimination—”where a risk classification is actually predicting race, and not the insurance outcome”—is the type of unnecessary, unfair discrimination that is “precisely amenable to actuarial skillsets,” Birnbaum said.

“One answer to this problem is to apply analytics to identifying and minimizing disparate impact. And it’s clear to me that if that’s going to happen in insurance, it’s going to be the actuarial profession that will lead regulators and policymakers.”

“One answer to this problem is to apply analytics to identifying and minimizing disparate impact. And it’s clear to me that if that’s going to happen in insurance, it’s going to be the actuarial profession that will lead regulators and policymakers.”

Birny Birnbaum, Center for Economic Justice

He reviewed an approach that actuaries can apply to multivariate pricing models, explicitly introducing “race” or another “protected class” as a “control variable” to ferret out the degree to which other predictive variables correlate with the control variable. (See sidebar, “Race as a Control Variable” for a more detailed discussion.)

Birnbaum argued that this type of disparate impact analysis improves cost-based pricing. But there is one big problem with all such approaches—one that actuaries repeatedly wrote about in text chats during Birnbaum’s presentation, and one that he ultimately volunteered to address. The basic problem is that insurers do not collect data on an insurance applicant’s race, so they can’t use it even as a test variable in their models.

Offering a possible solution, he said insurers could assign a racial characteristic to an individual based on the racial characteristics of a small geographic area, like a census block. Another approach that’s been studied combines geographic data and a last name analysis, he noted, going on to suggest the alternatives of reaching out to data brokers and vendors for new data and simply starting to collect racial characteristic data.

Managing Risk Inputs or Price Outcomes

Mosley began his talk referring to what he termed “the guiding principle for ratemaking”—the idea that rates are to be adequate, not excessive and not unfairly discriminatory. The phrase, which is “drilled into” the heads of actuaries focused on ratemaking, is written into many state laws. Further, the notion that a rate conforms to the guiding principle “if it is an actuarially sound estimate of the expected value of all future costs associated with an individual risk transfer” is actually part of the Statement of Principles on Ratemaking of the CAS, he said. (Editor’s Note: The CAS Board recently rescinded that principles statement and others. See related article, “Status of Certain Casualty Actuarial Ratemaking, Reserve Principles in Flux.” After opening the decision up for comment, the board initially rejected efforts to reinstate the principles. In early May, the CAS board officially reinstated the principles.)

The actuary went on to display definitions of terms like “unfair discrimination” and “proxy discrimination” (related sidebar) that are being referred to in some forums and in bills being introduced in some states, noting that discussions of what is fair or unfair are moving beyond the “expected value of future costs” definition of fairness. Actuaries involved in analytics “need to begin thinking about these issues. “If we’re not part of the discussion, a lot of these things will ultimately end up being defined for us,” he said, adding that difficulties inherent in satisfying some of these definitions will become more apparent down the road.

He then polled the actuaries viewing the virtual session to weigh in on courses of action ranging from doing nothing to controlling for protected characteristics in pricing as Birnbaum had recommended. Other possible alternatives offered in the poll were to prohibit problematic risk characteristics from being used in developing premiums and adjusting the final pricing outcomes for protected classes.

My suspicion is that if we held each of the risk characteristics that are used to price insurance, it’d be pretty hard to find a lot of them that don’t bear at least some relationship to some of these protected characteristics. At that point, the question becomes how much is too much.

My suspicion is that if we held each of the risk characteristics that are used to price insurance, it’d be pretty hard to find a lot of them that don’t bear at least some relationship to some of these protected characteristics. At that point, the question becomes how much is too much.

Roosevelt Mosley, Pinnacle Actuarial Resources

Roughly half of the poll takers agreed with the approach Birnbaum advocated, but Mosley noted that the “control variable” approach is only directly applicable to certain model types. “Modeling approaches that don’t necessarily have a linear structure like the GLM [generalized linear models] wouldn’t lend themselves as well to a control kind of approach,” he said.

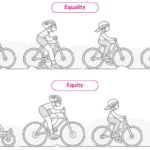

Another Proposal: Equality vs. Equity

About a quarter of the actuaries thought that adjusting the final outcomes rather than focusing on model inputs was a promising idea for eliminating racial bias in pricing. “You can think of it as more of a UK-style regulation, where the regulation doesn’t necessarily focus on how companies are making rates. They’re more focused on the actual rates that come out on the back end, with the thought process being that if [those] are discriminatory, then there’s a problem that needs to be addressed,” Mosley said.

Birnbaum doesn’t like the idea. “That ends up skewing risk-based pricing. From our perspective, giving consumers the true price of protection is vitally important for making financial decisions,” he said.

Separately, Daniel Schreiber, the CEO of InsurTech Lemonade, recently advanced the idea that adjusting outcomes to make risk-based prices equitable and affordable for protected classes is the job of governments and regulators. Echoing Birnbaum’s view that insurance isn’t a tool to address social inequities, Schreiber proposed a solidarity tax and rebate process to be mapped out by regulators, in a LinkedIn post titled “AI Doesn’t Do Solidarity.” In the post, Schreiber distinguishes between equality (where pricing reflects the risk that each individual represents, determined through AI and machine learning) and equity (which considers circumstances of hardship and affordability).Beyond Pricing: The Way Forward

Back at the CAS session, panel moderator Mallika Bender, co-chair of the Joint CAS/SOA Committee on Inclusion, Equity and Diversity, teed up other questions raised by the virtual audience, including whether there is any particular variable they could use for ratemaking that would actually be free of bias.

“It’s really the $64,000 question—how much is too much?” Mosley said. “My suspicion is that if we held each of the risk characteristics that are used to price insurance [to scrutiny], it’d be pretty hard to find a lot of them that don’t bear at least some relationship to some of these protected characteristics. So, at that point, then the question becomes how much is too much.”

He continued: “If you define 50 percent correlation as too much, then everything over 50 is out, everything under 50 is in, and that still doesn’t necessarily address the entire problem. Part of the challenge [is] defining what’s the outcome that we’re looking to get to. And then secondly, once we define that outcome, is the individual factor approach the way to do it? Or is there some other more holistic approach that allows us to address the issue directly?”

Birnbaum emphasized that while pricing and underwriting are the main focus of discussions about discrimination in insurance, he believes it’s even more important for insurance companies to examine marketing and claim settlements practices. “In an era of big data, the way you market, the way folks learn about things through micro-targeting means that you can get pre-selected before you even make an [insurance] application,” he said. “So, if there’s disparate impact in terms of marketing, that’s going to basically pre-underwrite before anybody comes to you.”

To his mind, insurer processes for identifying potentially fraudulent claims are the most problematic—and are his top candidates for disparate impact scrutiny. Those processes “have a self-fulfilling prophecy built in: You can’t identify a claim as fraudulent unless you identify it as suspicious and then investigate. So, if your algorithms are based on claims that you’ve historically identified as suspicious or fraudulent, then your data is going to keep pushing you for those same types of claims and claimants.”

Summing up his thoughts about disparate impact in pricing and the other areas, Birnbaum said, “I think the way to address that is for insurance companies, and the actuarial profession, to get out in front right now. The lead cannot be taken by insurance trade associations, which “have an incredibly reactionary view,” or by state legislators through NCOIL. (Editor’s Note: Birnbaum alluded to the fact that NCOIL recently passed amendments to the NCOIL Property/Casualty Insurance Modernization Model Act, in which they define proxy discrimination as the “intentional substitution of a neutral factor” for a factor based on race, color, creed, etc., ignoring unnecessary unintentional bias.)

“If that continues, if those forces carry the day, then I think the change is going to come from the federal government, which is not what anybody who is interested in state-based regulation wants,” he said.

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  UN, Scientists Warn Strong El Niño Will Add Fuel to ‘Planet Already on Fire’

UN, Scientists Warn Strong El Niño Will Add Fuel to ‘Planet Already on Fire’